The Chilean automotive market reached a significant milestone in April 2026, as electric vehicle (EV) adoption accelerated to nearly 10% market share, effectively tripling the figures recorded just one year prior. This sudden shift marks a decisive turning point for a nation that has long been a regional leader in renewable energy and public electric transit but had previously struggled to convert its passenger vehicle segment to electric power. Driven by a combination of escalating global fuel prices, stringent new efficiency regulations, and an influx of competitive models from Chinese manufacturers, the Chilean market is now undergoing one of the fastest transitions to electromobility in Latin America.

A Turning Point for South American Electromobility

For years, Chile has occupied a unique position in the Latin American economic landscape. As the wealthiest country in the region per capita, it has frequently served as a testbed for new technologies. This is most evident in the energy sector, where the country boasts the highest per-capita deployment of solar energy in the region, primarily concentrated in the sun-drenched Atacama Desert. Furthermore, Chile was a global pioneer in the electrification of public transport; its capital, Santiago, hosts the second-largest fleet of electric buses in the world, surpassed only by major metropolitan areas in China.

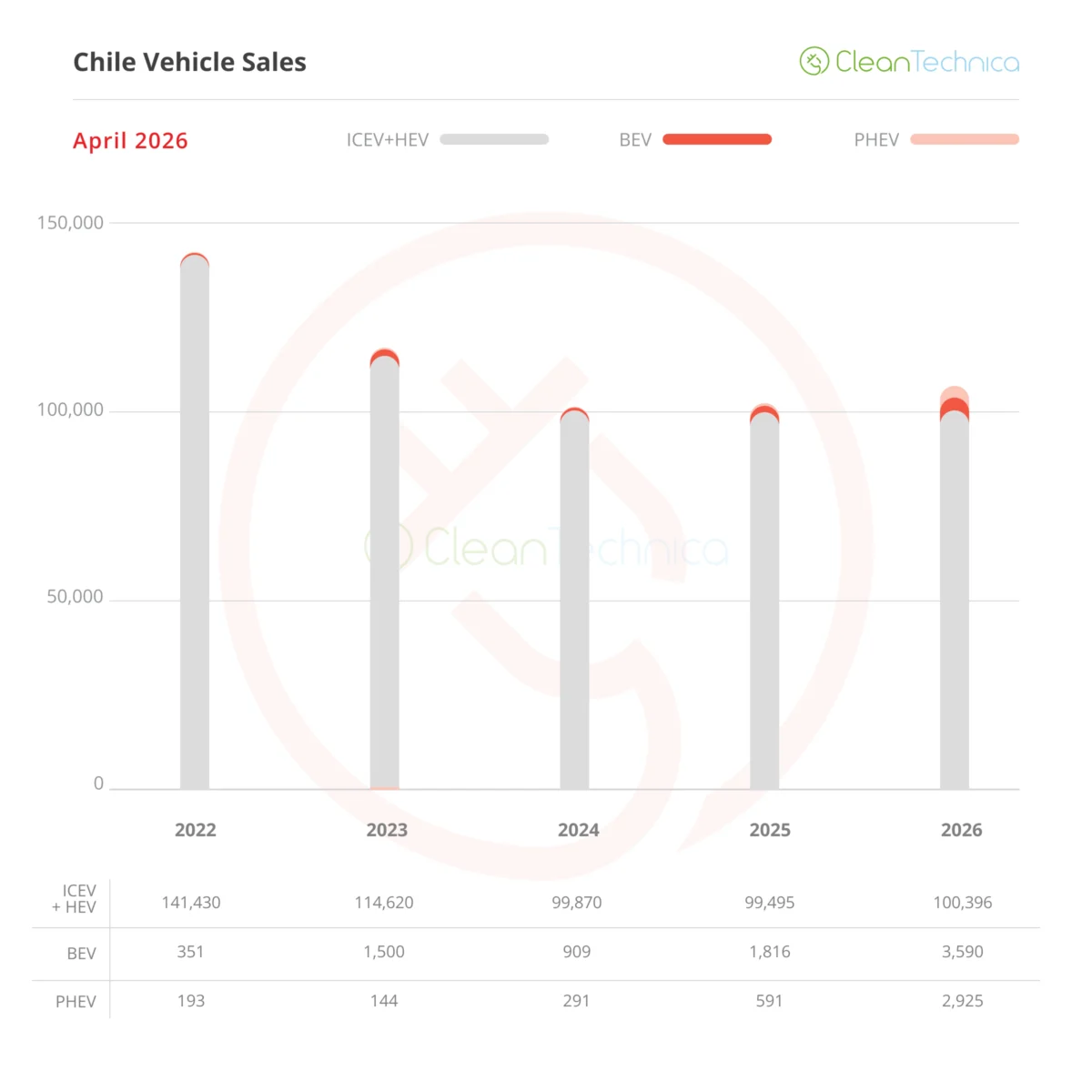

Despite these successes, the passenger vehicle market remained stubbornly reliant on internal combustion engines (ICE). By the end of 2025, the market share for passenger EVs sat at a modest 3.3%. Early 2026 saw a slight uptick to 4.72% in the first quarter, but this still lagged significantly behind regional neighbors like Uruguay, which has seen adoption rates exceed 30%. However, the data for April 2026 indicates that the "slumber" of the Chilean EV consumer has ended. Monthly sales approached the 3,000-unit mark for the first time, signaling a fundamental shift in consumer behavior and market dynamics.

The Economic Catalyst: Global Geopolitical Volatility and Fuel Inflation

The primary driver behind this sudden acceleration appears to be economic necessity. Chile produces negligible amounts of crude oil and is almost entirely dependent on international imports to sustain its transport sector. Consequently, the domestic economy is highly sensitive to fluctuations in global oil markets. Recent geopolitical instability—specifically the escalation of conflict in the Middle East involving the United States and Iran—has severely disrupted global supply chains, removing an estimated 10% of the world’s oil supply from the market.

For Chilean consumers, the impact at the pump has been immediate and painful. Prior to the current crisis, gasoline prices in Chile were already among the highest in the region at approximately $1.30 per liter ($4.95 per gallon). Following the onset of the conflict, prices surged to $1.70 per liter ($6.40 per gallon). This 30% increase in fuel costs has fundamentally altered the total cost of ownership (TCO) equation for Chilean drivers, making the switch to electric or plug-in hybrid vehicles a financial imperative rather than a lifestyle choice.

Market Composition: The Unprecedented Rise of Plug-in Hybrids

An analysis of the April 2026 sales data reveals a fascinating divergence from previous years. Historically, the Chilean EV market was dominated by Battery Electric Vehicles (BEVs), which accounted for roughly 75% of all electrified sales in 2025. However, the current surge has been led by Plug-in Hybrid Electric Vehicles (PHEVs), leading to a state of near-parity between the two powertrains.

While BEV sales have maintained a healthy year-over-year growth rate of 150%, PHEV sales have exploded with a staggering 535% increase. Analysts suggest this is due to "range anxiety" combined with immediate economic pressure. Consumers looking to escape high gas prices but wary of the charging infrastructure for long-haul travel across Chile’s unique geography are opting for PHEVs as a transitional solution. This shift has allowed the total EV market share (BEV + PHEV) to hit 9.9% in April, with BEVs specifically accounting for 5.3%.

Competitive Landscape: The Dominance of Chinese Automakers and Tesla

The Chilean market is currently one of the most competitive in the world, largely due to its open-trade policies and lack of domestic automotive manufacturing, which allows brands from all continents to compete on a level playing field. In April 2026, the brand rankings saw a surprising shift. Changan, a Chinese automaker, secured the top spot on the podium. This success is largely attributed to the launch of the Cs55 PHEV, an affordable SUV that has resonated with middle-class families feeling the pinch of fuel inflation.

Following Changan are the perennial leaders of the global EV transition: BYD and Tesla. BYD’s extensive range of both BEV and PHEV models has allowed it to maintain a dominant year-to-date lead, while Tesla’s Model Y remains the single best-selling electric model in the country. Other notable performers include Volvo and Riddara, the latter of which has found a niche with the Riddara 6 PHEV pickup truck.

A significant takeaway from the 2026 data is the diversity of the market. Unlike other Latin American markets where one or two models dominate the charts, the Chilean top-ten list is highly competitive. The sales gap between the number one model (Tesla Model Y) and the number ten model (Jaecoo 7) is relatively narrow, indicating a healthy ecosystem with multiple viable options for consumers across different price points and vehicle segments.

Regulatory Framework: Efficiency Standards and Importer Obligations

While fuel prices provided the immediate "push" for consumers, government policy provided the "pull" for manufacturers. Chile is currently the only country in Latin America to have implemented comprehensive energy efficiency regulations for the automotive sector. Under the current legal framework, vehicle importers are held to strict average efficiency standards across their entire fleet.

These regulations are tiered across three categories (light, medium, and heavy vehicles), with requirements becoming progressively stricter each year. Importers who fail to meet these standards face significant financial penalties. Crucially, the law allows for a "credit" system where importers of high-emission internal combustion engine vehicles (ICEVs) can offset their averages by importing and selling more EVs. This has forced traditional legacy automakers to either accelerate their own EV launches or partner with EV-only brands to balance their portfolios. This regulatory environment ensured that when fuel prices spiked, a wide variety of EV models were already available in showrooms to meet the sudden demand.

Economic Barriers: The Persistence of Low-Cost Internal Combustion Vehicles

Despite the record-breaking growth in the EV sector, the transition faces a formidable opponent in the form of hyper-affordable ICEVs. Chile remains one of the few markets where consumers can still purchase a new vehicle for under $10,000 USD.

The price gap remains the primary hurdle for mass-market adoption. For instance, the Geely EX2, one of the most affordable EVs in Chile, is priced at approximately $19,100 USD. While competitive for an EV, it sits in stark contrast to its internal combustion counterpart, the Geely Coolray Lite, which retails for roughly $11,800 USD. In a cooling economy, the $7,000 price difference remains a barrier for lower-income households, even when factoring in the long-term savings on fuel.

However, the April data suggests that the "tug-of-war" between cheap ICEVs and efficient EVs is beginning to lean toward the latter. Total vehicle sales in Chile have stabilized at around 100,000 units for the first four months of the year, but nearly all the growth in the market has been captured by electrified powertrains. Sales of traditional combustion-only vehicles are beginning to stagnate or decline for the first time in the country’s history.

Future Outlook: Toward Energy Independence and Regional Dominance

The implications of Chile’s EV surge extend far beyond the automotive sector. By reducing its reliance on imported fossil fuels, Chile is effectively insulating its economy from future geopolitical shocks. The country’s massive investments in solar and wind energy mean that the "fuel" for these new EVs is produced domestically, keeping capital within the country and supporting the local green energy industry.

Industry experts anticipate that if global oil prices remain elevated, the 10% market share seen in April could become the new baseline for the remainder of 2026. This would place Chile on a trajectory to meet its goal of 100% electric sales for small and medium vehicles by 2035.

Furthermore, Chile’s success provides a roadmap for other nations in the region. While Peru and Colombia have shown interest in electromobility, they have yet to implement the combination of infrastructure, regulatory pressure, and market openness that has allowed Chile to pivot so rapidly. As the Chilean economy continues to integrate its "Atacama electrons" into its transport network, it solidifies its position as the regional leader in the global transition to a low-carbon economy.

The transition is not without its challenges—infrastructure in rural areas still requires significant investment, and the used car market for EVs is still in its infancy. However, the data from early 2026 makes one thing clear: the era of internal combustion dominance in Chile is beginning to wane, replaced by a more resilient, domestically powered, and technologically advanced transport ecosystem.