The Regulatory Landscape: From Voluntary to Mandatory Disclosure

The introduction of the UK SRS represents a pivotal moment in the UK’s commitment to becoming a global leader in green finance. Following the recommendations of the International Sustainability Standards Board (ISSB), the UK government has moved to adopt a framework that aligns closely with global standards, specifically IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and IFRS S2 (Climate-related Disclosures). This alignment is intended to create a "common language" for sustainability reporting, allowing investors to compare the performance of companies across different jurisdictions with greater clarity and confidence.

The Financial Conduct Authority (FCA) has been at the forefront of this transition. Recently, the regulator proposed that mandatory UK SRS-aligned reporting should begin for listed companies as early as 2027. While the initial focus is on publicly traded entities, the government has signaled that large private companies will likely fall under the scope of these requirements shortly thereafter. This phased approach is designed to give the market time to mature, though it leaves a relatively narrow window for large organizations to overhaul their data collection and reporting infrastructures.

Sweep’s Technical Response to UK SRS Requirements

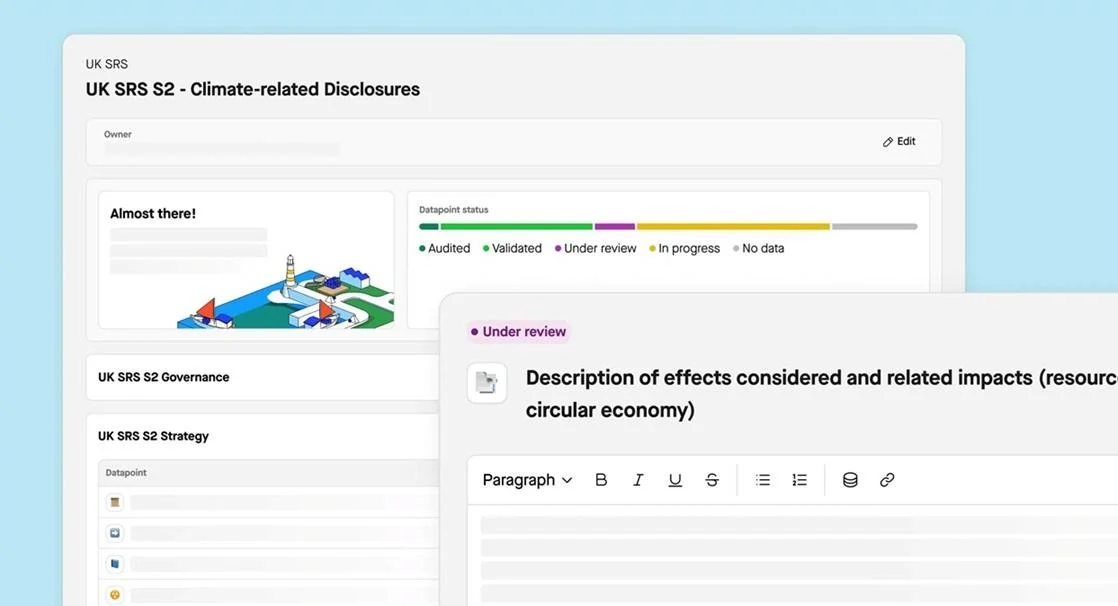

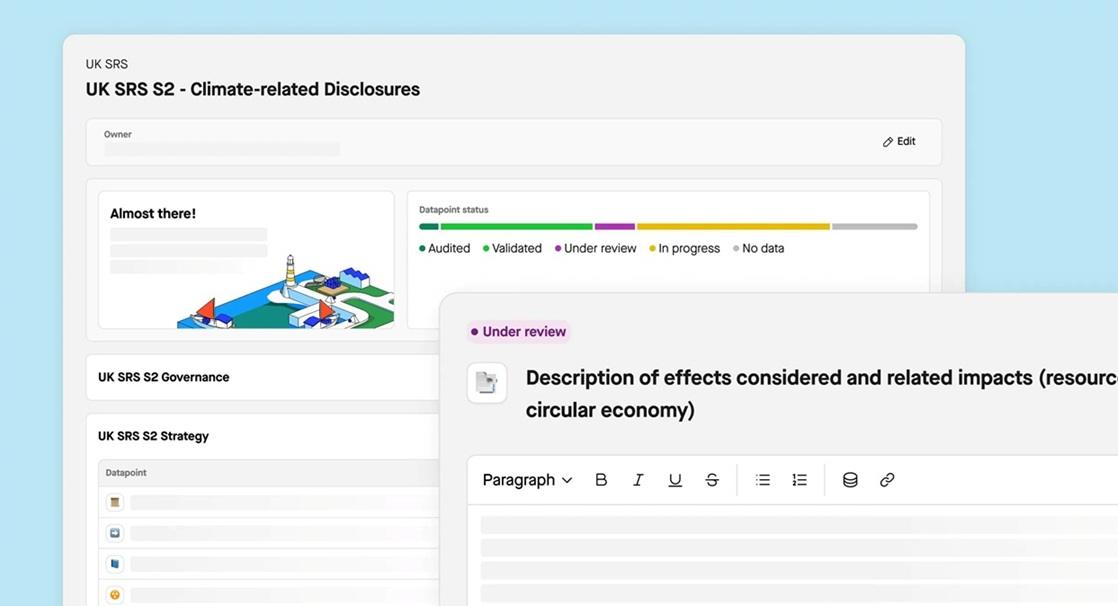

Sweep’s newly launched solution is engineered to address the specific technical challenges posed by the UK SRS. One of the primary hurdles for large enterprises is the sheer volume of data required to fulfill the disclosure requirements of IFRS-based standards. These standards demand not only high-level carbon footprints but also detailed narratives on governance, strategy, risk management, and metrics and targets.

Key features of the Sweep UK SRS solution include:

- Full Disclosure Mapping: The platform provides comprehensive pre-mapping to every specific disclosure required under the UK standards. This ensures that sustainability teams are not starting from scratch and can see exactly which data points are missing or require updates.

- AI-Assisted Narrative Generation: Through "Sweepy," the platform’s proprietary AI assistant, companies can automate the drafting of narrative responses. By scanning existing data held within the platform, Sweepy can populate data points and draft descriptions that align with the required reporting format, significantly reducing the administrative burden on ESG teams.

- Governance and Auditability: To meet the "limited assurance" and eventually "reasonable assurance" requirements that often accompany mandatory reporting, Sweep has integrated rigorous approval workflows and immutable audit trails. This allows internal and external auditors to trace every figure back to its original source, ensuring data integrity.

- Supply Chain Integration: Recognizing that Scope 3 emissions—those originating in a company’s value chain—often represent the largest portion of a firm’s footprint, the solution includes dedicated supplier interfaces. This facilitates the collection of primary data from vendors, moving away from the less accurate spend-based estimates that have characterized early-stage ESG reporting.

- Interoperability and Cross-Framework Coverage: Many UK-listed firms also operate in Europe or report to global bodies. Sweep’s solution allows the same core dataset to be utilized for the EU’s Corporate Sustainability Reporting Directive (CSRD), the Carbon Disclosure Project (CDP), the Global Reporting Initiative (GRI), and specific investor-led reporting requests.

Chronology of the UK Sustainability Reporting Evolution

The path to the UK SRS has been several years in the making, reflecting a global trend toward the "institutionalization" of ESG data.

- November 2020: The UK government announces its intention to make TCFD-aligned (Task Force on Climate-related Financial Disclosures) disclosures mandatory across the economy by 2025.

- November 2021: During COP26 in Glasgow, the IFRS Foundation announces the creation of the ISSB to develop a global baseline for sustainability disclosures.

- June 2023: The ISSB issues its inaugural standards, IFRS S1 and IFRS S2.

- Early 2024: The UK government officially releases the finalized UK Sustainability Reporting Standards, confirming they will be based on the ISSB framework.

- Mid-2024: Sweep launches its dedicated UK SRS solution to assist early adopters and firms preparing for the 2027 deadline.

- 2027 (Projected): Mandatory reporting begins for the first wave of UK-listed companies.

Market Context and Data Challenges

The demand for specialized tools like Sweep’s is driven by the increasing complexity of ESG data. According to recent industry surveys, nearly 70% of corporate sustainability leaders report that data collection remains their biggest challenge in meeting disclosure requirements. Furthermore, the shift from voluntary "marketing-led" sustainability reports to "finance-grade" regulatory filings means that the margin for error has disappeared.

The UK SRS requires companies to disclose how climate change affects their financial position and prospects. This necessitates a close collaboration between sustainability departments and finance teams. Historically, these two departments have operated in silos, using different software and methodologies. Sweep’s platform acts as a centralized "source of truth," bringing these departments together under a single governance framework.

Industry data suggests that companies that invest early in automated ESG reporting tools can reduce their reporting costs by up to 40% over a three-year period. By automating data ingestion and utilizing AI for narrative drafting, firms can pivot their ESG teams away from manual spreadsheet management and toward strategic decarbonization efforts.

Leadership Perspectives and Official Responses

Rachel Delacour, CEO and co-founder of Sweep, emphasized the urgency of the situation during the product launch. She noted that the UK SRS standards represent a "significant ask" for corporations, particularly regarding the depth of data required. "The timeline is tight for any large corporation to get organized for this new report," Delacour stated. She further highlighted Sweep’s advantage as an official ISSB licensee, which allows the company to embed expert-level knowledge directly into the software’s architecture.

Regulatory bodies have also weighed in on the necessity of high-quality data tools. While the FCA does not endorse specific software, it has repeatedly emphasized that "robust data and clear disclosures are essential for market integrity." In its recent consultation papers, the FCA noted that the move to UK SRS is intended to provide investors with "comparable, reliable, and decision-useful information."

Institutional investors, who are the primary users of these disclosures, have expressed support for the UK’s move toward ISSB-aligned standards. Many large asset managers have struggled with the "fragmentation" of ESG data, where different companies use different metrics to describe similar risks. The UK SRS, supported by platforms like Sweep, is expected to significantly reduce this friction.

Broader Implications for the UK Business Sector

The launch of the Sweep UK SRS solution is more than just a software update; it is an indicator of the "professionalization" of the sustainability sector. As the UK moves toward a mandatory regime, several long-term implications emerge for the business community:

1. The Rise of "Finance-Grade" ESG Data

The days of estimated or "proxy" data are coming to an end. Under UK SRS, companies will be expected to provide data that is as rigorous as their financial statements. This will likely lead to an increased role for Chief Financial Officers (CFOs) in the sustainability reporting process.

2. Competitive Advantage Through Transparency

Companies that can demonstrate a clear, data-backed path to net zero will likely enjoy a lower cost of capital. Investors are increasingly penalizing firms that lack transparency, viewing "data gaps" as unmanaged risks. Sweep’s solution allows firms to present a sophisticated, audit-ready profile to the market.

3. Supply Chain Pressure

As large listed companies begin to use Sweep’s supplier interfaces to gather data, smaller, non-listed companies in their supply chains will feel the pressure to track their own emissions. This "trickle-down" effect of regulation means that even firms not directly covered by the UK SRS will need to modernize their data practices to remain competitive as vendors.

4. Mitigating Greenwashing Risks

With mandatory standards and audit trails, the risk of "greenwashing"—making unsubstantiated environmental claims—is mitigated. The UK SRS provides a legal framework that makes companies accountable for their disclosures, and Sweep’s platform provides the evidence base to support those claims.

Conclusion

As the 2027 deadline for mandatory reporting approaches, the launch of Sweep’s UK SRS solution provides a necessary tool for the corporate sector to meet evolving regulatory expectations. By integrating AI, cross-framework compatibility, and rigorous audit features, the platform aims to transform sustainability reporting from a burdensome compliance exercise into a strategic asset. For UK-listed companies, the transition to the new standards will be a test of their data maturity and their commitment to transparency in an increasingly climate-conscious global market.