Few observers would have predicted that the often-contentious and high-stakes disputes between activist investors and publicly traded companies would increasingly culminate in something akin to a mutual agreement, or even a handshake. Yet, this paradoxical trend is becoming a notable feature of the corporate governance landscape. The growing prevalence and high-profile nature of informal settlements, even in the context of proxy contests, suggest a significant evolution in how these conflicts are resolved. This analysis, drawing from a memorandum by Sergi Corbatera, Founder and CEO of DEF 14 Inc., delves into the rise of these privately negotiated agreements and their implications.

Defining the Informal Settlement

An informal activist settlement, as defined by DEF 14 Inc., represents a privately negotiated resolution to disagreements between a company and an activist investor. These disputes can span a wide range of corporate matters, including strategic direction, governance structures, capital allocation policies, leadership changes, or the exploration of strategic alternatives. Crucially, unlike a formal settlement, an informal resolution is not typically codified in a publicly disclosed written agreement. Instead, its outcomes are often reflected through a series of public announcements, such as press releases or regulatory filings, detailing board appointments, specific commitments made by the company, and statements of support from the activist investor.

While the concept of informal settlements is not new, its prominence has been amplified in recent years. Earlier commentary, dating back to 2020, already identified them as an established, albeit selective, component of the activism ecosystem, particularly in larger and more constructive engagements where common ground could be found without the need for formal cooperation agreements. More recent analyses continue to highlight their efficacy in situations where companies and activists share a degree of strategic alignment and possess mutual trust, allowing public commitments—such as board seats, business reviews, or capital allocation adjustments—to substitute for the more stringent provisions of a formal contract.

The Impact of Universal Proxy Cards

The introduction of the universal proxy card has demonstrably reshaped the dynamics of settlement negotiations. Data and commentary from the past few years indicate a noticeable shift: an increase in the overall number of settlements, a reduction in the time taken to reach them, and a greater proportion of resolutions being achieved through private channels. Furthermore, there appears to be a sustained willingness among parties to settle rather than proceed to a shareholder vote. This environment has also fostered more operationally focused activist campaigns and has contributed to a more continuous, year-round activism cycle, characterized by off-cycle campaigns, "vote no" initiatives, and a growing trend of activists publicly launching campaigns without extensive prior engagement with the company.

Empirical Evidence: A Growing Trend

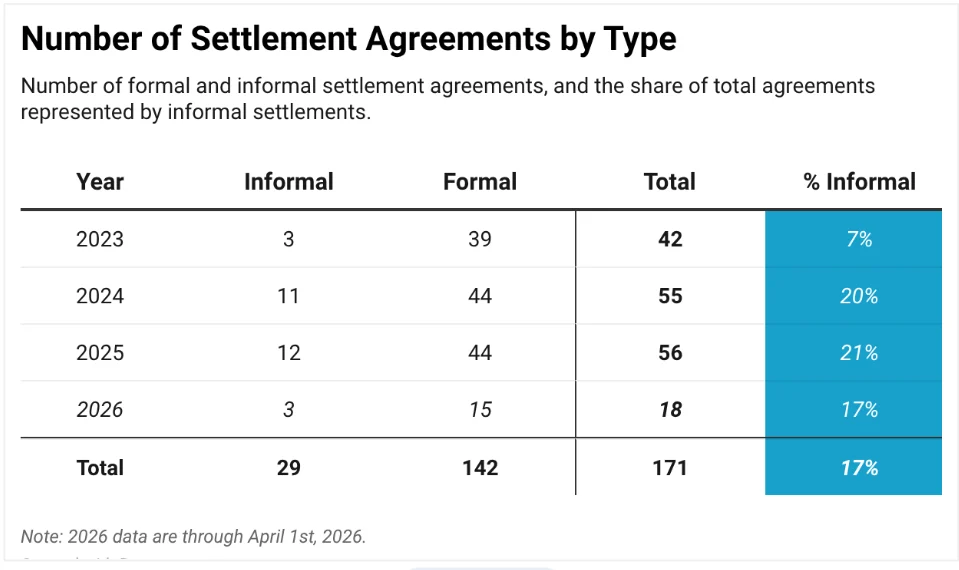

To understand this evolving landscape, DEF 14 Inc. undertook an empirical review of 646 activist campaigns initiated in 2023, alongside earlier campaigns that remained active and settled in 2023 or later. The analysis focused specifically on settlements that resulted in board representation, as these outcomes are most consistently observable through public disclosures.

The findings reveal a significant increase in informal settlements. Between 2023 and April 1, 2026, a total of 171 campaigns in the examined sample concluded with settlements that included board representation. Of these, a substantial 29 settlements, or 17%, were classified as informal. Examining this trend year by year, the share of informal settlements was 7% in 2023 (3 out of 42 campaigns), rose to 20% in 2024 (11 out of 55 campaigns), continued to climb to 21% in 2025 (12 out of 56 campaigns), and stood at 17% in the early part of 2026 (3 out of 18 campaigns).

Concentration Among Activist Firms

This surge in informal settlements is not uniformly distributed across the activist investor population. The DEF 14 Inc. sample indicates that while 74 distinct activist investors accounted for the 171 settlements involving board representation, only 18 of these investors were responsible for all the informal settlements observed. A striking concentration emerges when noting that nearly half of all informal settlements were attributable to just three activist firms, with one firm alone accounting for approximately 30% of the total.

Further analysis of the top 10 activists by the number of settlements (each achieving between four and 21 board seats) shows a divided approach: five of these leading activists utilized informal settlements, while the other five did not employ this strategy at all. This concentration strongly suggests that the adoption of informal settlements is, to a significant degree, a reflection of firm-specific strategies and preferences rather than solely a response to overarching market conditions.

Key Themes: Shareholder Choice and Board Authority

The increasing attention paid to the structure of activist settlements is underscored by ongoing litigation and commentary, which predominantly revolve around two interconnected themes: shareholder choice and board authority. The former concerns whether a settlement might effectively predetermine board composition before shareholders have had the opportunity to exercise their voting rights. The latter probes whether commitments made to an activist investor could potentially constrain the board’s independent decision-making or grant the activist undue influence over corporate affairs.

Landmark Litigation Shaping the Debate

Several significant Delaware court cases have become central to the discourse surrounding these settlement structures.

- Coster v. UIP: This case is frequently referenced in discussions concerning board actions and the principles of electoral fairness, highlighting the importance of transparent processes.

- West Palm Beach Firefighters’ Pension Fund v. Moelis & Co.: This case emerged as a crucial reference point for debates on the extent to which governance rights can be contractually shaped. The legal discussions surrounding it have continued to evolve following subsequent developments.

- Miller v. Crown Castle: This litigation brought similar issues into the spotlight within the specific context of activist settlements. In this instance, Crown Castle’s co-founder, Theodore B. Miller Jr., and Boots Capital challenged the company’s cooperation agreement with Elliott Investment Management. Following the company’s decision to grant Elliott board seats and related governance concessions, the lawsuit focused on whether a settlement reached shortly before the annual meeting, particularly in light of questions surrounding the activist’s economic exposure, could be viewed as improperly influencing the shareholder vote.

Collectively, these cases do not appear to have established a singular, definitive rule for all settlement scenarios. However, they have undeniably contributed to a heightened scrutiny of settlement structures. The ongoing dialogue increasingly questions whether a settlement preserves the board’s fiduciary duty to exercise independent judgment, whether influence granted is tied to a clear and demonstrable economic stake, and whether the integrity of the shareholder electoral process is respected.

Tradeoffs in the New Activism Playbook

The evolving landscape necessitates that both activist strategies and the scope of concessions offered by companies are increasingly shaped by a careful balancing of several variables. These include:

- Tolerance for Litigation Risk: Companies must assess their willingness to endure potential legal challenges arising from settlement terms.

- Choice of Investment Instruments: The nature of an activist’s economic exposure (e.g., direct stock ownership versus derivatives) can influence the perceived legitimacy of their demands.

- Willingness to Depart from Ordinary Governance Structures: Companies must decide how far they are willing to deviate from established governance norms to reach an agreement.

- Timing Relative to the Proxy Process: The proximity of a settlement to the annual meeting can significantly impact its perceived fairness and legality.

- Contractual Flexibility: The advantages of avoiding formal agreements, which can offer greater flexibility, are weighed against the potential for ambiguity.

- Practical Benefits: The allure of lower costs, reduced process, and greater speed associated with informal settlements is a significant factor.

Speed and Substance: A Closer Look

DEF 14 Inc.’s data suggests that informal settlements are, on average, reached more quickly. However, this difference in speed diminishes when exceptionally long-running campaigns are excluded from the analysis. For campaigns concluding with board representation between 2023 and 2026, the average time from the first public disclosure of the campaign to settlement was 79 days for informal settlements, compared to 88 days for formal settlements, after excluding campaigns exceeding 365 days. The gap was more pronounced in 2024 and 2025, where informal settlements were concluded 38 and 25 days sooner, respectively.

Despite this speed advantage, the data does not reveal equally clear differences in other observable aspects of the settlements. Beyond the defining contractual provisions of formal agreements—such as standstill clauses, minimum ownership thresholds, and similar stipulations—informal settlements do not appear materially distinct from their formal counterparts in other examined dimensions. This holds true for the seasonality of settlements, where the annual pattern for informal resolutions largely mirrors that of formal settlements. Similarly, the representation of activist principals on boards shows little divergence; in approximately one out of every three settlements in both subsets, at least one fund employee or principal joined the board.

However, a notable distinction emerges in the scale of board representation. Informal settlements accounted for 17% of all settlements but only 13% of the total board seats secured. This implies an average of 1.4 seats per informal settlement, compared to 1.9 seats per formal settlement. The data suggests that greater board representation, in this sample, was more frequently achieved through formal settlement agreements.

The Role of Private Engagement

The analysis also indicates a modestly higher proportion of informal resolutions among campaigns that remained private until settlement and were disclosed only at that juncture. While the margin is not substantial enough to draw definitive conclusions, this trend aligns with prior commentary observing an increase in private settlements in the era of universal proxy cards. This is further supported by the notion that constructive, trust-based engagements provide a fertile ground for workable informal arrangements.

One plausible explanation for this phenomenon, though not definitively proven by the current data, is that when activists do not need to escalate to public campaigns and companies engage constructively, a sufficient level of trust and alignment may develop, rendering a detailed public agreement unnecessary. Another potential factor relates to the nature of the activist’s economic exposure. Commentary surrounding the Miller v. Crown Castle case, for instance, has highlighted the scrutiny that can arise when governance rights are granted to investors whose stakes are partially held through derivatives or other less transparent instruments. At this stage, these remain hypotheses warranting further empirical investigation.

Conclusion: A Strategic Evolution

The rise of informal settlements in shareholder activism signifies a strategic evolution in how disputes are managed. While offering potential benefits of speed and reduced process, these resolutions are increasingly subject to legal and governance scrutiny. The interplay between shareholder rights, board independence, and the practicalities of reaching swift agreements continues to define this dynamic and evolving area of corporate governance. The data presented by DEF 14 Inc. provides a crucial empirical foundation for understanding these shifts and anticipating future trends in activist engagements.