The private equity landscape is undergoing a significant transformation, driven by a pronounced thirst for liquidity that is reshaping how investors and fund managers approach asset realization. In an era marked by challenges in the traditional dealmaking environment, private equity assets, once perceived as a stable long-term investment, are increasingly revealing their inherent illiquidity. This friction is manifesting in a notable slowdown in distributions, impacting both Limited Partners (LPs) and General Partners (GPs) and propelling the rise of innovative transaction structures, most notably continuation vehicles (CVs).

The Liquidity Squeeze Intensifies

The period between 2022 and 2024 has witnessed a stark deviation from historical norms in private equity distributions. Data indicates that distributions as a percentage of Net Asset Value (NAV) have trailed previous benchmarks by approximately 15%, settling around 13% compared to a historical average closer to 28%. This shortfall directly affects the Distributions to Paid-In Capital (DPI) metric, a key indicator of realized returns. For fund vintages from 2018 to 2021, the DPI is reported to be 0.2 times lower than initially projected, creating significant liquidity pressure across the private markets ecosystem.

The heightened focus on liquidity is palpable among LPs. A 2025 survey by McKinsey highlighted a dramatic shift in investor sentiment, with 2.5 times more LPs ranking DPI as the "most critical" performance metric compared to three years prior. This signifies a move from valuing potential future growth to demanding tangible cash returns in the present.

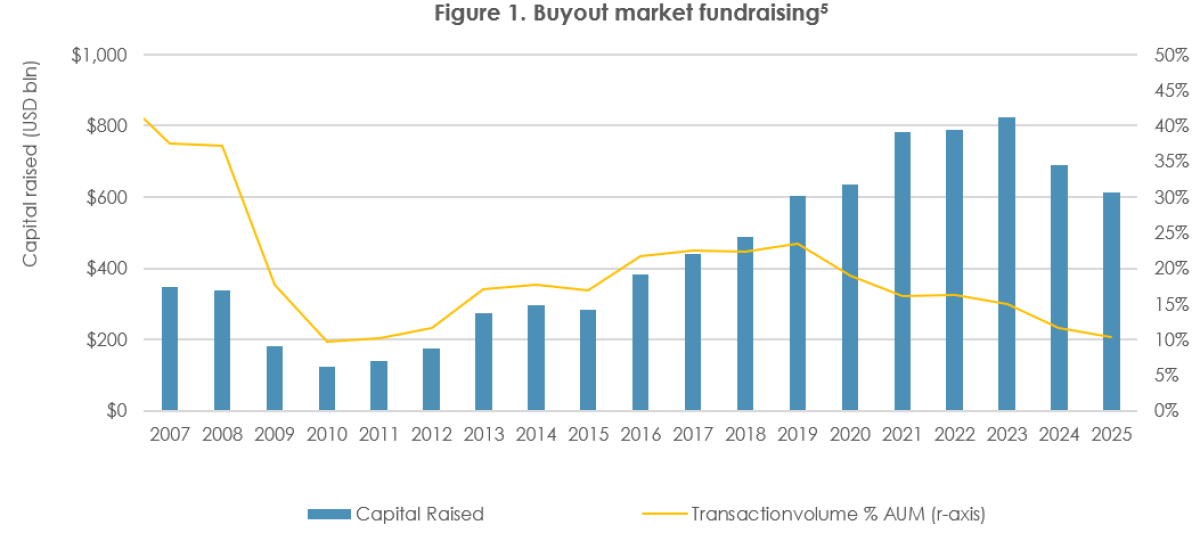

GPs are equally attuned to this liquidity drought. The challenges in distributing capital back to LPs have, in turn, created headwinds in their fundraising efforts. With LPs’ private markets exposure remaining elevated due to slower distributions, their appetite for new capital commitments has waned, leading to a more selective allocation process. The current fundraising environment is characterized by a stark imbalance: for every $3 of targeted fundraising, only $1 of capital is currently available for commitment. This ratio, historically around 1.3:1, underscores the significant contraction in deployable capital. Last year, buyout fund fundraising relative to NAV reached its lowest point since the Global Financial Crisis, a clear indicator of the prevailing market conditions.

The Secondary Market as an Oasis

Against this backdrop of constrained exit markets and reduced distributions, the secondary private equity market has experienced rapid expansion. Initially established to provide liquidity to LPs seeking to divest their holdings, the secondary market has evolved into a vital source of capital for GPs as well. Increasingly, GPs are turning to GP-led secondary transactions to unlock liquidity and manage their portfolio exposure, particularly when traditional exit avenues, such as IPOs or trade sales, are unviable.

Continuation Vehicles Emerge as Dominant Structure

Within the burgeoning secondary market, continuation vehicles (CVs) have rapidly ascended to become the dominant transaction structure. These vehicles allow GPs to buy out existing investors from a fund at a predetermined valuation, offering immediate liquidity while retaining ownership and management of select, high-conviction assets. This mechanism effectively "rolls over" the assets into a new vehicle, allowing the GP to continue to manage and grow them, often with a longer investment horizon than permitted by the original fund’s lifecycle.

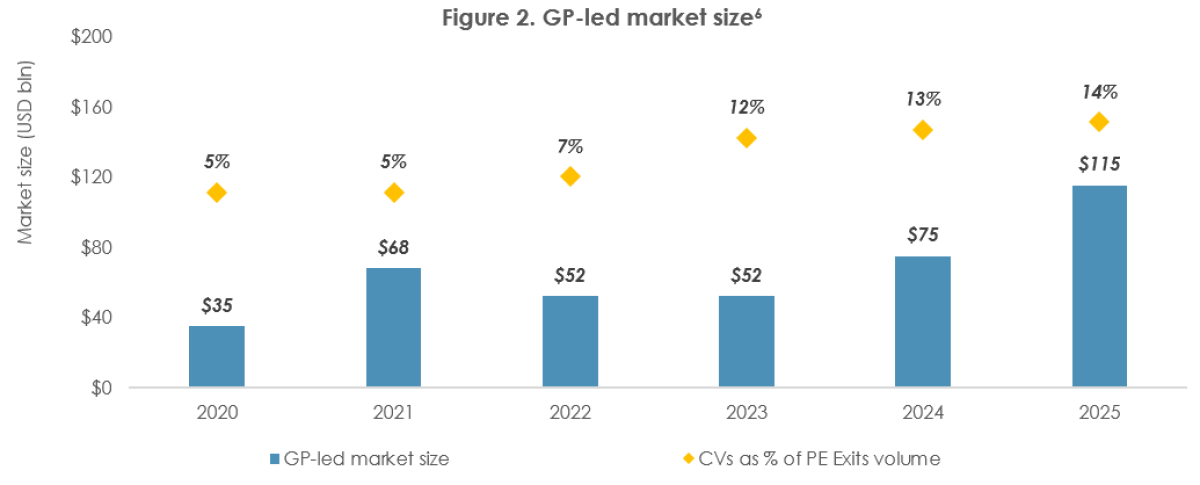

The scale of this trend is substantial. In 2025 alone, GP-led secondary transaction volume reached an estimated $115 billion. Continuation vehicles accounted for a significant majority of this activity, representing 89% of GP-led volume and approximately 43% of the total secondary market volume. This surge reflects not only a greater reliance on secondary solutions in challenging exit markets but also a potential structural shift in how private equity exits are conceived and executed.

The adoption of GP-led CVs has broadened significantly across the industry. Nearly 75% of the largest global private equity firms have participated in at least one continuation transaction, signaling widespread acceptance and utilization of this strategy. Furthermore, the investor base for CVs has diversified considerably. Beyond traditional secondary funds, direct LP investments and evergreen vehicles are increasingly participating. Continuation fund syndications have become more commonplace, capturing the largest share of LP direct secondary investments in the first half of 2025. These developments collectively indicate that continuation vehicles have become an integral component of private equity liquidity management, fundamentally reshaping liquidity options for both LPs and GPs.

Diversification of Continuation Vehicle Structures

The continuation vehicle market has further evolved into two distinct structures: multi-asset continuation vehicles (MACVs) and single-asset continuation vehicles (SACVs). MACVs are often employed to facilitate liquidity across a broader range of a fund’s remaining assets, sometimes as part of a fund wind-down process. SACVs, on the other hand, are typically utilized for "trophy" assets—individual, high-conviction companies that sponsors believe have significant remaining value creation potential and that they wish to retain beyond the original fund’s life.

Empirical evidence suggests a performance differentiation between these structures. SACVs are generally associated with stronger asset performance and higher valuation metrics compared to MACVs. This distinction is reflected in their pricing, with SACVs commanding higher valuations. The shift towards single-asset exposure in SACVs necessitates a change in the required skillset from investors, moving from manager selection to a more direct underwriting of the underlying asset’s value and future prospects. This evolution also expands the potential for conflicts of interest, which warrants careful examination.

Navigating Conflicts of Interest

The widespread adoption of continuation vehicles, while offering significant liquidity solutions, also introduces potential conflicts of interest that demand close scrutiny. These conflicts arise from the GP’s dual role as both the seller and the manager of the assets within the continuation vehicle.

For General Partners (GPs):

- Valuation Discrepancies: GPs are tasked with determining the valuation of the assets being transferred into the CV. This presents a conflict as they are incentivized to set a valuation that is attractive to new investors while also providing sufficient liquidity to existing LPs. This can lead to a scenario where the GP negotiates a valuation that may not fully reflect the optimal outcome for all parties involved.

- Information Asymmetry: GPs possess superior information regarding the portfolio companies compared to potential new investors or the existing LPs considering rolling over their capital. This asymmetry can be exploited to the GP’s advantage, particularly during the valuation and negotiation phases.

- Fee Structure Alignment: The fee structure of the continuation vehicle may differ from the original fund, potentially creating incentives for GPs to retain assets longer than optimal for existing LPs if it leads to higher management fees or performance fees for the GP.

- Distribution Prioritization: GPs may face pressure to prioritize distributions to existing LPs to facilitate the transaction, potentially at the expense of reinvesting capital for further value creation within the CV if that capital could otherwise be utilized more effectively for the benefit of all stakeholders.

From an LP perspective, these conflicts can be partially mitigated through robust independent valuations, adequate review periods for transaction documents, and the reinvestment of crystallized carried interest by the GP. However, LPs must ultimately rely on the sponsor’s discipline to ensure that the implementation of value-creation initiatives is not delayed for opportunistic reasons.

For Limited Partners (LPs):

- Compressed Decision Timelines: LPs often experience compressed timelines in GP-led processes. The need for additional re-underwriting and asset diligence required by LPs to assess "sell-or-roll" requests across multiple funds can be challenging within tight deadlines. GPs aim to execute transactions efficiently, but this can limit the depth of review LPs can perform, particularly for those without dedicated expertise in deal underwriting.

- Forced Liquidity Decisions: Short decision windows can force LPs to make critical choices between immediate liquidity and the potential for future, albeit uncertain, returns. This can lead to LPs exiting positions at less-than-optimal valuations simply to meet the transaction deadlines.

- Altered Risk/Return Profiles: Continuation vehicles significantly alter the traditional risk and return profile of secondary exposure. Single-asset continuation vehicles, in particular, shift secondaries away from diversified, shorter-duration portfolios towards more concentrated positions with extended holding periods. This change weakens historical portfolio characteristics that have underpinned secondary allocations, challenging their traditional role as a source of early liquidity and diversification.

- Reduced Diversification and Slower Distributions: Consequently, LPs face lower diversification benefits, slower distributions, and less countercyclical protection due to the potential for elevated discounts in CV transactions compared to traditional secondary sales.

Broader Portfolio Implications and Future Outlook

As continuation vehicles become increasingly embedded within private markets, their impact extends to a portfolio’s overall liquidity profile. Within buyout strategies, CVs have served as an additional liquidity mechanism when traditional exit routes are constrained. However, transaction pricing in continuation vehicles is often skewed below prior reported NAV. This can result in realized returns at levels below prior valuation assumptions when compared to a traditional exit. Furthermore, by extending asset holding periods, continuation vehicles alter the liquidity characteristics of secondary investments. This has significant implications for cash management, as slower distributions can exacerbate the already limited liquidity of primary private equity investments. The era of assuming shorter holding periods and early liquidity in secondary investments is evolving.

Conclusions: A Structural Shift or a Temporary Patch?

Continuation vehicles have undeniably reshaped the private markets landscape by establishing a new, viable exit route for sponsors. In periods of constrained exit markets, GP-led transactions have provided a crucial mechanism to generate liquidity and manage portfolio exposure, accounting for approximately 14% of exits during 2025. This has facilitated deal execution when traditional exits have been more challenging to realize.

However, this structural shift also introduces complexities that warrant careful consideration. Continuation vehicles are increasingly extending asset holding periods beyond the original fund mandate, blurring the economic boundaries of closed-ended structures. This challenges both the traditional role of secondaries within a diversified portfolio and the long-held assumptions around liquidity embedded in private market allocations. As a result, LPs are increasingly required to revisit their strategic asset allocation assumptions to reflect potentially longer value creation timelines and altered liquidity profiles.

For GPs, continuation vehicles must be treated as a clearly defined component of their exit toolkit, not a perpetual solution. This necessitates transparency regarding when a CV is preferred over traditional exit routes and how such decisions align with predetermined value creation objectives. Accordingly, LPs must rigorously assess how GPs incorporate continuation vehicles into their investment and exit frameworks and what this implies for expected liquidity timing. While continuation vehicles have undoubtedly supported deal execution and liquidity under difficult market conditions, their broader implications for portfolio construction and investor expectations demand careful and ongoing management. The long-term impact of this evolution will depend on the continued discipline and transparency of all market participants.