The investment landscape for both institutional investors and individual wealth management clients has undergone a significant transformation over the past decade, marked by a substantial increase in allocations to alternative assets. Private debt and infrastructure, once niche segments, are now prominent components of diversified portfolios. This trend is further propelled by regulatory shifts, such as the introduction of European Long-Term Investment Funds (ELTIFs) and governmental initiatives in the United States aimed at broadening access to private investments for retirement plans. Investors are drawn to these private markets by the allure of higher expected risk-adjusted returns and unique opportunities for sustainable investing. However, this embrace of private assets introduces a new layer of complexity, particularly in the management of liquidity risk.

The growing prominence of illiquid assets, defined by their limited trading volume and the absence of readily available secondary markets, presents a unique set of challenges that impact every stage of the investment process. These challenges extend from initial asset-liability management (ALM) studies to the day-to-day operational realities of managing a portfolio. Understanding and proactively addressing illiquidity risk is no longer an optional consideration but a critical imperative for asset owners seeking to maintain portfolio integrity and achieve their long-term financial objectives.

The Multifaceted Nature of Illiquidity Risk

The core of illiquidity risk stems from the inherent difficulty in quickly converting an asset into cash without a significant loss in value. This manifests in several interconnected ways, each posing a distinct threat to portfolio management.

Uncertainty in Cash Flows and Capital Calls: The absence of deep secondary markets and the protracted nature of purchase and sale processes for illiquid assets create a fundamental uncertainty surrounding the timing and magnitude of expected cash receipts and capital calls. For asset owners, this can lead to suboptimal portfolio allocations. A miscalculation of the timing of capital calls might result in an over-allocation to illiquid assets, tying up more capital than anticipated. Conversely, a delay in distributions can leave an investor with insufficient liquidity to meet obligations or to take advantage of new investment opportunities. This uncertainty can also hinder an investor’s ability to de-risk the portfolio when market conditions warrant, as the sale of illiquid assets may be slow or come at a steep discount.

Constrained Rebalancing and the Denominator Effect: A significant portion of illiquid assets within a portfolio inherently limits an investor’s flexibility to rebalance across asset classes. In periods of market volatility, especially during significant downturns like those experienced in 2022, the value of liquid assets can plummet. This "denominator effect" causes the proportion of illiquid assets in the portfolio to increase disproportionately, even without any new investment in these assets. Investors with a high duration exposure, such as pension funds heavily invested in fixed income, are particularly vulnerable. If the ability to rebalance is constrained by the illiquidity of other assets, the portfolio can deviate substantially from its strategic asset allocation targets, potentially exposing the investor to unintended risks. For instance, a pension fund aiming for a 60/40 stock/bond split might find its illiquid holdings ballooning to 30% of the total portfolio value during a market shock, leaving it with a significantly higher risk profile than intended.

Model Risk and Stale Pricing: The valuation of illiquid assets often relies on complex models due to the lack of real-time market pricing. This introduces model risk, where the estimated value may not accurately reflect the true market value that could be achieved in an arm’s-length transaction. Consequently, asset prices might not immediately reflect underlying impairments. This phenomenon, known as "stale pricing," means that the reported volatility of illiquid asset classes tends to be lower than that of comparable liquid investments, and their prices often lag behind broader market movements. This makes it challenging to apply traditional risk measures and accurately assess correlations with other asset classes. Evaluating the true risk exposure requires a greater reliance on qualitative judgment and a deep understanding of the underlying assets.

Information Asymmetry and Transparency Gaps: Information regarding individual illiquid investments is frequently proprietary and not publicly disseminated. This lack of transparency makes it difficult for asset owners to assess the quality of their holdings, especially when external asset managers act as intermediaries. The bankruptcy of entities like First Brands Group, which revealed significant off-balance sheet liabilities to some private market lenders, serves as a stark reminder. In such scenarios, asset owners cannot solely depend on asset managers for timely and accurate information about loan quality. Demanding greater transparency beyond standard reporting packages can be challenging, particularly when investing with established managers who manage large and complex strategies.

Strategic Approaches to Mitigate Illiquidity Risk

Navigating the complexities of illiquid assets requires a proactive and multifaceted approach that integrates risk management considerations into every stage of the investment lifecycle.

Integrating Illiquidity into Asset-Liability Management (ALM) Studies

The ALM process is the foundational step for any asset owner and must explicitly account for the unique characteristics of illiquid assets. Traditional risk metrics and correlations derived from liquid markets can be misleading when applied to illiquid investments due to stale pricing.

Enhanced Optimization and Constraints: In unconstrained optimization models, the artificially low volatility and correlation of illiquid assets might lead to allocations that carry far greater risk than suggested by the data. To counter this, implementing constraints within the optimization process is crucial. This can involve setting maximum allocation limits for specific asset classes or groups of assets. Stress testing is an invaluable tool in setting these limits. For instance, an ALM study might demand that the proportion of illiquid assets does not exceed a predetermined threshold even after factoring in the impact of rising interest rates or a significant downturn in liquid markets.

Liquidity Premiums and Penalties: Incorporating a "liquidity penalty" into the optimization function can effectively adjust for the inherent illiquidity. This can be achieved by deliberately increasing the perceived risk measures of illiquid asset classes beyond what historical data might suggest, or by introducing a specific penalty factor that weighs against their inclusion alongside traditional risk and return measures. Furthermore, enforcing greater portfolio diversification can be achieved by penalizing concentration risk, particularly relevant in private markets where manager dispersion can be high.

Proxying Correlations and Risk Metrics: In the absence of direct, real-time data, asset owners can leverage comparable liquid asset classes to proxy the behavior of illiquid ones. For example, the correlation of direct lending spreads with single-B rated high-yield bond spreads and senior bank loan spreads can be estimated over a suitable horizon, such as one year. The correlation of direct lending with other asset classes, like equities, can then be derived from the correlation between high-yield bonds and equities. This approach provides a more grounded estimation of risk and diversification benefits.

Liquidity Stress Testing: A critical component of ALM studies should be comprehensive liquidity stress testing. Asset mixes must be sufficiently liquid to withstand stressed market conditions. This is particularly pertinent for investors with long-duration interest rate or inflation derivative portfolios, which require liquid collateral to meet margin calls during adverse rate movements. Defining a clear "liquidity waterfall" and applying haircuts to simulate forced selling under stressed circumstances is best practice. The 2022 UK Gilt crisis, which saw even highly illiquid assets like private equity experience rapid selling albeit at deep discounts, underscores the importance of preparing for such scenarios.

Strategic Implementation and Cash Flow Planning

The long-term nature and illiquid characteristics of private market investments necessitate a robust implementation strategy that extends beyond initial allocation decisions.

Phased Capital Deployment and Distribution Planning: Since private market allocations cannot be adjusted rapidly, investors must have a well-defined plan for building, maintaining, and adjusting their exposure. This includes a clear understanding of how much capital should be deployed annually (vintage year planning) and realistic projections for capital distributions. This forms a crucial element of liquidity planning, ensuring the capacity to meet capital calls and other potential payments, such as pension disbursements. The objective is to minimize the probability of becoming a forced seller during periods of market stress, when redemptions may be subject to significant fees, penalties, and gating mechanisms.

Scenario Analysis and Cash Flow Stress Testing: The inherent difficulty in precisely forecasting capital deployment and repayment timelines in private markets requires robust scenario analysis. Investors, much like those in private equity who are currently experiencing challenges in repatriating capital due to changing market conditions, must supplement estimates from asset managers with their own stress testing and scenario analysis on expected cash flows. A second layer of implementation strategy involves acknowledging in ALM studies that illiquid asset class exposure will naturally deviate from targets. Stress testing the asset mix under scenarios where both portfolio ramp-up and distributions are significantly above and below target is crucial.

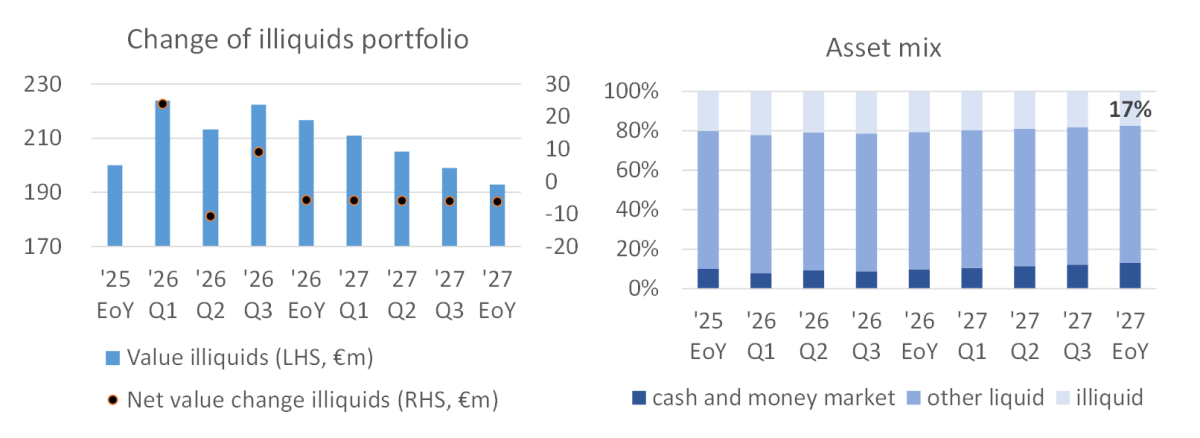

Consider a hypothetical EUR 1 billion balance sheet where 20% is allocated to illiquid investments. At the end of 2025, expected distributions from existing illiquid assets are projected to exceed upcoming capital calls, leading to a projected allocation of 17% by the end of 2027. In early 2026, a decision is made to commit an additional EUR 40 million, with capital expected to be called over the subsequent eight quarters.

If distributions proceed as anticipated, the illiquid allocation will return to the target 20% by the end of 2027. However, if these planned distributions are delayed by a year, the allocation by the end of 2027 could exceed the target by 3% (reaching 23% instead of the anticipated 20%). This illustrates how unexpected delays in cash inflows can significantly alter the portfolio’s composition and risk profile.

While there is no perfect solution to the inherent unpredictability of external market developments influencing capital deployment decisions, careful planning and the maintenance of adequate liquidity buffers through stress testing can effectively manage the associated risks.

Strengthening the Operational Framework

The operational demands of managing illiquid alternative assets are substantial and extend beyond quantitative modeling.

Appropriate Staffing and Resources: The investment team and back-office personnel must be adequately staffed and possess the requisite expertise to handle the complexity of illiquid portfolios. This may necessitate leveraging external partners such as specialized investment consultants and reporting services. Organizations need robust systems and sufficient personnel to manage pending capital calls and other administrative burdens. A larger asset base or significant internal resources can facilitate the management of more complex portfolios. A guiding principle should be to align the asset allocation strategy with the organization’s size and available team resources, building additional capacity incrementally as needed.

Diligent Manager Selection and Diversification: The dispersion of manager performance in illiquid asset classes is often pronounced, making manager selection even more critical than in traditional asset classes. Investment organizations must invest considerable time in designing a rigorous manager selection process. Diversification within illiquid asset classes is also paramount, encompassing dimensions such as manager selection, sector focus, and vintage year. This layered approach to diversification helps mitigate manager-specific risks and smooth out the impact of market cycles.

Conclusion

The sustained increase in allocations to alternative assets over the past decade has undeniably led to more complex and illiquid investment portfolios for both institutional investors and private wealth clients. For asset owners, developing a profound understanding of their specific liquidity needs is paramount. This clarity will enable them to define appropriate allocations to illiquid asset classes within their strategic asset allocation framework.

During the implementation phase, meticulous liquidity planning and investment planning are indispensable for effectively building these asset classes and managing cash flows. Within the realm of illiquid investments themselves, diligent manager selection and diversification across multiple dimensions are the cornerstones for mitigating selection risk. By embracing these principles, asset owners can navigate the challenges of illiquidity, transforming potential pitfalls into opportunities for enhanced risk-adjusted returns and more resilient portfolios.

Andreas Rothacher, CFA, CAIA, serves as the Head of Investment Research at Complementa AG, where he guides institutional clients on strategic asset allocation and manager selection. He is also a co-author of Complementa’s annual Swiss pension fund study and has authored numerous articles. Mr. Rothacher leads the CAIA Zurich Chapter and is a member of the CFA Swiss Pensions Conference Committee. His prior experience includes roles at a German family office and at UBS and Credit Suisse.

Richard Sanders, CFA, is the Head of Asset Allocation and Manager Selection at Coöperatie VGZ. With extensive experience in asset allocation, particularly in fixed-income portfolios for institutional investors, he has advised sovereign wealth funds, pension funds, and insurance companies on manager selection and asset allocation strategies. He also managed the liquid investments for NN Group.

To learn more about the CAIA Association and to join a professional network shaping the future of investing, please visit caia.org.