Global semiconductor job postings cooled in April 2026 after a significant surge in the first quarter, with a 6.6% month-on-month decline, signaling a nuanced shift in investment priorities and a recalibration of strategic focus within the industry. This moderation, while notable, does not represent a return to earlier lows, indicating sustained underlying demand for specialized talent and evolving market needs. For company leaders and investors, these granular hiring patterns serve as an invaluable early warning system, illuminating where innovation is being directed, which markets are experiencing growth or contraction, and where competitive advantages are being forged long before financial statements reflect these underlying currents.

The semiconductor industry, a bedrock of the global digital economy, is characterized by rapid technological advancement and substantial capital investment. Understanding the ebb and flow of its talent acquisition is paramount to deciphering future market trajectories. The data from April 2026, as analyzed by GlobalData Jobs Analytics, reveals a complex interplay of factors influencing hiring decisions, from the pervasive influence of Artificial Intelligence (AI) and cloud computing to geographical shifts in manufacturing and research, and the specific technical skills that are most in demand.

The April 2026 Hiring Landscape: A Snapshot of Momentum

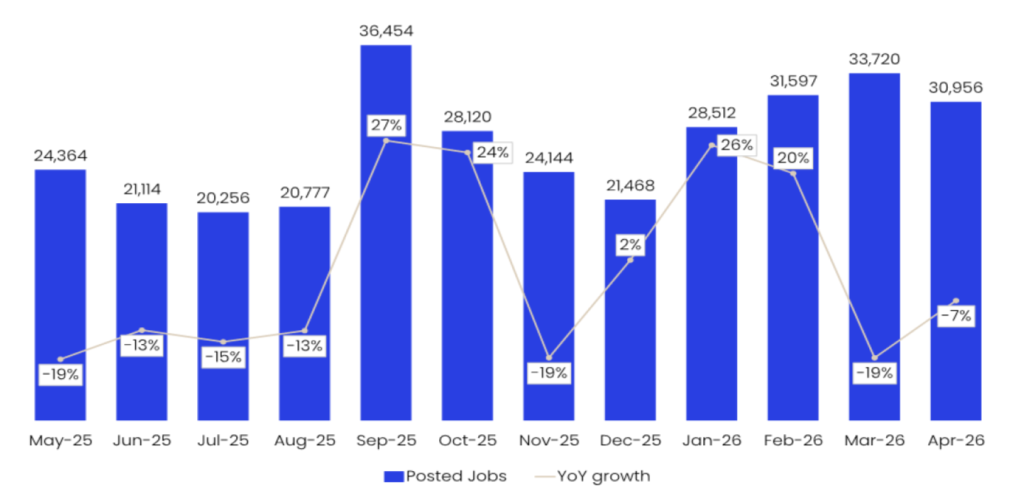

Global semiconductor job postings experienced a dip in April 2026, falling by 6.58% to reach 30,956. This marked the second consecutive monthly decline, following a robust acceleration observed in January and February of the same year. The hiring landscape over the preceding twelve months has been characterized by volatility, with notable upswings in September 2025 and again in the early months of 2026, followed by a period of consolidation in March and April. Despite the recent pullback, the overall posting levels remain higher than the baseline recorded in December 2025, suggesting a sustained, albeit moderated, hiring run-rate compared to the latter half of 2025. This trend indicates a cooling of momentum rather than a significant retrenchment to earlier trough levels.

This dynamic hiring environment underscores the critical importance of real-time workforce data. Such analytics provide a forward-looking perspective, enabling leaders to anticipate market shifts and adjust their strategic investments accordingly. The ability to identify which roles, skills, and geographic regions are attracting increased attention from companies offers a competitive edge, allowing for proactive adjustments to product development, market penetration, and talent acquisition strategies. The window of opportunity for acting on these hiring signals is typically one to three months; by the time broader market consensus forms, the underlying trends may have already evolved.

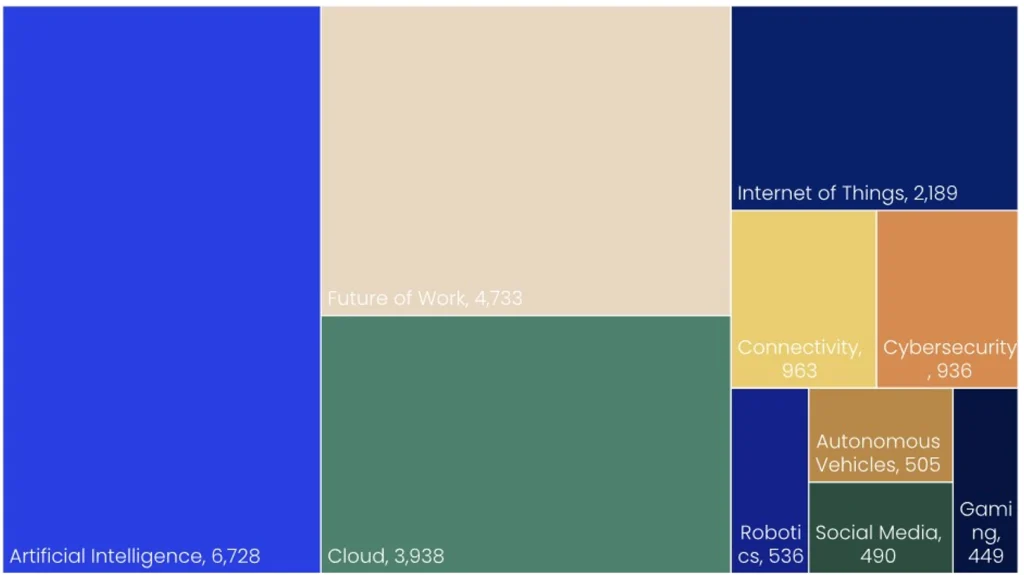

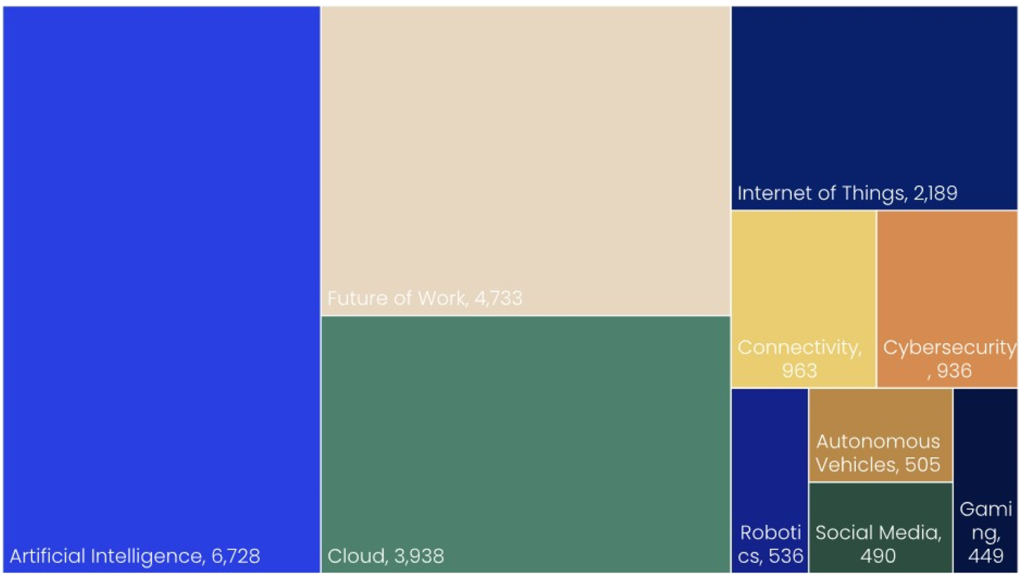

Dominance of AI and Cloud: Shaping the Demand for Semiconductor Talent

A detailed examination of the thematic focus within semiconductor job postings reveals a clear concentration of investment in areas intrinsically linked to digital transformation and advanced computing. Artificial Intelligence (AI) emerged as the dominant theme in April 2026, accounting for 6,728 job postings. This surge in AI-related roles reflects the ongoing race to develop more sophisticated AI hardware, algorithms, and applications, from advanced neural network processors to specialized AI accelerators. The demand for engineers and researchers skilled in AI is driven by the transformative potential of this technology across virtually every sector, including autonomous systems, personalized medicine, and advanced analytics.

Following closely behind AI, the "Future of Work" (FOW) theme garnered significant attention, with 4,733 postings. This theme encompasses a broad range of roles and initiatives aimed at leveraging technology to enhance productivity, collaboration, and workforce flexibility. In the context of semiconductors, this likely translates to demand for talent involved in developing the underlying technologies that enable remote work, augmented reality-based training, and intelligent automation within workplaces.

Cloud computing, a foundational pillar of modern digital infrastructure, also ranked prominently, with 3,938 job postings. The continued growth of cloud services, both public and private, necessitates the development and refinement of the semiconductor components that power these vast data centers. This includes demand for expertise in high-performance computing, specialized memory technologies, and energy-efficient chip designs essential for scalable cloud operations.

Beyond these top three themes, secondary areas such as the Internet of Things (IoT) and connectivity saw substantial, though comparatively smaller, hiring volumes, with 2,189 and 963 postings respectively. The significant drop-off in postings beyond the top themes highlights a strategic narrowing of focus, with resources being disproportionately channeled into AI, FOW, and Cloud. Niches such as robotics, autonomous vehicles, and gaming, while critical emerging markets, currently represent a comparatively limited portion of the overall hiring demand within the semiconductor sector, suggesting that investment in these areas may be more nascent or focused on specific, highly specialized R&D initiatives.

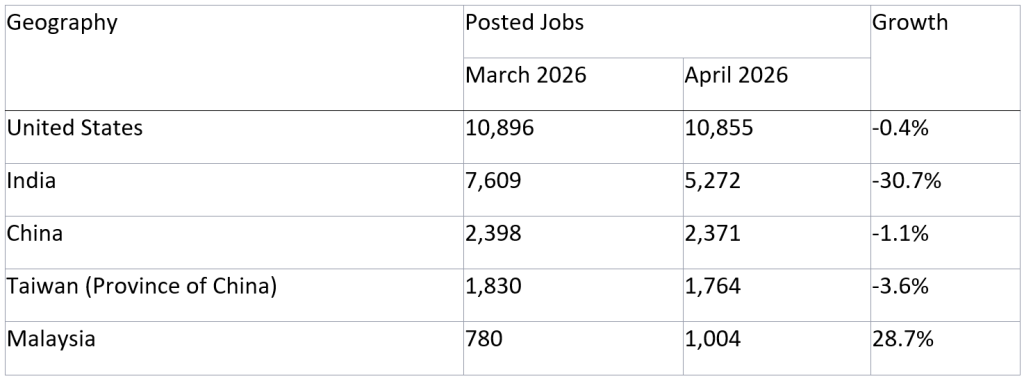

Geographic Distribution: The US Leads, with Shifting Dynamics Elsewhere

The United States maintained its position as the preeminent hub for semiconductor hiring in April 2026, with its hiring market remaining relatively stable, experiencing only a marginal decline of 0.4% compared to March. This stability in the largest market underscores its continued importance in semiconductor innovation, manufacturing, and research and development.

However, other key regions exhibited more pronounced shifts. India experienced the steepest month-on-month contraction, with a significant decrease of 30.7% in job postings. This sharp decline, while notable, could reflect seasonal hiring patterns, project completions, or a strategic reallocation of resources within global talent acquisition strategies. China and Taiwan, also critical centers for semiconductor manufacturing and design, saw modest declines of 1.1% and 3.6% respectively. These slight contractions may indicate a period of recalibration or a strategic shift in focus within these established semiconductor ecosystems.

In contrast, Malaysia emerged as a significant growth area, with job postings surging by an impressive 28.7% to reach 1,004. This substantial increase positions Malaysia as a key positive mover within the observed geographic landscape. Such growth could be attributed to new manufacturing investments, expansion of existing facilities, or a strategic effort to diversify global supply chains, making it an increasingly attractive location for semiconductor operations. Overall, April’s geographic hiring profile depicts a landscape of relative stability in major markets, coupled with dynamic and varied growth rates in other regions, reflecting a complex and evolving global supply chain and talent pool.

Employer Momentum: A Mixed Picture Amidst Evolving Strategies

The hiring momentum among the top semiconductor employers in April 2026 presented a mixed picture, reflecting diverse strategic priorities and the ongoing recalibration of workforce needs. IBM remained the largest single job poster in April, with 4,248 postings. However, this figure represented a material decrease from its peak in February, which saw 9,517 postings, and also a decline from March’s figures. This softening in IBM’s hiring activity contributed to a general deceleration in overall top-employer hiring momentum.

Hitachi demonstrated relative stability, maintaining an elevated level of hiring with 2,300 postings in April, a marginal decrease from 2,317 in March. This consistency suggests a sustained commitment to expanding its workforce in key areas. Several other companies also reported moderate increases in their April job postings. Qualcomm, for instance, saw its postings rise to 1,203, indicating continued investment in its core semiconductor design and development capabilities. Huawei also posted an increase, reaching 917 roles, suggesting ongoing efforts to bolster its technological capacity despite geopolitical considerations.

Conversely, some established players experienced a decline in their hiring activities. Jabil’s job postings decreased to 1,360, and Applied Materials saw a reduction to 904. These fluctuations could be indicative of project-specific hiring cycles, the completion of major recruitment drives, or a strategic reassessment of immediate talent needs.

A particularly noteworthy development was Infineon Technologies’ entry into the top-employer list in April, with 751 postings. This is especially significant given the company had zero postings in January, February, and March. This substantial month-specific shift suggests a new strategic initiative, a significant project launch, or a rapid expansion of operations that requires a swift influx of specialized talent. The varied hiring trends among leading companies underscore the dynamic nature of the semiconductor industry, where strategic decisions, market conditions, and technological advancements constantly reshape workforce requirements.

Core Technical Skills in Demand: Engineering the Future

The demand for specific technical skills within the semiconductor sector in April 2026 highlighted a strong emphasis on foundational engineering and integration capabilities. Application Platforms and Containers emerged as the most sought-after technical skill area, with 4,960 job postings. This indicates a significant need for professionals adept at developing, deploying, and managing software applications and their underlying infrastructure, particularly in cloud-native environments. The increasing complexity of semiconductor design and manufacturing processes necessitates robust platform engineering and efficient deployment mechanisms.

Systems Design and Integration followed closely, with 3,637 postings. This reflects the critical requirement for engineers who can conceptualize, architect, and seamlessly integrate complex semiconductor systems. As chips become more intricate and integrated with various functionalities, the ability to manage these complex interdependencies is paramount. Operating Systems (3,408 postings) also ranked highly, underscoring the persistent demand for expertise in the fundamental software layer that manages hardware resources. This is crucial for developing efficient and reliable semiconductor operations across a wide range of applications.

The remaining top technical skills included enterprise application domains, such as Application Lifecycle Management and HR/Payroll applications. The inclusion of these business systems indicates a broadening of the skill sets required within the semiconductor sector, extending beyond core engineering to encompass the IT infrastructure and support systems that enable efficient business operations. This suggests a need for a holistic approach to talent acquisition, recognizing that both highly specialized technical expertise and robust enterprise system management are vital for the industry’s continued success.

Strategic Implications for Leadership: Navigating the Data-Driven Future

The granular analysis of job postings across themes, geographies, and specific technical skills offers invaluable foresight for business leaders and investors. In an industry as dynamic and capital-intensive as semiconductors, where innovation cycles are rapid and competition is fierce, understanding where investment and capacity are genuinely shifting is crucial. By monitoring these hiring signals, which often precede shifts in financial performance by one to three months, stakeholders can make more informed decisions regarding resource allocation, market entry and exit strategies, and competitive positioning.

The ability to interpret these early indicators allows leaders to proactively identify burgeoning growth areas, potential market saturation, and emerging technological trends. This foresight can guide strategic investments in research and development, manufacturing capabilities, and talent development, ensuring that organizations remain agile and competitive in a rapidly evolving landscape.

GlobalData Jobs Analytics provides a critical tool for this strategic intelligence. By delivering point-in-time job postings directly from company career pages, meticulously tagged by company, sector, and theme, it offers an unfiltered view of actual hiring priorities. For leaders seeking to translate complex workforce data into actionable strategic insights, understanding these patterns is no longer a competitive advantage but a necessity for sustained success. Requesting a data sample or delving into comprehensive white papers can provide the clarity needed to navigate the intricacies of hiring trends and leverage them for robust planning and investment decisions in the future of the semiconductor industry.