For the better part of a decade, the strategic blueprint for real estate growth in Texas was characterized by its remarkable simplicity. To achieve scale, liquidity, and rapid capital appreciation, investors and developers focused their efforts almost exclusively on the "Texas Triangle"—the geographic region anchored by Austin, Dallas–Fort Worth, Houston, and San Antonio. The objective was to identify the next "ring of rooftops" on the periphery of these major metros and establish a presence before the inevitable surge of population and infrastructure followed.

During this era, these four metropolitan areas captured the overwhelming majority of the state’s population growth and job creation. National and international capital followed this demographic shift, pouring billions into high-rise residential towers in Austin, sprawling suburban developments in Collin County, and industrial hubs surrounding the Port of Houston. However, as the mid-2020s approach, that long-standing script is undergoing a fundamental revision.

While Texas continues to outpace much of the United States in terms of economic expansion, the breakneck speed of the post-pandemic era has transitioned into a more calculated, "normalized" phase. The Federal Reserve Bank of Dallas has noted that the state’s economy is currently moderating toward a more historically typical pace. This shift is characterized by easing job growth and a recalibration of consumer demand, even as overall conditions remain expansionary. For the real estate industry, this slowdown is not necessarily a harbinger of decline but rather a filter. As capital becomes increasingly selective, the focus is shifting away from the saturated urban cores toward secondary markets that offer a rare combination of absorption potential, pricing power, and regulatory efficiency.

The Macroeconomic Shift: From Boom to Normalization

The Texas economic miracle of the early 2020s was fueled by a unique confluence of factors: a massive influx of corporate relocations, a surge in remote work that prioritized space over proximity, and a relatively low cost of living compared to coastal hubs. However, the "everything works" mode of that period has been replaced by a market that requires deeper underwriting and more precise geographical targeting.

The Dallas Fed’s recent economic indicators suggest that while Texas remains a national leader, the gap between the state and the rest of the country is narrowing. Business investment and consumer spending remain resilient, yet the impact of sustained higher interest rates has cooled rate-sensitive sectors, particularly residential real estate and large-scale commercial construction.

Despite these headwinds, the macro picture for Texas remains fundamentally attractive. The state continues to benefit from a favorable tax environment and a diverse economic base that includes energy, technology, healthcare, and logistics. According to recent projections, Texas is expected to remain among the best-performing state economies through 2025. In the housing sector, statewide single-family permits are projected to grow by approximately 2.5% in 2025 compared to 2024 levels. This represents the second consecutive year of rising starts, signaling that the underlying demographic demand remains robust enough to overcome tighter affordability constraints.

The Psychology of the Modern Texas Buyer

The primary driver behind the rise of secondary markets is a shift in buyer psychology. After years of double-digit price appreciation in premium submarkets—such as Austin’s Zilker neighborhood or the Frisco-Plano corridor in North Texas—many prospective homeowners have reached an affordability ceiling.

Buyers are no longer willing or able to stretch their budgets for the same square footage in traditional "hot" ZIP codes. Instead, they are increasingly making a calculated trade-off: an additional fifteen to twenty minutes of commuting time in exchange for significant monthly savings and a different quality of life. This "attainability migration" is providing the momentum for secondary markets that were previously considered too far from the urban center to be viable for major development.

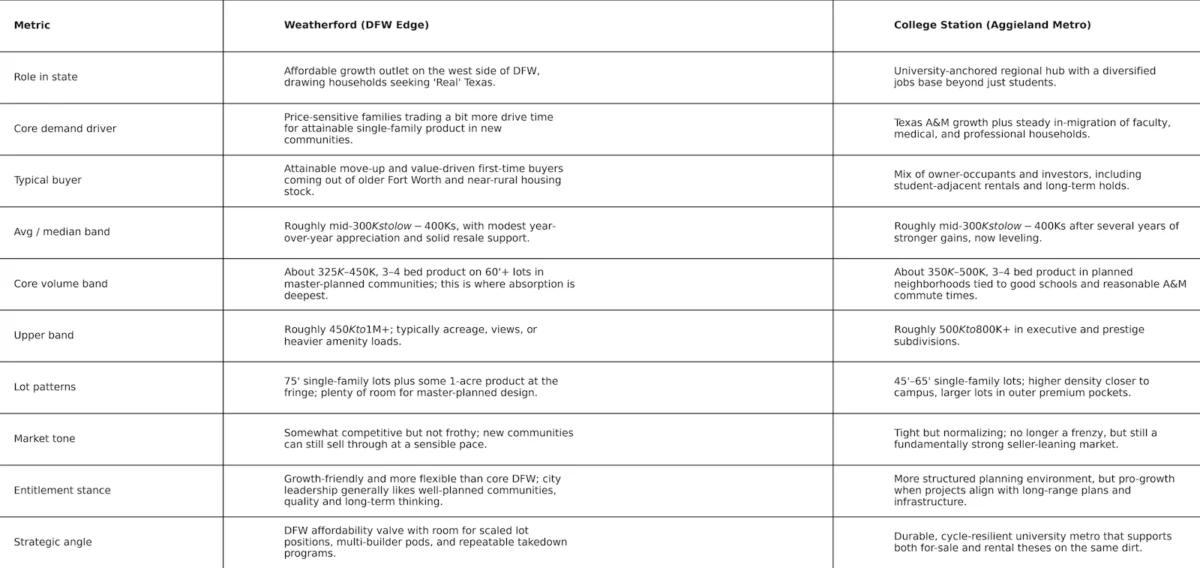

Weatherford: The New Frontier of the Dallas–Fort Worth Metroplex

Nowhere is the shift toward the periphery more evident than in Weatherford, a city located approximately 30 miles west of Fort Worth. Traditionally known as the "Cutting Horse Capital of the World" and celebrated for its historic courthouse square, Weatherford is rapidly transforming into one of the nation’s most significant affordable suburbs.

In a 2025 national analysis of the fastest-growing affordable suburbs, Weatherford was ranked 14th in the United States. It was one of only four suburbs in the DFW metroplex with a population under 50,000 to earn a spot on the list. The city’s appeal lies in its ability to offer genuine population growth while maintaining home values that remain accessible to households earning the area’s median income.

Current housing data indicates that Weatherford is transitioning from a quiet rural outpost to a high-demand suburban hub. The local demand is concentrated heavily in the $350,000 to $850,000 price range, a "sweet spot" that caters to two primary demographics: first-time buyers who have been priced out of central Fort Worth and "move-up" households looking for newer stock and larger lots.

For national homebuilders, Weatherford offers advantages that the core DFW markets have largely lost. These include:

- Entitlement Velocity: The regulatory environment in secondary markets often allows for faster project approvals compared to the bureaucratic hurdles found in larger municipalities.

- Land Availability: There is still a significant inventory of developable land that allows for production-scale communities.

- Infrastructure Connectivity: Direct access to Interstate 20 provides a straightforward commute to the major employment engines of the western Metroplex.

College Station: Stability through Institutional Anchors

While Weatherford represents the "edge-of-metro" growth story, College Station exemplifies the university-anchored secondary market. Together with its sister city, Bryan, College Station has outgrown its "college town" moniker to become a mid-sized metropolitan area with a diversified and stable economy.

The primary engine of this growth is Texas A&M University. The institution’s massive expansion—not just in student population, but in research expenditures and healthcare partnerships—has created a recession-resistant economic base. A 2025 market analysis revealed a significant surge in housing demand driven by this institutional stability.

In College Station, the market offers a dual-track opportunity for investors:

- Student and Faculty Housing: The constant influx of students and the hiring of high-income research staff create a perennial need for both high-density rentals and premium single-family homes.

- Professional Services and Healthcare: The growth of the RELLIS Campus and various bio-manufacturing initiatives has attracted a workforce that demands modern, amenity-rich master-planned communities.

Compared to the hyper-competitive markets of Austin or suburban Houston, College Station remains relatively affordable. However, it offers many of the same high-end amenities, including top-tier public schools and sophisticated retail developments, making it an attractive destination for families and retirees alike.

Underwriting Strategy in a Normalized Cycle

For institutional investors and builders accustomed to the "crane-counting" booms of the last decade, reallocating capital to secondary markets requires a more nuanced underwriting strategy. In a normalized growth environment, the metrics that dictate success have shifted.

First, regulatory efficiency has become a primary driver of ROI. In an environment of high financing costs, the time it takes to get a "shovel in the ground" can make or break a project’s viability. Secondary markets often offer a more collaborative relationship between developers and local government.

Second, demand depth is now prioritized over price appreciation. Investors are looking for markets where the median home price is aligned with the local median income, ensuring a deep pool of buyers even if the broader economy stutters.

Third, the "15-minute rule" has evolved. Buyers are willing to live further out, but they still demand proximity to "lifestyle infrastructure"—grocery stores, healthcare facilities, and quality schools. Secondary markets that have invested in their own internal infrastructure, rather than just acting as bedroom communities, are seeing the highest levels of absorption.

Chronology of the Texas Real Estate Evolution

To understand the current state of the market, it is essential to view it through the lens of the last five years:

- 2020–2021 (The Post-Pandemic Surge): Interest rates hit historic lows, and Texas becomes the top destination for domestic migration. The "Texas Triangle" sees unprecedented price growth, with Austin leading the nation.

- 2022 (The Rate Shock): The Federal Reserve begins a series of aggressive rate hikes to combat inflation. Transaction volume slows, but prices remain sticky due to a lack of inventory.

- 2023 (The Adjustment Phase): Builders begin using mortgage rate buy-downs to maintain sales velocity. Development starts to move further out into the "third ring" of suburbs as land costs in the core become prohibitive.

- 2024 (The Normalization): The Dallas Fed officially notes the cooling of the economy. Investors start pivoting from "growth at any cost" to "yield and stability," leading to increased interest in secondary markets like Weatherford and College Station.

- 2025 (The Secondary Pivot): Projections indicate that while the major metros will remain stable, the highest percentage of growth and the most attractive risk-adjusted returns will be found in secondary markets that offer affordability and high entitlement velocity.

Broader Impact and Implications

The shift toward secondary markets has significant implications for the future of Texas urban planning and economic policy. As development moves further from the urban cores, the state faces new challenges regarding transportation infrastructure and water management. The success of places like Weatherford and College Station will depend on their ability to manage this growth without losing the "small-town" appeal that initially attracted residents.

Furthermore, this trend suggests a "decentralization" of the Texas economy. Rather than being purely reliant on the four major hubs, the state is developing a network of resilient mid-sized cities that can support their own economic ecosystems. For the national homebuilding industry, this represents a permanent shift in strategy. The secondary market is no longer a "nice-to-have" addition to a portfolio; it has become a core component of the Texas growth strategy.

In summary, the Texas real estate market is not in decline, but it is maturing. The era of easy gains in the urban core has given way to a period where local knowledge, price point precision, and speed to market are the keys to success. For those willing to look beyond the skyline of Dallas or the tech hubs of Austin, the secondary markets of the Lone Star State offer a compelling new frontier for investment and development.