The infrastructure asset class, once a bastion of predictable income and stability, is now navigating a complex landscape shaped by its own remarkable growth. Once lauded for its resilience and steady returns, infrastructure has become a multifaceted investment arena, demanding a more nuanced approach from investors as it grapples with evolving definitions, shifting risk profiles, and the undeniable influence of political will. This evolution, while presenting new opportunities, also introduces complexities that necessitate a deeper understanding of the sector’s trajectory.

The Golden Decade: Infrastructure’s Meteoric Rise

The period following the 2008 Global Financial Crisis marked a pivotal moment for the infrastructure asset class. With governments worldwide struggling under the weight of increased debt and prioritizing financial sector bailouts, the funding gap for essential public works widened significantly. Projections from institutions like Stanford highlighted a staggering $2.6 trillion U.S. funding shortfall through 2029, while McKinsey estimated global annual infrastructure needs exceeding $9 trillion. This created a compelling vacuum, ripe for private investment.

From an investor’s perspective, infrastructure emerged as an attractive proposition. It offered tangible assets providing essential services, insulated from the vagaries of economic downturns. The promise of stable, often inflation-linked cash flows, underpinned by regulatory frameworks and long-term contracts, resonated deeply with those seeking alternatives to traditional fixed-income instruments. Furthermore, the inherent monopolistic nature of many infrastructure assets provided significant pricing power, a highly desirable trait in a post-crisis environment. This unique combination – the perceived safety of bonds with the potential income of equities – fueled an unprecedented surge in capital allocation.

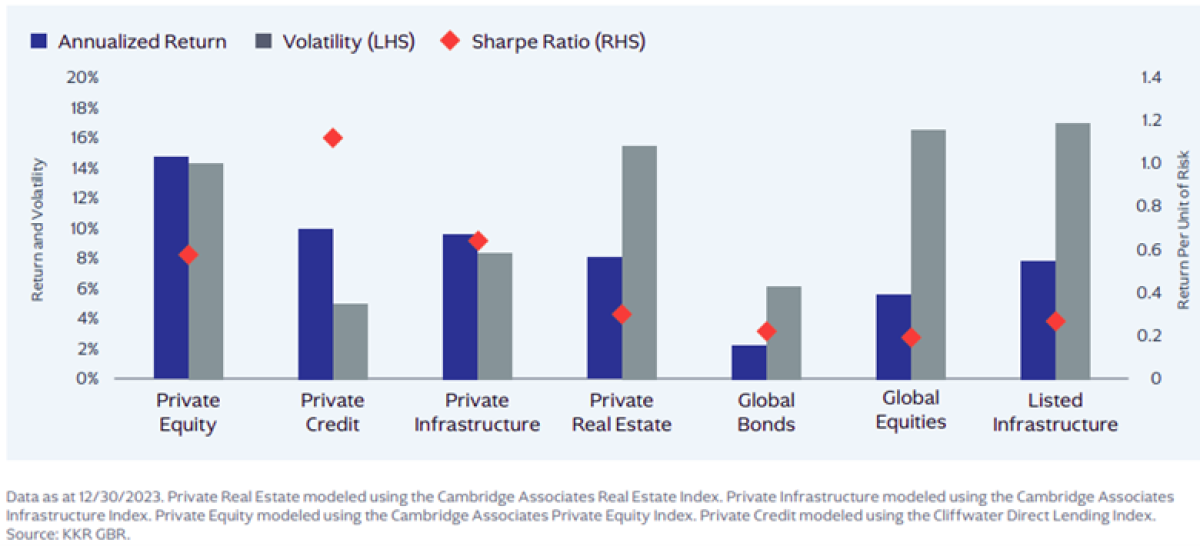

By 2013, private infrastructure funds managed an estimated $60 billion. This figure ballooned dramatically, with projections indicating it would reach $1.6 trillion by 2026. This represented a compound annual growth rate in the double digits, second only to venture capital among private asset classes. This era, particularly from 2016 to 2022, saw global infrastructure funds consistently deliver average annual returns of approximately 11%. Crucially, the mark-to-market volatility observed during this period was often comparable to that of public bonds, and correlations with public equity markets remained within a manageable range of 0.6-0.8, as illustrated in Figure 1.

Figure 1: Asset Class Performance

(Image of a graph showing infrastructure asset class performance relative to other asset classes, with a description indicating it demonstrates lower volatility and stable returns during the 2016-2022 period.)

Source: KKR. It is important to note that mark-to-market volatility in private markets does not always provide a direct apples-to-apples comparison with public markets.

The Paradox of Success: "Suffering from Success"

However, this sustained period of growth and attractive returns began to present its own set of challenges, echoing the sentiment of DJ Khaled’s 2013 album, "Suffering from Success." By the early 2020s, the very popularity of infrastructure started to inflate valuations and intensify competition for assets. In 2021 alone, infrastructure funds raised a record $130 billion. This influx of capital created a seller’s market, driving up prices for mature, low-risk assets such as utilities and toll roads – the very cornerstones of infrastructure investing that had historically delivered 8-10% internal rates of return (IRRs).

This intense competition for established assets led to a situation where projected returns for these traditional infrastructure investments began to decline, while the operational complexities remained. General Partners (GPs) found themselves under pressure to deploy vast sums of capital, often necessitating a re-evaluation of what constituted an "infrastructure" investment. The once clear-cut definition began to blur as the easy, low-risk, high-yield deals became scarce. Investors were faced with a stark choice: accept lower returns on mature assets or venture further up the risk curve into territory that increasingly resembled private equity.

The Expanding Definition: A New Era of Infrastructure

The term "infrastructure" itself has undergone a significant transformation over the past 15 years. Historically, it conjured images of tangible, long-lived physical assets like toll roads, airports, utilities, and schools. These were characterized by stable demand, predictable cash flows secured through regulated or concession-based frameworks, and an inherent essentiality. While perhaps not glamorous, these assets provided a reliable foundation for investor portfolios.

Today, the definition has broadened considerably, and it is within this expanded scope that much of the new capital is being deployed.

Digital Infrastructure: The New Essential Utility

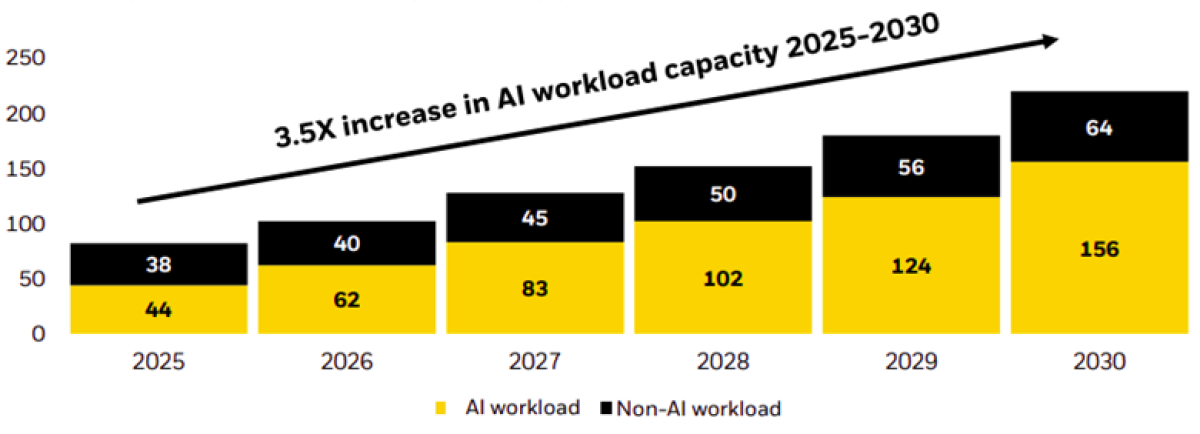

Digital infrastructure has emerged as perhaps the most striking example of this redefinition. Telecom towers, fiber optic networks, and data centers, once considered niche technology-driven projects, are now increasingly viewed as the digital equivalent of traditional utilities. The exponential growth in data consumption, fueled by the rise of cloud computing and the accelerating adoption of artificial intelligence (AI), has cemented digital connectivity as a critical component of modern economies, as essential as water or power.

These assets often benefit from long-term contracts with highly creditworthy counterparties, leading to predictable and often growing cash flows. Telecom towers and fiber networks, for instance, have transitioned from "core-plus" to "core" or even "super-core" status due to their predictable revenue streams. McKinsey projects that global data center capacity could nearly quadruple by 2030, underscoring the immense growth potential in this sector.

Figure 2: Estimated Global Data Center Capacity Demand, Gigawatts

(Image of a bar chart projecting a significant increase in global data center capacity demand over the next decade.)

Source: McKinsey, retrieved from BlackRock.

The economic implications of this digital expansion are profound. Just as the development of the U.S. interstate highway system between 1950 and 1989 is credited with contributing approximately 25% of American productivity gains during that period, the widespread availability and expansion of digital infrastructure could yield similar macro-economic benefits.

Renewable Energy & Clean Power: A Climate Imperative

The imperative to address climate change has propelled renewable energy and clean power into the forefront of infrastructure investment. A decade ago, this sector was nascent, heavily reliant on subsidies, and often viewed as akin to venture capital. Today, it represents a crucial pillar in the effort to "climate-proof" economies.

Clean energy has, in many regions, shifted from a subsidy-dependent model to one that is increasingly market-competitive. The sheer scale of investment required for the global energy transition – estimated at approximately $9 trillion annually through 2050 – has spurred the creation of dedicated energy transition funds. This has led to increased capital allocation towards higher-risk greenfield projects, including offshore wind farms, energy storage solutions, and grid modernization initiatives, areas where governments alone are unable or unwilling to shoulder the full financial burden.

Conventional Energy & Utilities: Navigating the Transition Risk

The landscape for conventional energy and utilities presents a more complex narrative. Natural gas pipelines and fossil-fuel power plants, historically considered stable, low-risk cash cows, now face significant "transition risk" as economies pivot towards cleaner energy sources. A traditional gas distribution network, once a "super-core" asset, might require substantial and costly repurposing to accommodate hydrogen or other alternative fuels, thereby elevating its risk profile. These assets necessitate a strategic re-evaluation, focusing on which specific components remain viable and adjusting return expectations accordingly.

Transportation & Logistics: The Enduring Backbone

Transportation and logistics, encompassing toll roads, airports, and seaports, remain fundamental components of infrastructure portfolios. However, the need for extensive maintenance and repair across these networks is substantial. Data from BlackRock indicates that U.S. bridges require nearly $375 billion in repairs over the next decade. Similarly, approximately half of Japan’s roads and tunnels are nearing 50 years of age, and nearly 20% of England’s water supply is lost due to leaks. These figures highlight significant opportunities for brownfield upgrades and reinvestment, essential for maintaining the functional integrity of the global economy’s traditional backbone.

The modern definition of infrastructure now spans a wide spectrum, from the ultra-stable, regulated utilities to the frontier of greenfield renewable projects and the innovation-driving realm of digital connectivity. This broad scope demands that investors approach infrastructure with the same sector and risk differentiation they apply to equity markets, looking beyond the overarching label to understand the unique characteristics of each sub-sector.

The Political Will Variable: A Growing Determinant

In assessing infrastructure’s role within a diversified portfolio, two distinct, yet often intertwined, opportunities emerge: the fundamental, often unglamorous, work of maintaining and upgrading physical infrastructure, and the high-growth potential offered by digital infrastructure. Modern infrastructure portfolios must encompass both.

However, the performance dispersion within the infrastructure asset class has widened considerably. Cambridge Associates data reveals that while diversified infrastructure strategies may yield median returns below 10%, digital infrastructure strategies can achieve returns around 14%. More critically, the distribution of returns within these strategies offers insights into geopolitical risk. Digital infrastructure, like venture capital, often exhibits extreme positive skew in its return distribution, indicating the potential for substantial upside. Conversely, renewables and power projects may display left-skewed distributions, suggesting a higher probability of downside risk.

Figure 3: Infrastructure Returns by Strategy Type, Vintages 2009 – 2020

(Image of a chart comparing the return distributions of different infrastructure strategy types, highlighting the skewness of returns.)

Source: Cambridge Associates.

The true complexity arises when overlaying the impact of political will. Extreme left-skewed return distributions can often be attributed to government intervention, which may manifest as regulatory delays, policy shifts, or protracted political infighting, particularly impacting legacy businesses. This is most evident in traditional utilities and energy assets operating within politically fractious environments. Conversely, a clear and supportive infrastructure agenda, such as that demonstrated by Germany, can act as a significant enabler of growth. In contrast, fragmented decision-making processes, as seen in the United States, can become a constraint on development and investment.

Therefore, infrastructure has evolved beyond its initial role as a mere fixed-income replacement or a stable income generator. It now encompasses growth allocations and, increasingly, represents a strategic bet on the capacity and ambition of governments. The political environment is no longer a peripheral consideration; it is emerging as a primary driver of which infrastructure assets will deliver value and which may disappoint.

Synthesizing the Landscape: Investing in the Future

In the nascent stages of private infrastructure investing, the asset class was envisioned as a dual solution: bridging the government funding gap and satisfying investor demand for income and stability. This vision necessitated a dramatic expansion of the asset class’s definition, now encompassing both the predictable stability that investors initially sought and the inherent complexity and risk associated with private equity. Compounding this is the current geopolitical landscape, characterized by intense competition and transformational change. Consequently, investing in infrastructure today transcends merely acquiring assets; it involves making a calculated bet on the efficacy and foresight of governmental leadership.

While infrastructure has, at times, "suffered from success," investors must recognize that the current market dynamics demand a sophisticated understanding of its diversified nature. The days of a monolithic infrastructure investment are over. Navigating this evolving terrain requires a granular approach, discerning the distinct risk and return profiles within the broad asset class and acknowledging the pervasive influence of political will on future performance.