The global transition toward a low-carbon economy has entered a volatile new phase characterized by a retreat from open markets and the rise of strategic protectionism. As nations scramble to secure their positions in the burgeoning green industrial revolution, the era of unfettered free trade in clean technology is being replaced by a complex landscape of defensive trade postures, localized manufacturing mandates, and escalating tariff regimes. Governments worldwide are increasingly viewing solar panels, lithium-ion batteries, and electric vehicles (EVs) not merely as tools for climate mitigation, but as the fundamental pillars of 21st-century economic sovereignty and national security. This shift toward "walled markets" represents a significant departure from the previous decade’s emphasis on globalized supply chains, threatening to alter the pace and cost of the international energy transition.

The Rapid Proliferation of Trade Barriers

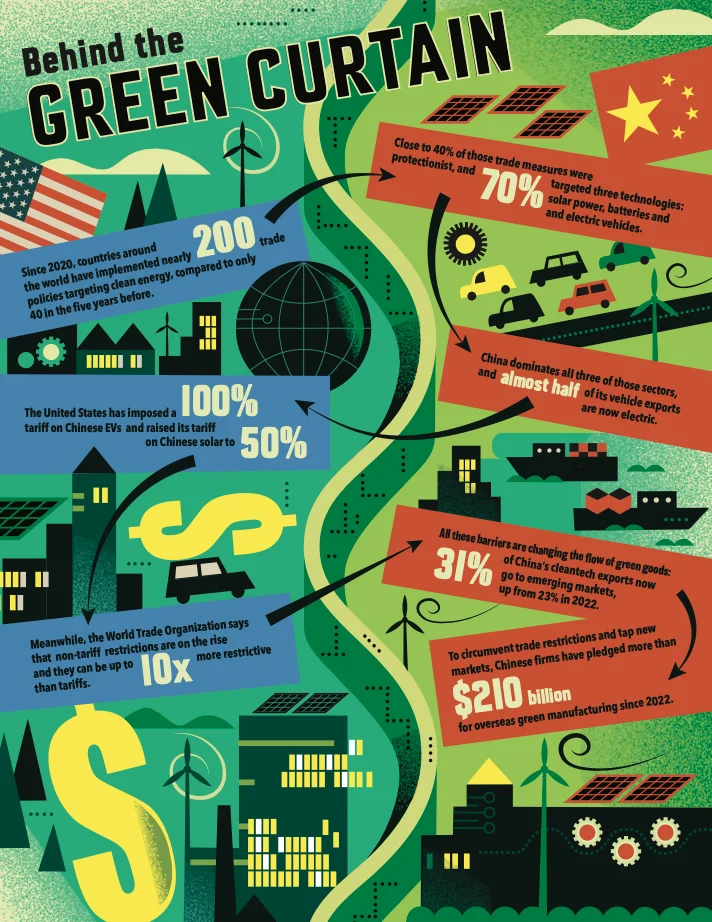

The acceleration of trade interventions in the green sector is a relatively recent phenomenon, primarily catalyzed by the disruptions of the early 2020s. According to data from the Net Zero Policy Lab and the International Energy Agency (IEA), the global community has implemented nearly 200 trade policies specifically targeting clean energy since 2020. To put this into perspective, only 40 such measures were enacted in the preceding five-year period between 2015 and 2019. This fivefold increase signals a profound change in how policymakers approach the intersection of climate goals and industrial strategy.

Of these approximately 200 measures, roughly 40% are classified as overtly protectionist, designed to shield domestic industries from foreign competition or to incentivize the "onshoring" of production. The focus of these policies is highly concentrated; approximately 70% of the trade measures target three critical "New Three" technologies: solar photovoltaic (PV) modules, advanced batteries, and electric vehicles. These sectors are the primary battlegrounds because they represent the largest market opportunities and the most critical components of a decarbonized infrastructure.

A Chronology of the Shift Toward Defensive Industrialism

The movement toward green protectionism did not occur in a vacuum but followed a series of global shocks and strategic realizations.

2015–2019: The Era of Cost Reduction through Globalization. Following the Paris Agreement, the global focus was primarily on driving down the cost of renewables. China’s massive scaling of solar production helped reduce costs by over 80%, but it also led to the hollowing out of solar manufacturing in Europe and North America. Trade tensions existed but were often secondary to the goal of rapid deployment.

2020–2021: The Pandemic and Supply Chain Fragility. The COVID-19 pandemic exposed the vulnerabilities of "just-in-time" global supply chains. As countries struggled to source essential components, the concept of "strategic autonomy" gained traction. Governments began to realize that relying on a single dominant supplier—China—for the components of the energy transition posed a significant geopolitical risk.

2022: The Legislative Pivot. This year marked a turning point with the passage of the Inflation Reduction Act (IRA) in the United States. By decoupling subsidies from domestic content requirements, the U.S. effectively signaled that the future of the green economy would be built at home. Simultaneously, the European Union began formalizing its Green Deal Industrial Plan to prevent an exodus of capital to the U.S. or China.

2023–2025: The Escalation of Tariffs. Tensions reached a boiling point as Western markets became concerned about Chinese "overcapacity." As China’s domestic demand for EVs and solar panels cooled relative to its massive production capacity, it began exporting surplus goods at prices that Western manufacturers claimed were artificially low due to state subsidies. This led to the landmark tariff increases seen in mid-2024 and 2025.

The Dominance of China and the Western Response

The primary driver of current protectionist sentiment is the overwhelming market dominance of the People’s Republic of China. China currently controls more than 80% of the global solar manufacturing chain and a similar share of the processing for critical minerals used in batteries. The scale of China’s export machine is most evident in the automotive sector, where almost half of its vehicle exports are now electric.

In response to this dominance, the United States has taken the most aggressive stance. The U.S. government recently imposed a 100% tariff on Chinese-made electric vehicles, effectively barring them from the American market. Furthermore, tariffs on Chinese solar cells and modules were raised to 50%, a move intended to provide a breathing room for the domestic manufacturing base fostered by the IRA.

The European Union has followed a more moderated but still defensive path. Following an anti-subsidy investigation into Chinese EVs, the EU implemented provisional countervailing duties, arguing that Chinese manufacturers benefit from unfair state support. While European leaders remain wary of a full-blown trade war—given their dependence on China for critical minerals—the shift toward protecting the European automotive industry is unmistakable.

The Rise of Non-Tariff Barriers and Their Economic Weight

While headlines often focus on high-percentage tariffs, the World Trade Organization (WTO) has warned that non-tariff restrictions are becoming an even more significant hurdle to clean tech trade. These measures include local content requirements, stringent technical standards, complex certification processes, and "green" procurement rules that favor local suppliers.

Data suggests that these non-tariff barriers can be up to 10 times more restrictive than traditional tariffs. For example, a country might not impose a direct tax on an imported battery but may require it to meet specific environmental or labor standards that are difficult for foreign firms to verify quickly. These "invisible" barriers create a fragmented regulatory landscape, making it difficult for companies to achieve the economies of scale necessary to lower prices for consumers.

The Redirection of Trade Flows to Emerging Markets

As the U.S. and EU markets become increasingly difficult to penetrate, the flow of green goods is undergoing a major geographic realignment. China, in particular, has redirected its export focus toward the Global South and emerging economies. Currently, 31% of China’s cleantech exports are destined for emerging markets, a significant increase from the 23% recorded in 2022.

Nations in Southeast Asia, Latin America, and the Middle East are benefiting from this shift, gaining access to low-cost solar panels and EVs that are being diverted away from Western "walled markets." However, this trend also creates a dilemma for these emerging economies: while they benefit from cheap technology to meet their own climate goals, they also face pressure to protect their own nascent manufacturing sectors from being overwhelmed by Chinese imports.

Strategic Circumvention: The $210 Billion Overseas Investment

In an effort to bypass trade restrictions and maintain access to global markets, Chinese firms have adopted a strategy of "localization" outside of China. Since 2022, Chinese companies have pledged more than US$210 billion for overseas green manufacturing projects. By building factories in countries that have favorable trade agreements with the U.S. or EU—such as Mexico, Hungary, Morocco, and Thailand—Chinese firms can effectively "neutralize" the impact of tariffs.

For instance, Chinese battery giants like CATL and Gotion have announced multi-billion dollar investments in Hungary to serve the European automotive market from within the EU’s borders. Similarly, Chinese EV makers are scouting locations in Mexico to potentially access the North American market under the terms of the USMCA (United States-Mexico-Canada Agreement). This "offshoring" of Chinese capital and technology is creating a new global manufacturing map, where the origin of the company matters less than the physical location of the factory.

Implications for the Global Energy Transition

The rise of green protectionism carries profound implications for the global fight against climate change. On one hand, the race to build domestic industries is driving a massive surge in capital investment. The IEA notes that global investment in clean energy is now significantly higher than investment in fossil fuels. The competition to be a "green superpower" is encouraging governments to provide subsidies and support that might not have existed in a purely free-market environment.

On the other hand, protectionism threatens to increase the cost of the transition. By restricting the flow of the world’s lowest-cost clean technologies, countries may find that the price of installing solar farms or transitioning to electric fleets becomes significantly higher. Economists warn that if every country tries to build its own end-to-end supply chain, the resulting inefficiencies could delay net-zero targets by years.

Furthermore, the fragmentation of the market could lead to a "technology schism," where different regions operate on different standards and supply chains, reducing the global compatibility of green infrastructure.

Official Responses and the Future of Trade Governance

The WTO and the OECD have expressed growing concern over the trend. WTO Director-General Ngozi Okonjo-Iweala has repeatedly called for "re-globalization" rather than fragmentation, arguing that the world needs more trade, not less, to solve the climate crisis. International bodies are currently struggling to update trade rules that were designed for a different era—one where environmental subsidies were seen as market distortions rather than essential policy tools.

As the decade progresses, the challenge for policymakers will be to strike a balance between legitimate national security concerns and the urgent need for a rapid, low-cost global energy transition. The current trend toward walled markets suggests that the "green gold rush" will be a period of intense rivalry, where the flow of technology is governed as much by geopolitical strategy as by market demand. The outcome of this shift will determine not only which nations lead the next industrial age but also how effectively the world can meet its collective environmental obligations.