In the wake of the Global Financial Crisis of 2008, a seismic shift occurred in the world of asset allocation. Governments, burdened by mounting debts and the immediate imperative of financial sector stabilization, significantly curtailed their infrastructure spending. This fiscal vacuum, however, coincided with a growing consensus among researchers and economists: a critical need for infrastructure development and upgrades across the globe, coupled with an inability of public funds to meet this demand. Projections from institutions like Stanford, which estimated a $2.6 trillion U.S. funding shortfall through 2029, and McKinsey, which put global annual infrastructure needs at over $9 trillion, underscored the urgency. This confluence of factors created a fertile ground for private investment to step into the breach, fundamentally reshaping the infrastructure asset class.

The appeal for investors was multifaceted. Infrastructure assets, by their nature, represent tangible, essential services—power grids, transportation networks, utilities—that remain in demand irrespective of economic cycles. This inherent resilience translated into stable, predictable cash flows, often bolstered by regulatory frameworks or long-term contracts, and frequently indexed to inflation. Furthermore, many infrastructure assets historically benefited from monopolistic or oligopolistic market positions, granting them significant pricing power. For investors emerging from the wreckage of 2008, this offered a compelling proposition: an asset class that could, in theory, deliver bond-like stability with equity-like returns.

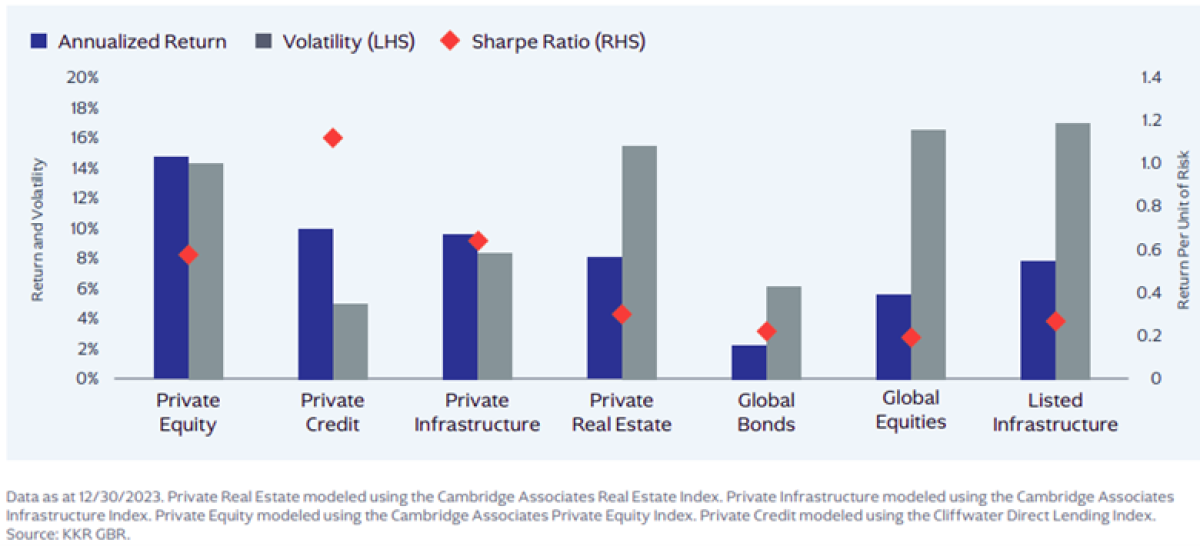

This narrative proved remarkably successful throughout the 2010s. The total assets under management in private infrastructure funds surged from approximately $60 billion in 2008 to an astonishing $1.6 trillion by 2026, representing a compound annual growth rate that trailed only venture capital among private asset classes. From 2016 to 2022, global infrastructure funds consistently delivered average annual returns of around 11%, with volatility that closely mirrored that of public bonds. Correlations with public markets during this period ranged between 0.6 and 0.8, further cementing infrastructure’s reputation as a reliable diversifier and income generator. This era was characterized by investments in mature, well-understood assets such as toll roads, utilities, and airports, which offered predictable yields and relatively straightforward operational management.

The Unintended Consequences of Success

However, as DJ Khaled famously quipped in his 2013 album "Suffering from Success," even immense prosperity can bring its own set of challenges. By the early 2020s, the infrastructure asset class began to exhibit the strains of its own burgeoning popularity. In 2021 alone, infrastructure funds raised a record $130 billion, leading to a highly competitive environment where General Partners (GPs) were under immense pressure to deploy capital. This capital inflow inevitably drove up asset valuations. The "boring" yet reliable infrastructure assets that had formed the bedrock of the asset class’s success—mature utilities and toll roads, typically yielding 8-10% internal rates of return (IRRs)—began to project lower returns, while their operational complexities remained.

This inflection point signaled the end of an era characterized by easy, low-risk, high-yield deals. The market became bifurcated: investors were left with either expensive, mature assets with diminishing return prospects or riskier, more complex projects that demanded greater expertise and tolerance for uncertainty. The choice for investors became stark: accept lower returns on established assets or venture further up the risk curve, into territory that increasingly resembled private equity.

An Expanding Definition: Beyond Roads and Rails

Historically, infrastructure was defined by its tangible, long-lived physical assets, stable demand, and predictable cash flows, often secured through regulated or concession-based frameworks. This included everything from toll roads and airports to utilities and schools. While perhaps not glamorous, these assets provided a crucial bedrock for economic activity and investor portfolios.

Over the past 15 years, however, the definition of infrastructure has undergone a dramatic expansion, and it is within this broadened scope that the majority of new capital has been deployed.

Digital Infrastructure: The New Essential Utility

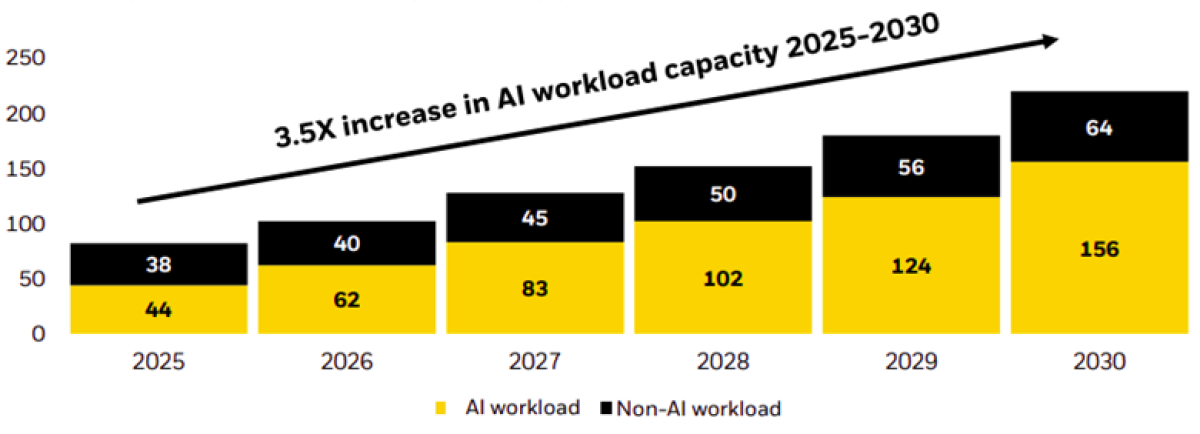

Perhaps the most striking evolution has been the emergence of digital infrastructure. Telecom towers, fiber optic networks, data centers, and 5G infrastructure, once considered niche, technology-driven projects, are now increasingly viewed as the new utilities of the 21st century. The exponential growth in data consumption, fueled by the rise of cloud computing and the burgeoning adoption of artificial intelligence (AI), has rendered digital connectivity as critical as water or power. Demand for these services is highly inelastic, and many digital infrastructure assets now feature long-term contracts with improving risk profiles. Telecom towers and fiber networks, for instance, have transitioned from "core-plus" to "core" or even "super-core" status due to the predictability of their cash flows. Projections from McKinsey indicate that global data center capacity could nearly quadruple by 2030, highlighting the immense scale of this sector’s growth. This trend may have profound macro-economic implications, akin to the productivity gains spurred by the U.S. interstate highway system in the mid-20th century.

Renewable Energy and Clean Power: A Climate Imperative

Renewable energy and clean power infrastructure have also become central to modern infrastructure allocations. A decade ago, this sector was nascent, heavily reliant on subsidies, and bore a strong resemblance to venture capital investments. Today, it is a critical pillar in the global effort to "climate-proof" economies. Clean energy sources have, in many regions, achieved market competitiveness, transitioning away from subsidy dependence. The sheer scale of the energy transition—estimated to require approximately $9 trillion annually in physical assets through 2050—has spurred the creation of dedicated energy transition funds. This imperative has also driven increased capital allocation towards higher-risk greenfield projects, including offshore wind farms, energy storage solutions, and grid modernization initiatives, areas where governments alone are unable or unwilling to bear the full financial burden.

Conventional Energy and Utilities: Navigating the Transition

The landscape for conventional energy and utilities presents a more nuanced picture. Natural gas pipelines and fossil-fuel power plants, once considered low-risk, stable cash cows, now face significant transition risk as economies pivot towards cleaner energy sources. A gas distribution network, traditionally a "super-core" asset, might require costly repurposing for hydrogen or other alternative fuels, thus elevating its risk profile. These assets necessitate a strategic "facelift," involving a careful reassessment of which specific components remain viable and what risk-return expectations are realistic in a decarbonizing world.

Transportation and Logistics: The Enduring Backbone

Transportation and logistics infrastructure, encompassing toll roads, airports, and seaports, continues to be a core component of infrastructure portfolios. However, significant maintenance and repair backlogs persist. Data from BlackRock highlights the magnitude of these needs: U.S. bridges require nearly $375 billion in repairs over the next decade, approximately half of Japan’s road and tunnel infrastructure will soon exceed 50 years of age, and nearly 20% of England’s water supply is lost to leaks. These challenges represent substantial opportunities for brownfield upgrades and reinvestment, essential for maintaining the foundational elements of our economies.

The modern iteration of infrastructure is thus a far broader category than its historical predecessor, encompassing assets ranging from ultra-stable, regulated utilities to greenfield renewable projects and innovation-supporting digital networks. This evolution necessitates a more sophisticated approach from investors, compelling them to analyze infrastructure through a lens similar to equity markets, with a keen focus on sector-specific dynamics and risk differentiation, rather than treating it as a monolithic asset class.

The Political Will Variable: A Growing Determinant of Success

In evaluating infrastructure’s role within a diversified portfolio, two parallel investment opportunities emerge: the essential, albeit less glamorous, work of maintaining and upgrading the physical backbone of economies, and the high-growth potential inherent in digital infrastructure, which is rapidly becoming as critical as traditional physical networks. Consequently, contemporary infrastructure portfolios must strategically encompass both.

A notable consequence of this diversification is a widening dispersion in infrastructure asset performance. Data from Cambridge Associates indicates that while diversified infrastructure strategies may yield median returns below 10%, digital infrastructure investments can achieve returns around 14%. More crucially, the distribution of returns offers insights into geopolitical risk. Digital infrastructure, much like venture capital, exhibits extreme positive skew in its return distribution, signifying the potential for substantial upside. Conversely, renewables and power infrastructure often display left-skewed distributions, suggesting a higher likelihood of downside risk or a more constrained upside potential.

The interplay of these dispersion figures with political will is a critical, and often underestimated, factor. Extreme left-skewed return distributions can arise when governmental intervention, whether through overly stringent regulations, policy indecision, or inter-party conflict, significantly impedes project development or operational efficiency, particularly for legacy assets. This dynamic is most evident in traditional utilities and energy sectors operating within politically fractious environments. Conversely, a clear and consistent infrastructure agenda, as exemplified by Germany’s national strategy, can act as a powerful enabler, while fragmented decision-making processes, such as those often seen in the United States, can present significant constraints.

Therefore, infrastructure has necessarily evolved beyond its original remit. It now functions as a partial substitute for fixed-income investments, a component of growth allocation, and increasingly, a bet on the efficacy and ambition of governmental policies. The political environment is no longer a mere footnote to infrastructure investing; it is poised to become a primary determinant of which assets deliver superior returns and which disappoint.

Synthesizing the New Infrastructure Paradigm

In its nascent stages, private infrastructure was envisioned as a dual solution: addressing the public funding gap for essential projects while providing investors with stable income and capital preservation. However, the relentless pursuit of scale and return has led to a dramatic expansion of the asset class. Today, it encompasses both the stable, income-generating assets that investors initially sought and the complexity and risk profiles previously associated with private equity. This evolution, compounded by the dynamics of geopolitical competition and transformative technological change, means that investing in infrastructure is no longer solely about acquiring physical assets. It has become, in essence, a strategic wager on the capacity of governments to effectively manage and foster development within their jurisdictions.

The repeated cycles of infrastructure "suffering from success" underscore the need for a nuanced and dynamic approach to portfolio construction. Investors must recognize that the traditional definition no longer suffices and that a deep understanding of sector-specific risks, technological trends, and, critically, the prevailing political landscape is paramount to navigating this evolving asset class successfully. The future of infrastructure investment lies not just in identifying viable projects, but in discerning which governmental frameworks are most conducive to their long-term success.

The Path Forward: Embracing Complexity and Differentiation

As the infrastructure landscape continues to mature and diversify, investors face a more complex decision-making environment. The era of straightforward, predictable returns from traditional infrastructure assets is giving way to a more nuanced reality. The burgeoning digital infrastructure sector offers significant growth potential but also introduces new technological and regulatory risks. Renewable energy projects, while crucial for the energy transition, are subject to evolving policy landscapes and can be capital-intensive with long development cycles. Conventional energy assets face the headwinds of decarbonization mandates.

Therefore, a "one-size-fits-all" approach to infrastructure investing is no longer tenable. Investors must develop sophisticated due diligence processes that can differentiate between various sub-sectors, assess project-specific risks, and evaluate the impact of governmental policies and geopolitical stability. This may involve increased reliance on specialized managers with deep sector expertise and a robust understanding of regulatory frameworks.

Furthermore, the increased correlation of some infrastructure assets with public markets during periods of stress, as seen in recent times, necessitates a re-evaluation of their diversification benefits. While infrastructure can still play a vital role in portfolio construction, its performance drivers are becoming more varied and, in some cases, more intertwined with broader market and political trends.

Ultimately, the successful navigation of the modern infrastructure landscape requires a forward-looking perspective, a commitment to ongoing research, and a willingness to embrace the inherent complexities and political variables that now shape this critical asset class. The opportunities for both essential infrastructure renewal and high-growth digital expansion remain substantial, but realizing them demands a more discerning and strategic investment approach than ever before.