The Department of Justice’s (DOJ) emphasis on "voluntary and timely" self-disclosure as a critical factor in leniency for corporate misconduct, while seemingly straightforward, presents a complex and often opaque challenge for compliance professionals. An in-depth analysis of recent enforcement actions reveals that the practical application of this principle, particularly the definition of "timely," remains a significant area of ambiguity, potentially leaving companies uncertain about when and how to secure crucial credit that can significantly mitigate penalties.

Recent examinations of enforcement cases where companies received credit for timely disclosure have highlighted a stark lack of specificity regarding measurable timeframes. Of the nine cases scrutinized, only two offered concrete benchmarks for what constituted prompt reporting. This scarcity of defined parameters raises questions about the consistency and predictability of the DOJ’s approach, potentially transforming a promised "guaranteed" benefit into a more precarious gamble for businesses operating under increasing regulatory scrutiny.

The financial stakes associated with timely disclosure are substantial. Companies that failed to meet the perceived timeliness window in the analyzed cases faced criminal penalties and disgorgement averaging between $140 million and $170 million. This underscores the critical importance of understanding and adhering to the government’s expectations, even when those expectations are not explicitly defined.

The core of the issue lies in the government’s rather abstract definition of "timely." While corporate leaders might naturally desire clear directives, such as "within hours" or "within weeks," the reality, as evidenced by enforcement patterns, is far more nuanced. The DOJ’s guidance, while encouraging self-reporting, often falls short of providing the granular detail necessary for companies to confidently navigate these high-stakes decisions. This creates a scenario where a company’s perception of timeliness may not align with the government’s unarticulated standard, leading to missed opportunities for leniency.

Navigating this ambiguity requires a delicate balancing act. Companies are expected to identify potential legal breaches, conduct thorough internal investigations, implement necessary remediation, and report these findings to the government. Crucially, this process must often commence and conclude, or at least show significant progress, well before the internal investigation is fully finalized and all loose ends are tied. This inherent tension was acknowledged by Taryn McDonald, a partner at Haynes Boone, who stated in an interview with Corporate Compliance Insights (CCI), "The DOJ wants you to disclose all relevant facts, but they also want you to disclose very, very early. That’s really hard to do. If you make a decision to disclose, you’re not waiting till it’s all tied up with a bow. It’s just not going to be possible."

The Ambiguity of "Timely": A Lack of Defined Benchmarks

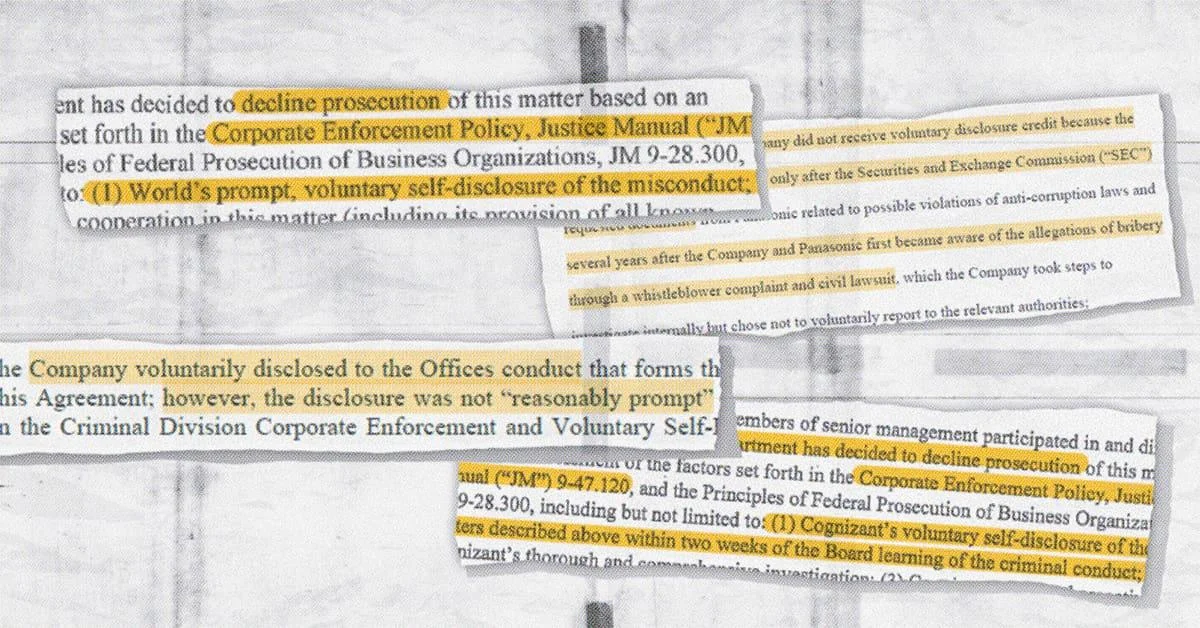

The enforcement record, much like the DOJ’s public guidance, offers limited specific details, even in instances where companies were recognized for their prompt reporting. In the nine examined cases where credit was granted for timely disclosure, only two provided any quantifiable time window. In one notable instance, a company reported potential misconduct within three months of its initial identification and within hours of internal confirmation. Another case saw the board of directors notify the government of an issue within two weeks of becoming aware of it.

However, the majority of credited disclosures were described using general terms such as "voluntarily and timely," "promptly," or "prompt, voluntary self-disclosure." These broad descriptors offer little in the way of a clear benchmark for compliance officers striving to establish definitive internal processes. In one particularly illustrative case, a company disclosed its findings while its internal investigation was still ongoing, a fact that was positively acknowledged by the declination letter without elaborating on what a delayed disclosure might have entailed.

A critical omission in these credited letters is the absence of a clearly defined starting point for the "timeliness clock." The government has not specified whether this clock begins ticking upon the initial allegation, the conclusion of a preliminary inquiry, or the moment of internal confirmation. Furthermore, there is no indication of what level of delay, if any, would disqualify a company from receiving credit. The message conveyed to companies that successfully navigated this process is essentially: "You were timely." For others, the implicit message is a cautionary one, highlighting the potential pitfalls of delayed action.

Conversely, when companies missed the self-disclosure window, or failed to open it at all, the language in enforcement documents tends to be more precise. A deferred prosecution agreement (DPA) with a major corporation explicitly stated that the company "did not voluntarily and timely disclose" the conduct in question. Another agreement detailed that a company "did not receive voluntary disclosure credit" because its disclosures were made "only after the [Securities and Exchange Commission (SEC)] requested documents" and occurred years after the company had been alerted to bribery allegations through a whistleblower complaint and a civil lawsuit. Despite conducting internal investigations into these allegations, the company had opted not to report them.

When External Triggers Preempt Corporate Action

In several documented cases, the enforcement record clearly indicates that the opportunity for timely disclosure was effectively closed not by the company’s inaction, but by external parties or events. This pattern, where the timeliness clock effectively runs out before a company takes action, is a recurring theme.

For instance, in a case involving a global spirits company, a former employee preemptively alerted both American and Indian government authorities via email regarding alleged misconduct before the company had come forward. Consequently, the company was denied voluntary disclosure credit and incurred a penalty of $19.6 million.

A similar scenario unfolded in a 2024 deferred prosecution agreement with SAP SE, the German software giant. The DPA explicitly stated that the company "did not voluntarily and timely disclose" the conduct at issue, as South African investigative reports had already publicized the allegations. While SAP initiated cooperation immediately following the press reports and received substantial cooperation credit, the voluntary self-disclosure credit was unattainable. The company ultimately paid $119 million in criminal penalties and an additional $103 million in disgorgement. In both these instances, the determination of timeliness was effectively made by external actors, leaving the companies with no agency in the matter.

Deliberate Choices and Their Consequences

Other cases, such as those involving Panasonic Avionics and Albemarle, offer a different perspective, illustrating situations where companies possessed the necessary information, had conducted internal investigations, and were faced with a clear decision regarding disclosure. The outcomes in these instances provide valuable insights into the potential ramifications of such choices.

Panasonic Avionics learned of bribery allegations through a whistleblower complaint and a subsequent civil lawsuit. Following an internal investigation, the company "chose not to voluntarily report to the relevant authorities." Disclosure was only made after the SEC formally requested documents. This decision led to a $137.4 million payment and a mandatory two-year monitoring period.

Albemarle, a specialty chemicals company, confirmed misconduct in one geographical region. However, it waited for over nine months before disclosing this information, while simultaneously reporting related conduct in three additional countries. The initial misconduct was deemed untimely, though the disclosures concerning the additional countries received partial credit. The total penalties levied against Albemarle amounted to approximately $196 million.

Walmart’s experience introduces another layer of complexity. The retail giant proactively disclosed misconduct in Brazil, China, and India before the government became independently aware of these issues, conduct that would typically qualify for voluntary disclosure credit. However, the company did not receive this credit because the government was already investigating related conduct in Mexico. The disclosure of misconduct in one region, it transpired, negatively impacted the credit available for disclosures in other regions.

Beyond a Simple Calculation: Risk Analysis and Strategic Disclosure

The enforcement record suggests that the decision to self-disclose is rarely a straightforward calculation based solely on the findings of an internal investigation. Instead, it typically involves a comprehensive risk analysis that weighs numerous factors, including the nature and prevalence of the misconduct, the individuals involved, and the potential reputational and financial consequences of both disclosure and non-disclosure.

As McDonald explained, "Part of that calculation is also what is the conduct, what does it look like, who was involved, how prevalent is it and all of those things kind of weigh more in favor of a potential self-disclosure than not."

The establishment and consistent reinforcement of a robust compliance culture are fundamental prerequisites for any successful self-disclosure strategy. A company’s ability to identify potential issues is severely hampered if employees are not encouraged to report concerns or if there are no effective channels for doing so. As McDonald emphasized, "Having a real compliance program, a real compliance culture where folks at the company are encouraged to report any issues… if you have no way to identify a potential issue, it really handicaps you as a company in terms of self-disclosure."

Implications for Corporate Compliance Programs

The ambiguity surrounding the definition of "timely" disclosure poses a significant challenge for corporate compliance departments. It necessitates a proactive and strategic approach, rather than a reactive one. Companies must:

- Develop Clear Internal Policies: Establish internal protocols for identifying, investigating, and reporting potential misconduct that are aligned with the spirit of the DOJ’s guidance, even in the absence of explicit timelines. This includes defining clear triggers for initiating investigations and setting internal deadlines for reporting to senior management and, if necessary, external authorities.

- Invest in Robust Compliance Infrastructure: A strong compliance program, including effective hotlines, training, and monitoring, is essential for early detection of potential issues. This proactive approach increases the likelihood of identifying misconduct before it is discovered by external parties.

- Conduct Thorough Risk Assessments: Regularly assess compliance risks across all business operations and geographies. This helps prioritize areas for heightened scrutiny and informs the decision-making process regarding disclosure.

- Engage Expert Legal Counsel: In situations involving potential misconduct, seeking prompt advice from experienced legal counsel specializing in white-collar defense and corporate compliance is crucial. Counsel can help assess the risks and benefits of self-disclosure and navigate the complex regulatory landscape.

- Document Everything: Meticulous record-keeping of all investigations, communications, and decisions related to potential misconduct is vital. This documentation can be critical in demonstrating a company’s commitment to compliance and its rationale for its actions.

The DOJ’s emphasis on voluntary and timely self-disclosure remains a cornerstone of its enforcement strategy. However, the lack of precise definitions for "timely" means that companies must operate with a heightened sense of caution and strategic planning. The enforcement record serves as a stark reminder that proactive engagement with compliance obligations, coupled with a clear understanding of the potential consequences of delay, is paramount in navigating the intricate landscape of corporate self-reporting. The ultimate goal for any organization is to move beyond a reactive stance and foster a culture where identifying and addressing potential wrongdoing is an ingrained and immediate process, thereby maximizing the chances of leniency should an issue arise.