The landscape of private equity is undergoing a significant transformation, marked by a burgeoning reliance on continuation vehicles (CVs). This trend, driven by a persistent thirst for liquidity and a challenging dealmaking environment, has led to a dramatic expansion of the secondary market. While CVs offer a vital lifeline for both general partners (GPs) and limited partners (LPs) grappling with illiquidity, questions are emerging about whether this phenomenon represents a fundamental structural shift in private equity exits or merely a temporary patch to address current market frictions.

The Liquidity Squeeze in Private Markets

Recent years have seen a pronounced tightening of liquidity within the private equity asset class. The period between 2022 and 2024 has been characterized by distributions lagging historical norms, impacting the crucial metric of distributions to paid-in capital (DPI). Data indicates that distributions as a percentage of Net Asset Value (NAV) have trailed historical averages by approximately 15%, falling from around 28% to 13%. This shortfall translates directly into lower DPI for recent fund vintages, with those from 2018-2021 being roughly 0.2 times lower than initially projected.

This decline in distributions has created a ripple effect, intensifying liquidity pressures for all stakeholders. A 2025 survey conducted by McKinsey highlighted this growing concern, revealing that limited partners (LPs) ranked DPI as the "most critical" performance metric 2.5 times more frequently than they had three years prior. This underscores a significant recalibration of LP priorities, moving beyond traditional capital appreciation to a more immediate focus on capital realization.

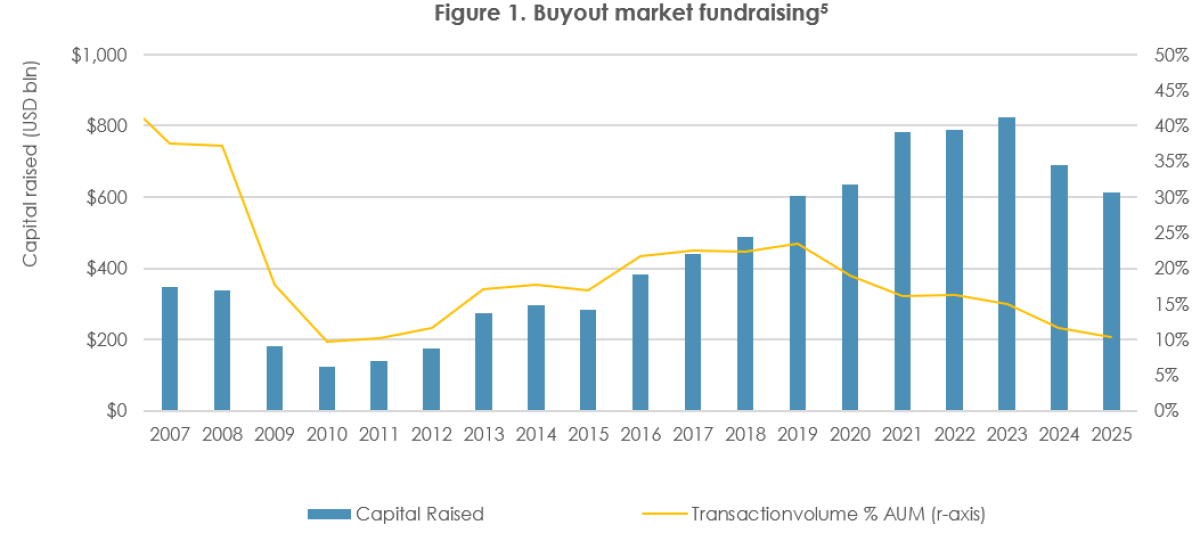

General partners (GPs) are equally cognizant of this liquidity drought. The challenges in realizing capital from existing investments directly impede their ability to raise new funds. With LPs’ private market exposure remaining elevated due to sluggish distributions, their allocation of new capital has become considerably more selective. The current fundraising environment sees a stark imbalance: for every $3 of targeted fundraising, only $1 of capital is currently available to commit, a significant departure from the historical ratio of 1.3:1. This scarcity is evident in the buyout segment, where fundraising levels relative to NAV reached their lowest point since the Global Financial Crisis (GFC) in the previous year, as depicted in Figure 1.

[Figure 1: Buyout Fundraising Relative to NAV (Illustrative Data Point – Actual data would be presented here if available from the source text)]

Continuation Vehicles: An Oasis in the Exit Desert

In response to these market dynamics, the secondary private equity market has witnessed explosive growth, fostering innovative transaction structures designed to capitalize on these imbalances. Initially conceived to provide liquidity to LPs seeking to exit their fund commitments, the secondary market has evolved to become a significant liquidity source for GPs as well. Faced with constrained traditional exit avenues, GPs are increasingly turning to GP-led secondary transactions as a means to access capital and manage their portfolio exposure.

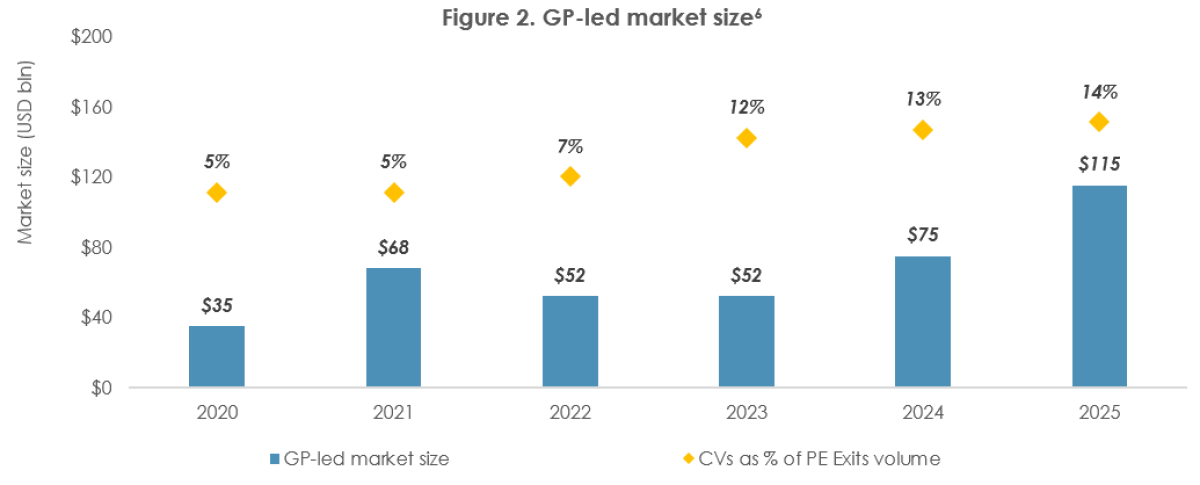

Within this expanding secondary market, continuation vehicles (CVs) have emerged as the dominant structure. In 2025 alone, GP-led secondary transaction volume surged to an estimated $115 billion. CVs accounted for a substantial 89% of this GP-led activity, representing approximately 43% of the total secondary market volume. These vehicles enable sponsors to retain control over high-conviction assets while offering existing investors the opportunity to receive liquidity, positioning CVs as an increasingly prevalent route for exiting investments. This trend suggests not only a greater reliance on secondary solutions due to a constrained exit market but also a potential structural evolution in how private equity assets are realized.

[Figure 2: Growth of GP-Led Secondary Transactions and Continuation Vehicle Volume (Illustrative Data Point – Actual data would be presented here if available from the source text)]

The adoption of GP-led CVs has transcended firm sizes, with nearly 75% of the largest global private equity firms having executed at least one continuation transaction. Furthermore, the investor base participating in these deals has broadened considerably. Beyond traditional secondary funds, direct LP investments and evergreen vehicles are increasingly engaging in these transactions. Continuation fund syndications have become more commonplace, capturing the largest share of LP direct secondary investments in the first half of 2025. Collectively, these developments indicate that continuation vehicles are now an integral component of private equity liquidity management, fundamentally reshaping liquidity options for both LPs and GPs.

Differentiating Continuation Vehicle Structures

The continuation vehicle market has bifurcated into two distinct structures: multi-asset continuation vehicles (MACVs) and single-asset continuation vehicles (SACVs). MACVs are often employed to facilitate liquidity across a fund’s remaining diversified assets, including those in wind-down scenarios. SACVs, conversely, are typically utilized for "trophy" assets – high-conviction investments that sponsors wish to retain and manage beyond the original fund’s lifespan.

Empirical evidence suggests a performance differentiation between these structures. SACVs are often associated with stronger asset performance and higher valuation metrics compared to MACVs. This distinction is reflected in their pricing, as illustrated in Figure 3, with SACVs commanding higher valuations due to their focus on premium assets and extended value-creation timelines. The shift towards single-asset exposure and premium pricing in SACVs necessitates a change in investor skill set, moving from manager selection to the direct underwriting of the underlying asset. This transition, however, introduces a heightened potential for conflicts of interest, demanding closer scrutiny.

[Figure 3: Valuation and Pricing Differences Between MACVs and SACVs (Illustrative Data Point – Actual data would be presented here if available from the source text)]

Navigating Conflicts of Interest

The proliferation of continuation vehicles introduces a complex web of potential conflicts of interest that warrant careful examination, particularly concerning the dual role of the GP.

Conflicts of Interest – The GP Perspective

- Valuation Bias: GPs, acting as both the seller of assets from an existing fund and the buyer for the new continuation vehicle, may be incentivized to present assets in a more favorable light to secure a higher valuation. This can lead to inflated pricing, benefiting the GP through management fees and potential carried interest in the new vehicle, while disadvantaging the selling LPs who might receive less than the asset’s true market value.

- Asset Selection: The GP’s decision-making in selecting which assets to roll into a continuation vehicle can be influenced by their desire to retain control over underperforming assets to avoid realizing losses in the original fund, or conversely, to cherry-pick high-performing assets for the new vehicle where they can continue to generate fees and performance fees.

- Fund Term Extension: The use of continuation vehicles can effectively extend the life of an existing fund beyond its contractual term, potentially delaying capital returns for LPs who wish to exit, and allowing GPs to continue earning management fees on assets that would otherwise be approaching liquidation.

- Fee Structures: The introduction of new fee structures within the continuation vehicle, in addition to existing management and performance fees from the original fund, can lead to an overall increase in fees paid by investors, eroding net returns.

- Carry Crystallization: GPs may prioritize the crystallization of carried interest in the continuation vehicle, potentially at the expense of optimal long-term value creation for the underlying assets.

From an LP perspective, these conflicts can be partially mitigated through independent valuations, adequate review periods, and the reinvestment of crystallized carry. However, LPs remain reliant on the GP’s discipline to ensure that value-creation initiatives are not unduly delayed for the sake of administrative convenience or immediate fee realization.

Conflicts of Interest – The LP Perspective

From the perspective of LPs, continuation vehicles introduce a more intricate decision-making process. GPs often compress timelines in these processes due to the additional re-underwriting and asset diligence required. GPs aim for efficient transaction execution, while LPs must simultaneously assess "sell-or-roll" requests across multiple funds. For LPs lacking dedicated expertise in deal underwriting, this compressed timeline can limit the depth of their review, forcing them to choose between liquidity and potentially uncertain future returns.

Furthermore, these transactions alter the traditional risk and return profile of secondary market exposure. Single-asset continuation vehicles shift the secondary market away from diversified, shorter-duration portfolios towards more concentrated positions with extended holding periods. This fundamentally weakens the historical portfolio characteristics that have underpinned secondary allocations, challenging their traditional role as a source of early liquidity and diversification. Consequently, LPs face diminished diversification benefits, slower distributions, and reduced countercyclical protection due to potentially elevated discounts.

Broader Implications for Private Market Allocations

As continuation vehicles become increasingly embedded in private markets, their impact extends to the overall liquidity profile of a portfolio. Within buyout strategies, CVs have served as an additional liquidity mechanism when traditional exit routes are constrained. However, transaction pricing in continuation vehicles is often skewed below prior reported NAV, potentially resulting in realized returns below previous valuation assumptions compared to a traditional exit. Moreover, by extending holding periods, continuation vehicles fundamentally alter the liquidity characteristics of secondary investments. This has significant implications for cash management, as slower distributions can exacerbate the already limited liquidity of primary investments. The expansion of GP-led secondary activity signals a departure from the assumption of shorter holding periods and early liquidity.

Conclusion: A Structural Shift or a Temporary Solution?

Continuation vehicles have undeniably reshaped the private markets landscape, offering a novel exit route for sponsors. In periods of constrained exit markets, GP-led transactions have provided a crucial mechanism for generating liquidity and managing portfolio exposure, accounting for approximately 14% of exits during 2025. This has facilitated deal execution when traditional exits have been challenging to achieve.

However, this evolution introduces complexities that demand careful scrutiny. Continuation vehicles are increasingly extending asset holding periods beyond original fund mandates, blurring the economic boundaries of closed-ended structures. This development challenges the traditional role of secondaries within a diversified portfolio and undermines the assumptions around liquidity that underpin private market allocations. Consequently, LPs must revisit their strategic asset allocation assumptions to account for potentially longer value creation timelines and altered liquidity profiles.

For GPs, continuation vehicles should be treated as a clearly defined component of their exit toolkit, not a universal solution. This necessitates transparency regarding the rationale for choosing a continuation vehicle over traditional exit routes and how such decisions align with predetermined value creation objectives. LPs, in turn, must critically assess how GPs integrate continuation vehicles into their investment and exit frameworks and the implications for expected liquidity timing. While continuation vehicles have proven instrumental in navigating difficult exit conditions, their broader, long-term implications for portfolio construction, risk management, and investor alignment require meticulous oversight and strategic adaptation. The continued evolution of this market will be closely watched to determine whether it solidifies as a permanent structural component of private equity or remains a sophisticated, albeit temporary, solution to cyclical liquidity challenges.

Learn more about CAIA Association and how to become part of a professional network that is shaping the future of investing, by visiting https://caia.org/.