The private equity landscape is undergoing a significant transformation, driven by a persistent thirst for liquidity among both investors (LPs) and fund managers (GPs). In a market characterized by increasing frictions in traditional dealmaking and exit avenues, continuation vehicles (CVs) have emerged as a dominant and rapidly expanding solution. While offering a much-needed lifeline for asset monetization and portfolio management, the proliferation of CVs raises critical questions about whether this trend represents a fundamental structural shift in private equity operations or merely a temporary patch to address prevailing liquidity challenges.

The Growing Liquidity Squeeze in Private Equity

The current market environment has starkly illuminated the inherent illiquidity of private equity investments. For General Partners (GPs), the ability to return capital to their Limited Partners (LPs) has become a paramount concern. Between 2022 and 2024, distributions as a percentage of Net Asset Value (NAV) have fallen significantly below historical norms, reportedly trailing by approximately 15% (averaging 13% compared to a historical average of 28%). This shortfall directly impacts the Distributions to Paid-In Capital (DPI) metric, a key indicator of investment performance. For vintage years 2018-2021, DPI is running about 0.2x lower than initially projected, intensifying liquidity pressures across the private equity ecosystem.

This liquidity crunch has had a profound effect on LP sentiment and behavior. A 2025 survey conducted by McKinsey revealed a substantial shift in LP priorities, with 2.5 times as many LPs ranking DPI as the "most critical" performance metric compared to just three years prior. This heightened focus on capital realization underscores a growing impatience with prolonged holding periods and a desire for more predictable cash flows.

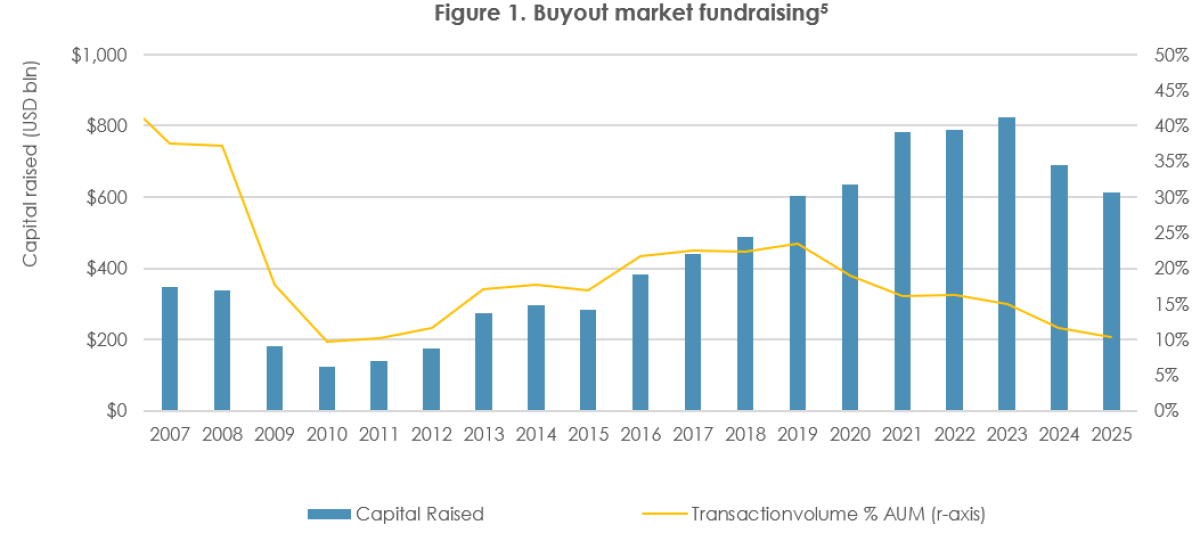

GPs are equally cognizant of the tightening liquidity. The subdued distribution environment has kept LPs’ existing private market exposure elevated, leading them to become highly selective in allocating new capital. The current fundraising environment is illustrative of this challenge: for every $3 of targeted fundraising, only $1 of capital is currently available to commit, a stark contrast to the historical ratio of 1.3:1. In the past year, buyout fundraising reached its lowest level relative to NAV since the Global Financial Crisis, underscoring the difficulty GPs face in replenishing their capital reserves.

Continuation Vehicles: An Oasis in the Exit Desert

Against this backdrop of constrained exit markets and increased demand for liquidity, the secondary private equity market has experienced rapid expansion. Initially conceived to provide liquidity primarily to LPs seeking to divest their holdings, the secondary market has evolved to become a significant source of capital for GPs as well. This evolution has been driven, in large part, by the increasing reliance on GP-led secondary transactions, particularly those involving continuation vehicles (CVs).

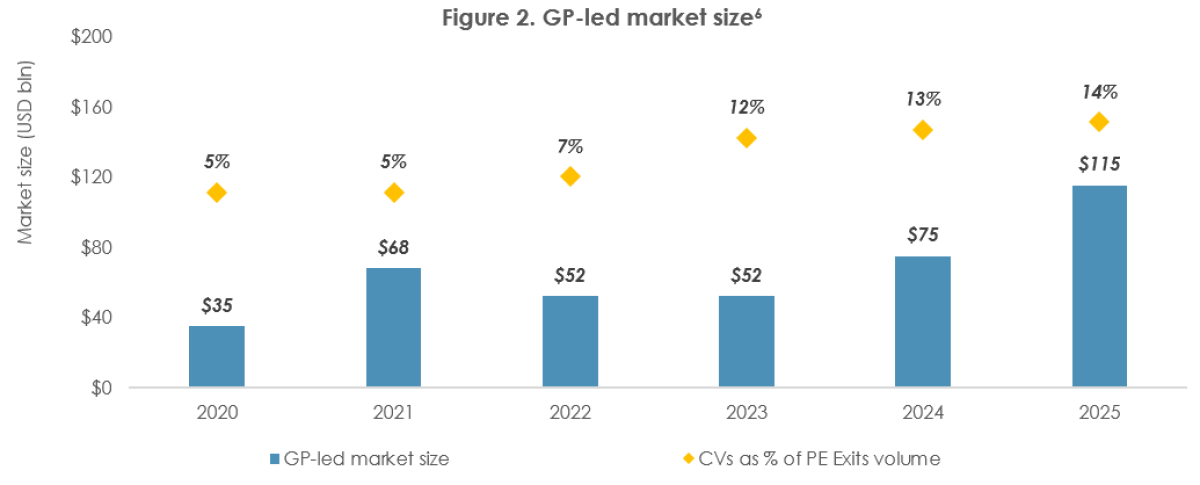

Continuation vehicles have rapidly become the dominant structure within the GP-led secondary segment. In 2025 alone, GP-led secondary transaction volume reached an estimated $115 billion. CVs accounted for the vast majority of this activity, representing approximately 89% of GP-led volume and a substantial 43% of the total secondary market volume.

These vehicles serve a dual purpose: they enable sponsors to retain control over high-conviction assets that they believe still hold significant potential for value creation, while simultaneously providing liquidity to existing investors who wish to exit their positions. This makes CVs an increasingly common and attractive route to achieving a form of exit, even when traditional sale or IPO pathways are challenging. The significant growth in CV activity suggests not only a greater reliance on secondary solutions in the face of exit market constraints but also a potential structural shift in how private equity firms approach asset realization and portfolio management.

The adoption of GP-led CVs has become widespread, with nearly 75% of the largest global private equity firms having executed at least one continuation transaction. Furthermore, the investor base participating in these transactions has broadened considerably. Alongside traditional secondary funds, direct LP investments and evergreen vehicles are increasingly playing a role. Continuation fund syndications, where multiple investors pool capital to acquire assets within a CV, have become more frequent and represented the largest share of LP direct secondary investments in the first half of 2025. These developments collectively indicate that continuation vehicles are no longer a niche product but an embedded component of private equity liquidity management, reshaping options for both LPs and GPs.

Diversification Within Continuation Vehicles: MACVs vs. SACVs

The continuation vehicle market itself has further differentiated into two primary structures: multi-asset continuation vehicles (MACVs) and single-asset continuation vehicles (SACVs).

MACVs are typically employed to facilitate liquidity across a broader portfolio of a fund’s remaining assets, often as part of a fund’s wind-down process. This structure allows for the monetization of multiple underlying investments simultaneously, providing a more comprehensive liquidity solution for LPs looking to exit a mature fund.

In contrast, SACVs are more commonly utilized for "trophy" assets – high-conviction, flagship investments that sponsors believe have exceptional potential for further value creation and wish to retain beyond the original fund’s life. Early empirical evidence suggests a performance differentiation between these two structures. SACVs are often associated with stronger underlying asset performance and higher valuation metrics compared to MACVs.

This divergence in asset quality and performance potential leads to material differences in pricing, with SACVs typically commanding higher valuations. The shift in focus from a diversified fund portfolio to a concentrated, high-conviction asset in SACVs means that the required investor skill set moves from manager selection towards a more direct underwriting of the underlying asset’s specific potential and risks. This evolution inherently expands the scope for potential conflicts of interest, necessitating closer scrutiny from all parties involved.

Navigating the Complexities: Conflicts of Interest

The increasing prevalence of continuation vehicles introduces a complex web of potential conflicts of interest that warrant careful examination. These conflicts primarily stem from the GP’s dual role as both the seller of assets from an existing fund and the manager of the new continuation vehicle acquiring those assets.

From the GP’s Perspective:

- Valuation and Pricing: GPs have an inherent incentive to secure the highest possible valuation for the assets being transferred to the CV, as this directly impacts the returns for the exiting LPs and the carried interest potential for the GP in the new structure. This can create a conflict if the valuation is perceived as overly optimistic or not fully reflective of market realities.

- Deal Structure and Fees: GPs may be incentivized to favor CV structures that offer additional fee streams (e.g., management fees on the CV, transaction fees) even if alternative exit routes might be more beneficial for LPs in the long run.

- Selective Asset Transfer: GPs might strategically choose to move underperforming or less desirable assets into a CV to clear out their existing fund, while retaining the "best" assets for future funds or personal investment.

- Information Asymmetry: GPs possess superior knowledge of the underlying assets’ performance and future prospects compared to incoming investors in the CV. This asymmetry can be exploited if not managed with transparency.

- Conflict of Interest in Sale Process: When a GP is responsible for both selling an asset from a prior fund and potentially buying it for a new vehicle, the integrity of the sale process can be compromised if not overseen by an independent third party.

While these conflicts present challenges, certain mitigation strategies can be employed. From an LP perspective, independent valuations, adequate review periods for proposed transactions, and the reinvestment of crystallized carried interest by the GP can help to align interests. However, ultimately, LPs must rely on the sponsor’s discipline to ensure that the implementation of value-creation initiatives is not unduly delayed in favor of the GP’s ongoing management fee structure.

From the LP’s Perspective:

- Compressed Timelines and Due Diligence: GP-led processes often involve compressed timelines. LPs are frequently presented with "sell or roll" decisions for their existing stakes, requiring them to conduct re-underwriting and asset diligence within tight windows. For LPs lacking dedicated expertise in deal underwriting, this can limit the depth of review, forcing difficult choices between liquidity and the potential for future returns.

- Altered Risk and Return Profiles: The shift from diversified, shorter-duration portfolios often found in traditional secondaries to more concentrated positions with extended holding periods within SACVs fundamentally alters the risk and return profile of secondary exposure. This can weaken the historical portfolio characteristics that have underpinned secondary allocations, such as providing early liquidity and diversification benefits.

- Reduced Diversification and Slower Distributions: Single-asset CVs inherently reduce diversification benefits. Furthermore, the extended holding periods associated with these vehicles lead to slower distributions, compounding the already limited liquidity of primary private equity investments.

- Less Countercyclical Protection: Elevated discounts on secondary portfolios in challenging markets have historically offered countercyclical protection. With the rise of CVs, particularly those driven by GPs seeking to retain assets, these discounts may be less pronounced, diminishing this protective aspect.

- Impact on Portfolio Liquidity: As CVs become more ingrained, they significantly influence a portfolio’s overall liquidity profile. While they offer an additional liquidity mechanism when traditional exits are constrained, the pricing in CVs is often skewed below prior reported NAV. This can result in realized returns that are lower than initial valuation assumptions when compared to a traditional exit. Moreover, by extending holding periods, CVs alter the liquidity characteristics of secondary investments, impacting cash management and cash flow planning for LPs.

Broader Implications and Future Outlook

The rise of continuation vehicles signifies a fundamental reshaping of the private markets landscape. They have created a novel exit route for sponsors, particularly critical during periods of constrained traditional exit markets like M&A and IPOs. In 2025, GP-led transactions accounted for an estimated 14% of all exits, demonstrating their growing importance in facilitating liquidity and portfolio management when traditional avenues are more challenging to navigate.

However, this trend is not without its complexities. Continuation vehicles are increasingly extending asset holding periods beyond the original fund mandates, effectively blurring the economic boundaries of traditional closed-ended fund structures. This development challenges the established role of secondaries within an LP’s portfolio, which has historically been viewed as a source of early liquidity and diversification. It also calls into question the fundamental assumptions around liquidity that are embedded in private market allocations.

Consequently, LPs are being compelled to revisit their strategic asset allocation assumptions. They must now account for potentially longer value creation timelines and a more nuanced understanding of liquidity within their private equity portfolios. The traditional expectation of shorter holding periods and early liquidity can no longer be taken for granted in the context of GP-led secondary activity.

For GPs, continuation vehicles should be treated as a clearly defined component of their overall exit toolkit, rather than a default solution. This requires greater transparency regarding the rationale for choosing a CV over traditional exit routes and a clear articulation of how such decisions align with predetermined value creation objectives. LPs, in turn, must diligently assess how GPs integrate continuation vehicles into their investment and exit frameworks and what implications this has for expected liquidity timing and overall portfolio performance.

While continuation vehicles have undoubtedly provided a valuable mechanism for execution during difficult exit conditions, their broader, long-term implications for portfolio construction, risk management, and investor returns require careful and ongoing management by all stakeholders in the private equity ecosystem. The continued evolution of this market will likely see further innovation in deal structures and increased demand for robust governance and independent oversight to ensure fair outcomes for all parties involved.