The landscape of executive outlook has subtly, yet significantly, shifted. In May, a notable decrease in the percentage of U.S. Chief Executive Officers anticipating business condition improvements over the next twelve months signals a collective move toward a more reserved, "wait and see" approach. This recalibration in sentiment, reflected in the latest Chief Executive CEO Confidence Index, is driven by a confluence of persistent geopolitical tensions, escalating costs, and a pervasive sense of policy uncertainty that is tempering previously held optimism. While the overall mood has not plummeted into outright pessimism, the trend indicates a hesitance to project robust growth, a marked departure from earlier in the year.

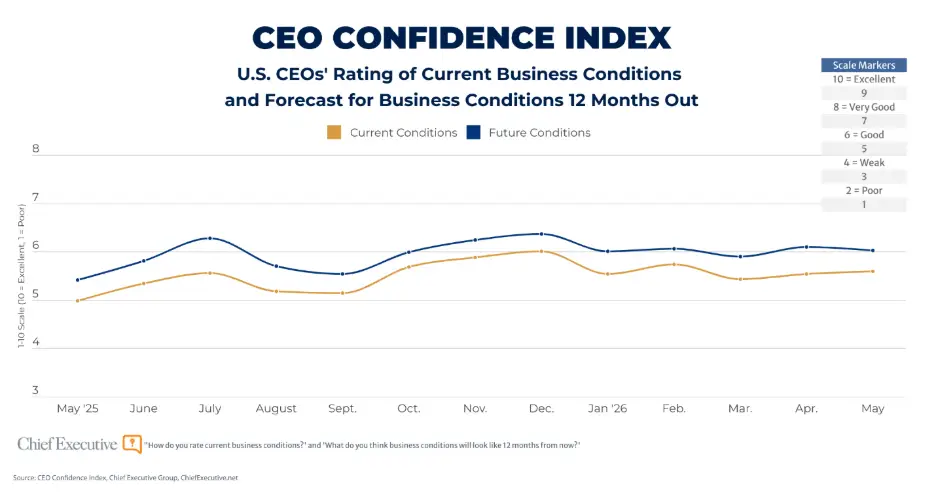

The Chief Executive May CEO Confidence Index, a comprehensive survey polling nearly 350 U.S. CEOs between May 5th and 6th, reveals a marginal dip in expectations for future business conditions. Specifically, the share of CEOs forecasting improvement over the next year fell to 48 percent in May, down from 52 percent in April. This slippage, though seemingly modest, underscores a growing prudence among business leaders. Importantly, the survey data indicates that this shift is not necessarily a sign of deteriorating current business environments. The perception of present conditions remained largely stable, with CEOs rating them at 5.6 out of 10, a slight increase from April’s 5.5 and holding near the year’s second-highest reading of 5.7 recorded in February. This suggests that while current operations may be holding steady, the outlook for the medium-term future is being viewed through a more cautious lens.

The forward-looking component of the index, which gauges the 12-month outlook, also showed a slight moderation, settling at 6.0 out of 10 compared to 6.1 in April. This translates to an anticipated improvement of approximately 8 percent by this time next year. This figure has remained relatively consistent since the beginning of 2026, hovering around this mark. However, some chief executives acknowledge that this forward-looking expectation carries an element of aspirational thinking. As one CEO of a family-owned healthcare business candidly noted, "It’s human nature. We like to anticipate change for the better." This sentiment highlights a psychological tendency for leaders to hope for positive developments, even as external factors warrant a more measured assessment.

The underlying drivers of executive sentiment remain consistent with those observed in recent months, encompassing geopolitics, cost pressures, demand dynamics, and policy uncertainties. However, the May data reveals a more nuanced impact of these forces, with CEOs interpreting them in diverging ways.

Geopolitical Ripples and Divergent Interpretations

Geopolitical developments, particularly the ongoing conflict in Iran, continue to be a significant factor influencing CEO outlooks. Notably, 57 percent of CEOs who anticipate worsening business conditions cited geopolitical concerns as a primary driver. However, a substantial 43 percent of those expecting improvement also pointed to geopolitical factors, albeit with a more optimistic interpretation. For those forecasting a downturn, concerns often revolve around potential trade disruptions, escalating supply chain vulnerabilities, volatile energy costs, and a general dampening of consumer demand stemming from global instability.

Conversely, for a segment of optimistic leaders, geopolitical events are viewed as potential catalysts for positive change. One CEO expressed anticipation for a swift resolution to the Iran conflict, envisioning it leading to reduced oil prices and a subsequent boost in consumer confidence. Another echoed this sentiment, hoping for a calming of geopolitical tensions which would, in turn, foster a resurgence in consumer confidence. This dichotomy in interpreting geopolitical events underscores the complex and often contradictory nature of their impact on business strategy and outlook. The interconnectedness of global markets means that events in one region can have far-reaching and varied consequences, necessitating careful analysis by business leaders.

The Double-Edged Sword of Costs and Inflation

Inflationary pressures and rising costs remain a critical concern for U.S. businesses. Forty-six percent of pessimistic CEOs identified costs or inflation as key factors influencing their forecasts. Yet, a significant 38 percent of optimistic CEOs also acknowledged these economic headwinds, suggesting that while they are a concern, they are not necessarily a insurmountable barrier to future growth for all.

For some, the escalating cost of goods and services is directly impacting consumer behavior and, consequently, demand. One CEO lamented, "Uncertainty of future costs is influencing demand." This indicates a cautious approach from consumers, who may be delaying purchases or reducing discretionary spending due to concerns about their own financial stability.

However, others foresee potential relief on the horizon. A more hopeful perspective suggests that a decline in energy prices, such as gasoline, could lead to a broader reduction in overall costs, thereby easing the pressure on both businesses and consumers. This expectation of moderating inflation is crucial for forecasting future profitability and investment decisions. The average 12-month forecast for the Headline Consumer Price Index (CPI) rate has indeed eased in May to 3.6 percent, down from 4.6 percent in April. This brings the expectation back in line with earlier months’ readings of around 3.5 percent.

Demand as a Beacon of Hope

Despite the prevailing uncertainties, demand remains a significant driver of optimism for a considerable portion of CEOs. Thirty-eight percent of optimistic leaders cited factors such as customer engagement, market activity, order pipelines, project backlogs, and emerging growth opportunities as the basis for their positive outlook.

A chief executive from a large construction firm, for instance, projected business conditions for the next year at an impressive 8 out of 10, considerably above the average. Their optimism was fueled by "strong new project orders, growing backlog, and increasing opportunities." This indicates a robust pipeline of work that provides a buffer against short-term economic fluctuations.

Another executive highlighted positive trends in quote activity and year-to-date booked results, noting their ability to absorb cost increases so far. They observed a tangible increase in purchase orders (POs) and requests for quotations (RFQs), suggesting a market that, while cautious, is actively engaging and signaling potential for future business. This sentiment reflects a dynamic where underlying demand, particularly in sectors with strong project pipelines, is helping to offset broader economic anxieties.

The Rise of the "Status Quo" Mentality

While fewer CEOs are projecting a robustly improving business environment, there is also a notable absence of a sharp turn towards outright pessimism. The percentage of CEOs expecting conditions to worsen remained relatively stable at 23 percent, a figure largely unchanged from the previous month. The most significant shift occurred in the middle ground: 30 percent of CEOs now anticipate business conditions to remain flat, an increase from 26 percent in April.

This trend aligns with the qualitative feedback gathered from the survey. Many CEOs described a business environment where operations are ongoing, but limited visibility makes accurate long-term forecasting exceptionally challenging. The constant stream of global events, from geopolitical conflicts to evolving economic policies, creates an environment where making definitive long-term strategic decisions is fraught with difficulty.

As one CEO of a mid-sized professional services firm articulated, there is "a non-stop stream of events standing in the way of leaders making long-term decisions." This sentiment of perpetual uncertainty is a defining characteristic of the current business climate. Similarly, an executive from an upper-middle-market firm, despite acknowledging a "strong backlog presently, and opportunities are still strong," conceded that "uncertainty in the world creates a less optimistic look for the next year." This underscores the psychological impact of global instability on executive confidence, even when current business fundamentals appear sound.

Economic Forecasts: A Moderating, Yet Still Elevated, Inflationary Outlook

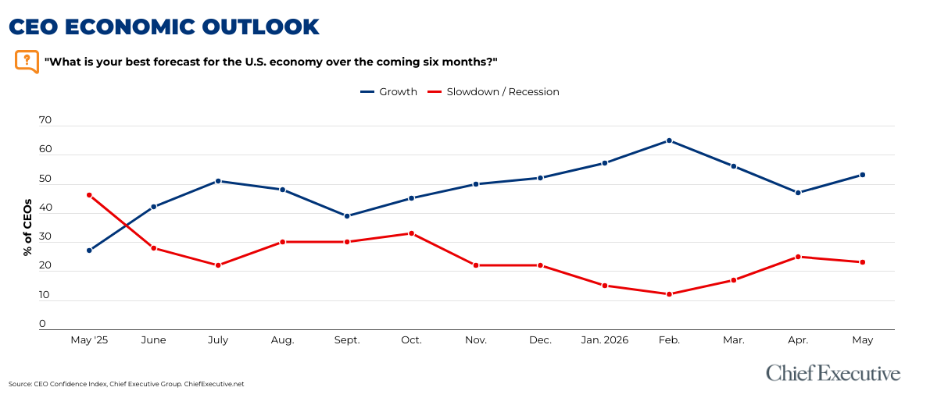

Beyond the immediate business outlook, the survey also delved into broader economic forecasts, revealing further nuances in CEO expectations. Recession forecasts, which had spiked in April to a six-month high, showed signs of easing in May. A slim majority of CEOs, 53 percent, now anticipate economic growth in the coming months. However, this figure remains considerably below the 65 percent peak observed in February, prior to the escalation of the conflict in Iran. This indicates a lingering apprehension about the potential for an economic downturn, even as the immediate fear of recession may be subsiding slightly.

Inflation expectations have also moderated, albeit with a cautionary note. The average forecast for the 12-month Headline CPI rate has decreased to 3.6 percent from 4.6 percent in April. This brings the average expectation back to levels seen earlier in the year. However, when examining the median forecast, a slightly different picture emerges. The median inflation forecast has steadily edged higher throughout the year, moving from 3.0 percent in February and March to 3.3 percent in April and reaching 3.5 percent in May. This suggests that while the most extreme inflation predictions have receded, a significant portion of CEOs still anticipate inflation settling at a somewhat higher level than they did at the beginning of the year. This persistent expectation of elevated inflation has implications for pricing strategies, wage negotiations, and investment decisions.

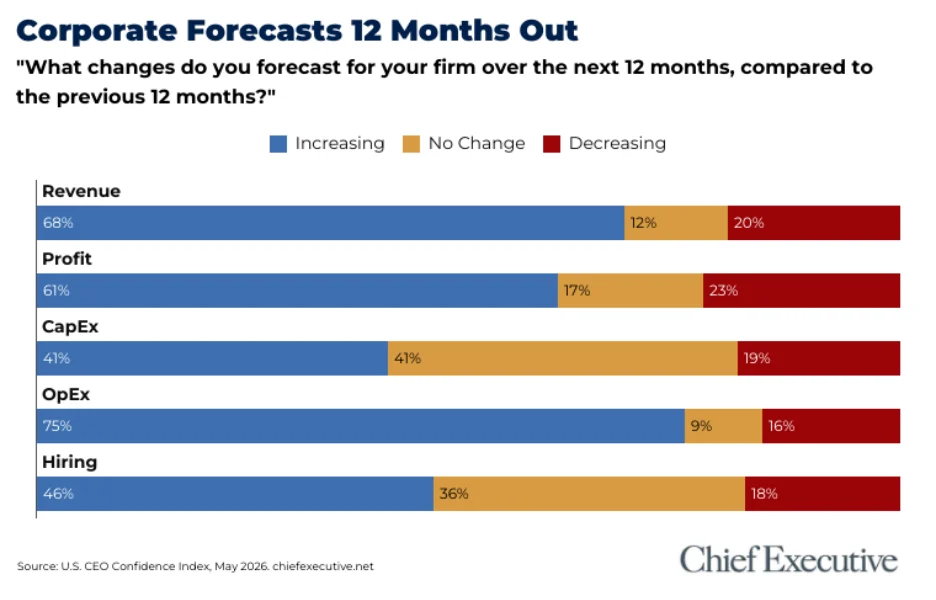

Corporate Forecasts: Hiring Gains Momentum, Expenses Remain High

The cautious sentiment is also reflected in how CEOs are projecting the performance of their own companies. While specific details for corporate revenue, profit, and capital expenditure forecasts were not provided in the snippet, the broader trend suggests a recalibration of internal targets and investment plans in response to the external environment.

Hiring stands out as a notable exception to the general moderation. Forty-six percent of CEOs now plan to increase headcount this year, a slight uptick from 44 percent in April. This indicates that, despite economic uncertainties, businesses are still seeking to expand their workforce, perhaps to meet existing demand or to prepare for future growth. However, this figure remains substantially below the beginning of the year, when 53 percent of CEOs anticipated hiring increases, suggesting that the pace of recruitment has slowed compared to earlier projections.

On the cost front, operating expenses continue to be a significant concern. A substantial 75 percent of CEOs expect their operating expenses to increase over the next 12 months, according to the May survey. This persistent expectation of rising costs, encompassing everything from raw materials and energy to labor and logistics, underscores the ongoing inflationary pressures that businesses are facing and will likely continue to grapple with. This sustained increase in operating expenses can impact profit margins and may necessitate difficult decisions regarding pricing, efficiency, and investment.

Broader Implications and the Path Forward

The shift in CEO sentiment towards a "wait and see" approach signals a period of heightened strategic deliberation for businesses across the U.S. The confluence of geopolitical instability, persistent cost pressures, and policy ambiguity creates a complex operating environment. While current business conditions may be stable, the tempered outlook for the next twelve months suggests that companies are prioritizing resilience and adaptability over aggressive expansion.

The divergence in how CEOs interpret global events like geopolitical tensions and inflation highlights the individualized nature of business strategy. Companies with strong market positions, diversified supply chains, and robust demand pipelines are better equipped to navigate these challenges and even find opportunities amidst uncertainty. Conversely, those more exposed to volatile commodity prices, geopolitical risks, or sectors sensitive to consumer spending may find it more challenging to project confidence.

The moderating, yet still elevated, inflation expectations suggest that the Federal Reserve and other central banks will likely continue to monitor price pressures closely. The median forecast’s upward trend, even as the average declines, indicates that the lingering concern about inflation remains a key factor influencing economic outlook.

Ultimately, the May CEO Confidence Index paints a picture of an economy at a crossroads. While outright pessimism is not dominant, the fading optimism and the embrace of a cautious stance suggest that businesses are bracing for a period of continued uncertainty. The coming months will be critical in determining whether geopolitical tensions de-escalate, cost pressures recede, and policy frameworks provide greater clarity, thereby shifting the needle back towards more robust optimism, or if the current environment of cautious observation will persist, shaping a more measured trajectory for the U.S. economy. The ability of businesses to adapt, innovate, and manage costs effectively will be paramount in navigating this complex landscape.