In recent years, the ownership of a natural gas power plant in the United States often felt like a precarious proposition, a challenging asset to integrate into private infrastructure portfolios. However, the landscape has dramatically shifted, transforming these once-doubtful holdings into some of the most coveted assets. Investors who astutely recognized and acted upon this evolving market dynamic have seen significant rewards. To fully grasp this turnaround, tracing the arc from a period of immense growth and subsequent decline to its current resurgence is essential, revealing a complex interplay of market forces, technological advancements, and geopolitical influences.

From Boom to Bust: The Shifting Tides of Natural Gas Power

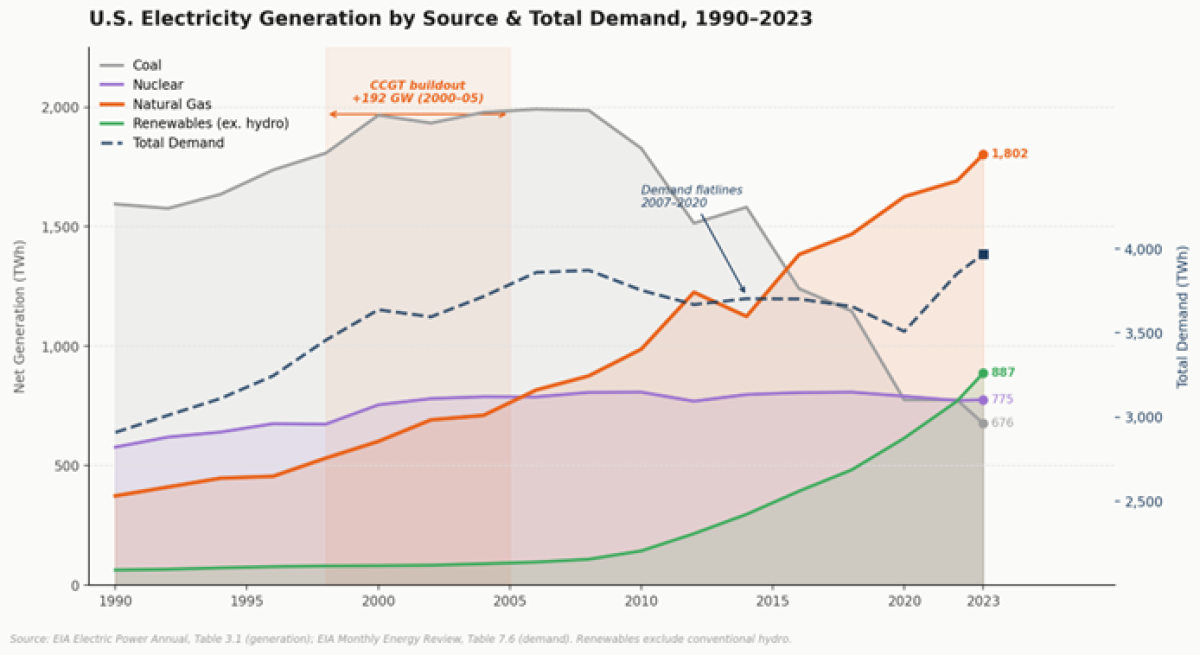

The late 1990s and early 2000s marked a golden era for the U.S. natural gas power sector. This period was characterized by a confluence of factors that fueled substantial generation expansion. The deregulation of electricity markets created opportunities for independent power producers and infrastructure sponsors to raise billions in capital. Coupled with the availability of cheaper natural gas and a growing demand for electricity, this environment spurred the widespread construction of highly efficient combined cycle gas turbines (CCGTs). These plants quickly became indispensable components of the American power grid, prized for their flexibility and lower emissions compared to older coal-fired facilities.

However, around 2007, the prevailing market conditions began to change. Electricity demand growth, which had been a consistent driver, started to plateau. Simultaneously, the renewable energy sector experienced a meteoric rise, significantly boosted by federal tax credits and rapidly declining installation costs. This surge in renewables, alongside a precipitous decline in coal-fired power generation, began to reshape the energy mix. Despite these shifts, natural gas generation continued to grow, ultimately solidifying its position as the dominant source of electricity generation in the U.S.

Chart 1: U.S. Electricity Generation by Source & Total Demand, 1999-2023

(Visual representation of the shift in energy sources and overall demand over the specified period, indicating the rise of renewables and gas, and the decline of coal.)

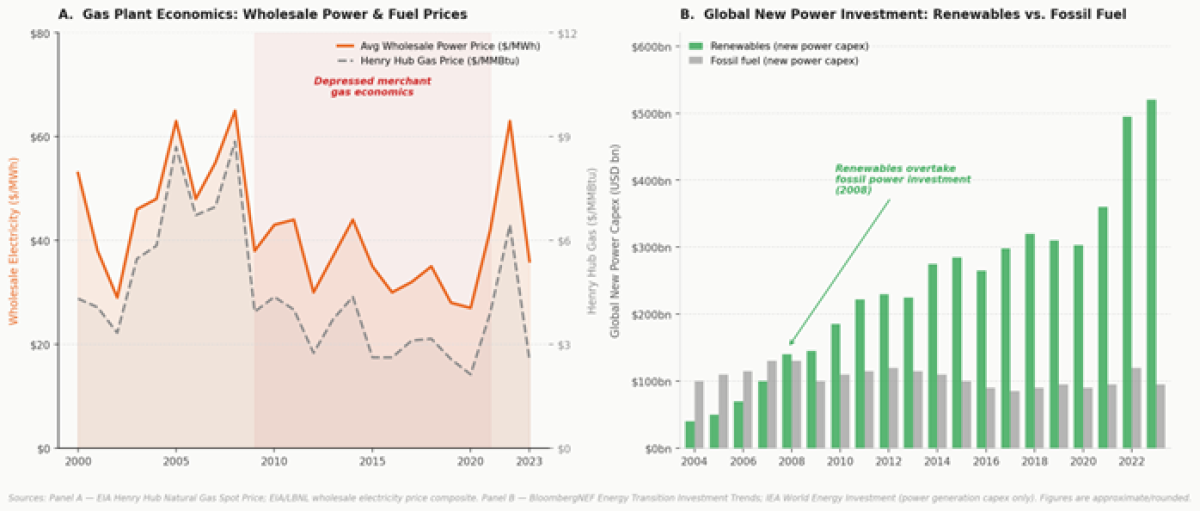

By the early 2020s, the economic viability of merchant gas plants – those selling power into the wholesale market without long-term contracts – faced significant headwinds. A decade of persistently low power prices had eroded their cash flows, leading to a wave of bankruptcies and distressed asset sales. Many projects struggled to meet their debt obligations, signaling a clear market sentiment. Infrastructure investors, in response, largely shifted their focus away from natural gas, prioritizing renewables as the present and future of energy investment.

Chart 2: Panel A. Gas Plant Economics: Wholesale Power & Fuel Prices and Panel B. Global New Power Investment: Renewables vs. Fossil Fuel

(Visual representation illustrating the pressure on gas plant economics due to price fluctuations and the comparative investment trends between renewables and fossil fuels globally.)

The Demand Shock: AI and Electrification Drive a New Era

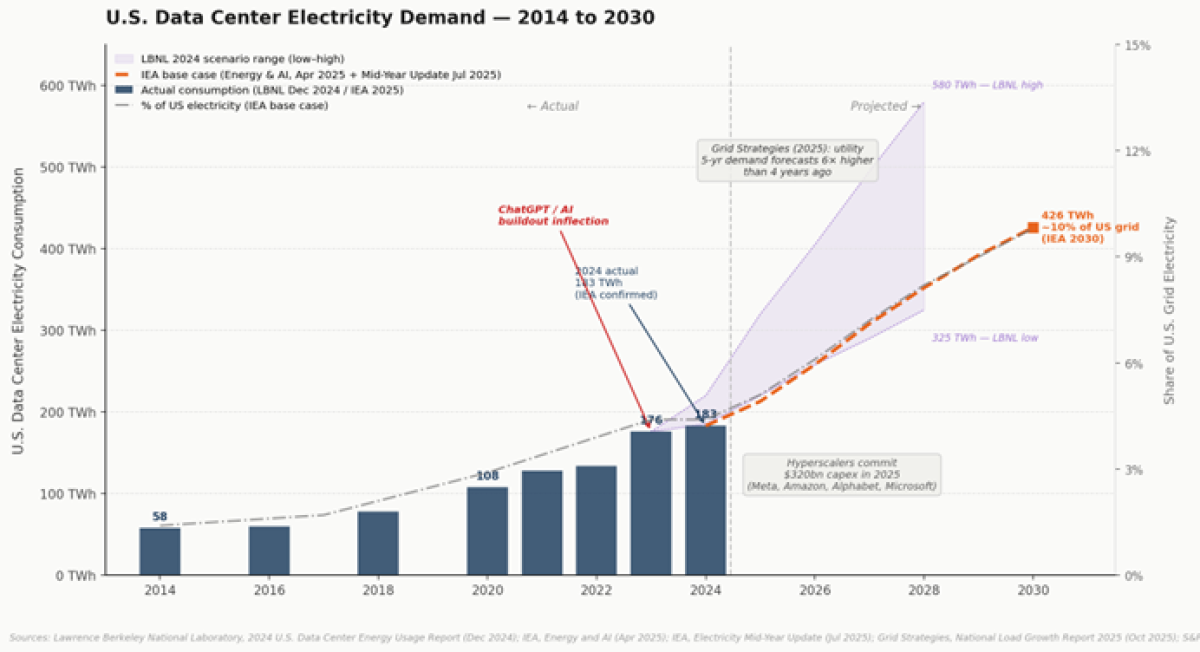

A dramatic reversal in this trend began to emerge in 2023, largely catalyzed by the explosive growth of artificial intelligence (AI). The insatiable energy demands of data centers, the backbone of AI development and deployment, are fundamentally altering the U.S. electricity consumption profile. In 2023, data centers accounted for approximately 4% of total U.S. electricity consumption. Projections now indicate this share could surge to between 10% and 12% by 2028, as hyperscalers race to build out the immense compute capacity required for training and inference workloads associated with large language models and other advanced AI applications. The power requirements for these AI applications are orders of magnitude greater than traditional enterprise computing, and this demand is not only accelerating but shows no signs of deceleration in the foreseeable future.

Chart 3: U.S. Data Center Electricity Demand – 2014 to 2030

(Visual representation forecasting the significant increase in electricity demand from data centers.)

The impact of data centers is not an isolated phenomenon. Simultaneously, the broader trend of electrification across various sectors is placing unprecedented strain on the U.S. power grid. The electrification of transportation, including the rapid adoption of electric vehicles, the decarbonization efforts within industrial processes, and the reshoring of domestic manufacturing, are all contributing to a substantial increase in electricity demand. This compounding demand is being layered onto a grid system where, in many regions, little new dispatchable capacity has been added in the last decade. Consequently, grid operators are now projecting sustained tightening of reserve margins – the buffer of available generation capacity – to levels not seen in a generation.

The growth of renewable energy sources, while crucial for long-term decarbonization, cannot single-handedly address this immediate challenge of reliable, dispatchable power. Wind and solar power remain inherently intermittent, their output dependent on weather conditions. While battery storage technologies are advancing rapidly, current solutions typically provide only hours of backup power, not the continuous reliability required to balance the grid under all conditions. When the grid demands power, particularly during peak periods or unexpected outages, natural gas plants are the assets that are called upon to provide this essential dispatchable capacity. This operational reality, which may have been downplayed in policy discussions, is now impossible to ignore.

The Structural Advantage: U.S. Natural Gas Costs and Geopolitical Realities

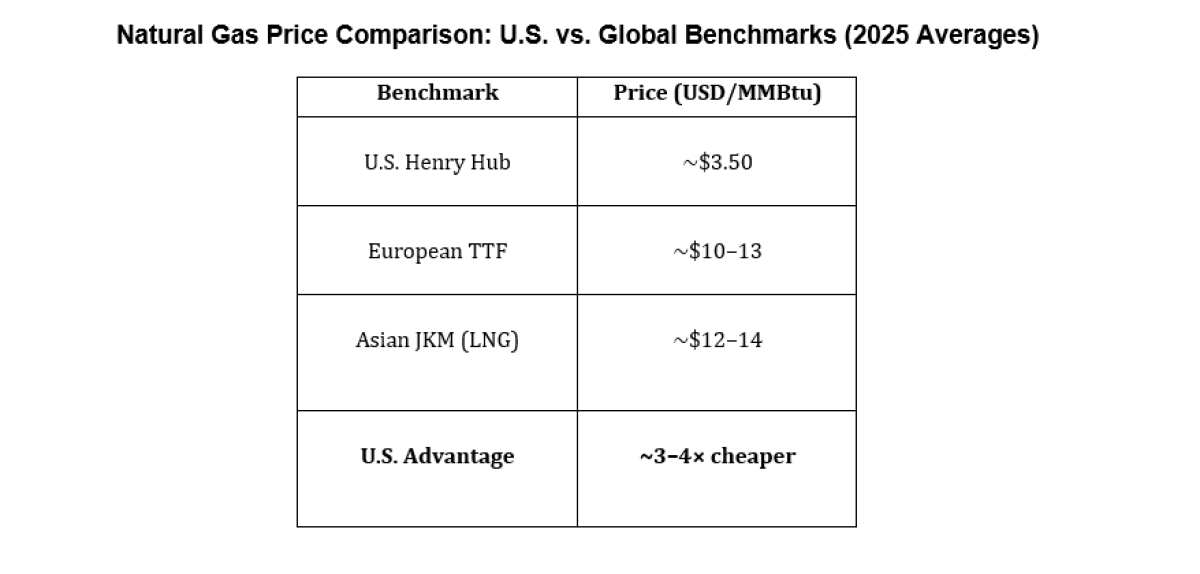

A critical factor underpinning the resurgence of natural gas power in the U.S. is the enduring cost advantage of domestically produced natural gas. U.S. natural gas production is forecasted to reach record highs, projected to be between 120 and 122 billion cubic feet per day through 2026-2027. This abundant domestic supply is expected to keep U.S. natural gas prices structurally lower than international import benchmarks in Europe and Asia. For gas-fired power generators, the cost of fuel represents the primary variable expense. Therefore, well-positioned U.S. natural gas plants benefit significantly from their proximity to this ample, low-cost supply. This inherent advantage has been further reinforced by recent geopolitical events, including the ongoing conflict in Ukraine and tensions in the Middle East, which have placed additional upward pressure on global energy import prices, widening the cost differential for U.S. producers and consumers.

Chart 4: Natural Gas Price Comparison: U.S. vs. Global Benchmarks (2025 Averages)

(Visual representation comparing projected U.S. natural gas prices against global benchmarks, highlighting the U.S. cost advantage.)

Capital Markets Respond: A Swift Revaluation

The capital markets have responded with remarkable speed to these shifting fundamentals. Energy sector Mergers and Acquisitions (M&A) activity surged, totaling nearly $142 billion in the twelve months concluding November 2025, a substantial increase from under $28 billion in the preceding year. Deal multiples have expanded sharply, with recent private market transactions for natural gas power assets clearing at enterprise value to EBITDA (EV/EBITDA) multiples of 7-8x or higher. A landmark transaction in this trend was Constellation’s acquisition of Calpine for $26.6 billion, representing the largest private power transaction in U.S. history.

Despite this robust M&A activity and increasing valuations, the current market prices for operating natural gas power plants remain below their replacement costs. The cost of constructing new greenfield CCGT facilities is estimated to range from $2,200 to $3,000 per kilowatt. In contrast, operating brownfield assets are currently trading in the market at significantly lower multiples, typically between $700 and $1,350 per kilowatt. This valuation discount provides a meaningful margin of safety for investors and reflects a hard structural reality: the rapid deployment of new natural gas generation capacity faces significant hurdles. These include extensive interconnection backlogs with grid operators, permitting timelines that can stretch for years, and substantial queues for gas turbine deliveries, with some extending as far out as 2030.

Chart 5: U.S. Power Sector Trends

(Visual representation of key trends impacting the U.S. power sector, potentially including capacity additions, M&A activity, and cost trends.)

Navigating Risk: Brownfield Acquisitions vs. Greenfield Development

For investors seeking exposure to the natural gas power sector, the choice between acquiring existing operating plants (brownfield) and developing new facilities (greenfield) presents distinct risk profiles and reward potentials.

Brownfield acquisitions are currently dominating deal activity for several compelling reasons. Operating plants immediately generate cash flows from day one, possess established grid connections, and have operational histories that facilitate rigorous underwriting and due diligence. While future power prices and potential regulatory changes represent inherent uncertainties, these risks are generally considered analytically forecastable.

Greenfield development, on the other hand, is a more complex undertaking. The multi-year processes for obtaining permits, the protracted interconnection queues, and the scarcity of critical equipment like gas turbines significantly compound execution risk. However, this development pathway can become more attractive when developers can secure long-term contracts for capacity before commencing construction. A particularly promising opportunity in this vein is the development of data center co-location facilities. In this model, new generation capacity is built adjacent to a hyperscaler’s data center and contracted directly to provide dedicated, behind-the-meter power, offering a high degree of revenue certainty.

The Opportunity: A "Thermal Renaissance"

For institutional allocators and infrastructure investors, the current market environment presents a significant opportunity within a large and liquid sector. The natural gas power market is offering a range of risk profiles and is undergoing a real-time repricing of assets. The fundamental question is no longer whether natural gas generation is attractive in principle, as its supply, demand, and pricing fundamentals appear to be robust and durable. The U.S. natural gas generation sector has indeed transitioned from a period of boom, through a challenging bust, and is now experiencing a remarkable resurgence. This phenomenon can be aptly termed a "Thermal Renaissance."

Learn more about CAIA Association and how to become part of a professional network that is shaping the future of investing, by visiting https://caia.org/