The global transition toward a sustainable economy has entered a volatile new phase characterized by intense geopolitical competition, defensive trade postures, and a systemic shift away from the era of unfettered globalization. As nations race to secure their positions in the burgeoning green economy, a wave of protectionism is fundamentally altering the flow of clean technologies. Governments are increasingly prioritizing the development of homegrown manufacturing hubs and the diversification of supply chains over the traditional pursuit of low-cost, cross-border efficiency. This shift is manifesting in a surge of trade restrictions, including targeted export controls, heightened tariffs on essential products like solar panels and electric vehicles (EVs), and the exclusion of clean technologies from new free trade agreements. The result is the emergence of "walled markets" that, while intended to bolster domestic resilience, risk slowing the global deployment of the very technologies required to meet urgent climate targets.

The Surge in Trade Interventions and Policy Shifts

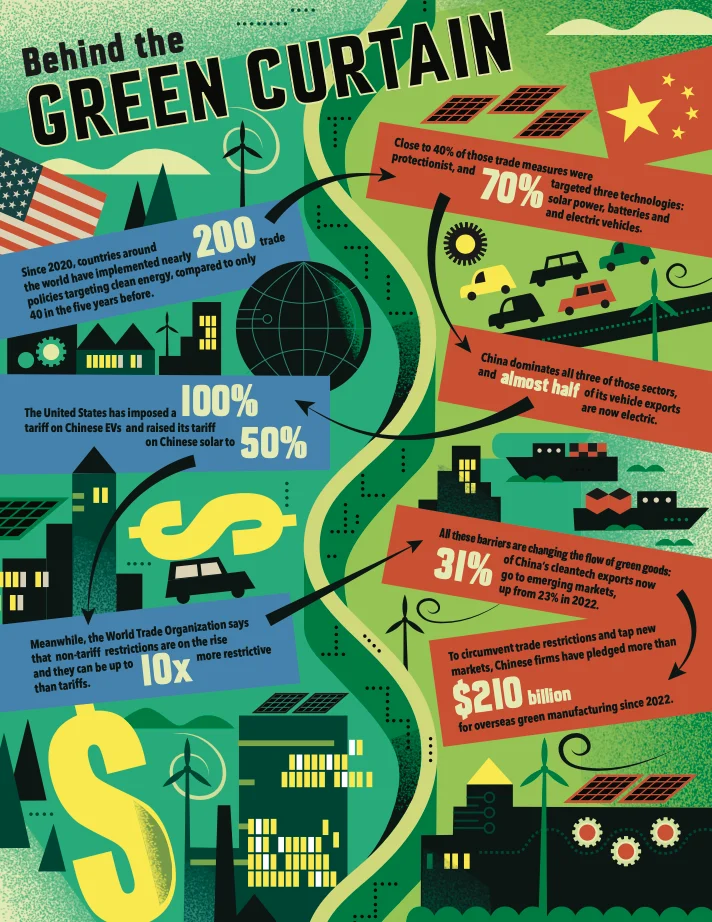

The scale of the shift toward protectionism is reflected in recent trade data. Since 2020, countries across the globe have implemented nearly 200 trade policies specifically targeting the clean energy sector. This represents a staggering increase compared to the five-year period between 2015 and 2019, during which only 40 such measures were recorded. This fivefold increase underscores a pivot from environmental cooperation to industrial competition. According to data from the Net Zero Policy Lab and the International Energy Agency (IEA), approximately 40% of these new measures are explicitly protectionist in nature, designed to shield domestic industries from foreign competition rather than merely regulating safety or environmental standards.

The focus of these interventions is highly concentrated. Roughly 70% of the trade measures implemented since 2020 have targeted three critical "pillar" technologies: solar photovoltaics (PV), lithium-ion batteries, and electric vehicles. These sectors are viewed by major economies not just as tools for decarbonization, but as the primary engines of industrial growth for the 21st century. Consequently, the competition to control these supply chains has become a matter of national economic security.

A Chronology of Green Trade Friction

The path to the current state of green protectionism can be traced through a series of escalating policy decisions and geopolitical shifts over the last decade.

2012–2018: The Early Solar Skirmishes

The roots of the current friction lie in the early 2010s, when the United States and the European Union first imposed anti-dumping and anti-subsidy duties on Chinese solar panels. These initial measures were a response to the rapid expansion of China’s solar manufacturing capacity, which led to a global glut of low-cost panels that threatened Western manufacturers.

2020–2021: Supply Chain Vulnerabilities Exposed

The COVID-19 pandemic served as a catalyst for the current protectionist trend. Global lockdowns exposed the extreme fragility of concentrated supply chains, particularly those reliant on a single geographic source. This realization prompted a strategic shift toward "near-shoring" and "friend-shoring," as nations began to view the concentration of clean tech manufacturing in China as a strategic risk.

2022: The Turning Point of the Inflation Reduction Act

The passage of the Inflation Reduction Act (IRA) in the United States marked a definitive move toward industrial policy. By offering massive subsidies for domestic clean energy production and implementing "local content" requirements for consumer tax credits, the U.S. effectively incentivized the relocation of supply chains to North America. This prompted concerns from allies and rivals alike, triggering a global "subsidy race."

2023–2024: The Era of High Tariffs and Anti-Subsidy Probes

Following the IRA, the European Union launched its own Green Deal Industrial Plan and initiated an anti-subsidy investigation into Chinese electric vehicles. By mid-2024, the United States escalated tensions further by imposing a 100% tariff on Chinese EVs and raising tariffs on Chinese solar cells to 50%. These moves were aimed at preventing a "second China shock," where a flood of subsidized Chinese exports would theoretically stifle the development of Western green industries.

2025–2026: The Consolidation of Walled Markets

By the spring of 2026, the global trade landscape has solidified into distinct blocs. Trade in clean technology is no longer governed primarily by price but by geopolitical alignment and domestic industrial mandates.

The Dominance of China and the American Response

At the heart of this trade conflict is China’s overwhelming lead in clean technology manufacturing. Through decades of state-led investment and industrial planning, China has secured a dominant position in the "New Three" industries: solar, batteries, and EVs. Today, almost half of China’s total vehicle exports are electric, a milestone that has alarmed traditional automotive powerhouses in Detroit, Stuttgart, and Tokyo.

The United States has adopted the most aggressive defensive posture. By imposing a 100% tariff on Chinese EVs, the U.S. government has effectively barred Chinese manufacturers from entering the American market at scale. Similarly, the 50% tariff on solar components is intended to provide a price floor that allows U.S.-based factories—many of which were incentivized by the IRA—to compete despite higher labor and operational costs.

However, the World Trade Organization (WTO) has warned that tariffs are only the most visible part of the problem. Non-tariff restrictions—such as complex technical standards, burdensome licensing requirements, and strict local content rules—are on the rise. The WTO estimates that these non-tariff barriers can be up to 10 times more restrictive than traditional tariffs, creating "invisible walls" that are harder to challenge through standard trade dispute mechanisms.

The Strategic Pivot to Emerging Markets

In response to being increasingly squeezed out of North American and European markets, Chinese clean tech firms are aggressively pivoting their strategies. This shift is twofold: a redirection of exports and a massive increase in overseas direct investment.

Data indicates that 31% of China’s cleantech exports are now destined for emerging markets, up from 23% in 2022. Regions such as Southeast Asia, Latin America, and parts of the Middle East and Africa are becoming the new primary consumers of Chinese green goods. These regions, often less concerned with the geopolitical implications of Chinese dominance and more focused on the immediate need for affordable energy, are benefiting from the low-cost technologies that the West is currently rejecting.

Furthermore, Chinese firms are circumventing trade restrictions by moving production closer to their end markets. Since 2022, Chinese companies have pledged more than US$210 billion for overseas green manufacturing projects. By building battery plants in Hungary, EV assembly lines in Mexico, and solar component factories in Vietnam, Chinese industry is effectively internationalizing its footprint to maintain market access despite the protectionist walls rising in Washington and Brussels.

Analysis of Economic and Environmental Implications

The rise of green protectionism carries profound implications for both the global economy and the fight against climate change.

The Cost of the Energy Transition

The most immediate impact of protectionism is the potential for increased costs. By restricting access to the world’s lowest-cost clean technology producers, countries implementing tariffs are essentially making their own energy transitions more expensive. Higher prices for solar panels and EVs could slow the pace of adoption among consumers and utilities, potentially delaying the achievement of net-zero targets.

Industrial Revitalization vs. Economic Inefficiency

Proponents of these trade measures argue that they are necessary to ensure a "just transition" that creates high-quality domestic jobs. By building local supply chains, countries can ensure that the economic benefits of the green shift stay within their borders. However, economists warn that this could lead to significant inefficiencies. If every nation tries to build its own complete supply chain for every technology, the global economy loses the benefits of specialization and scale, leading to a fragmented market where resources are duplicated and innovation may stagnate.

The Risk of a "Green Cold War"

The current trajectory suggests a deepening of the "Green Cold War." As clean technology becomes inextricably linked to national security, the sharing of research and development may diminish. This fragmentation could hinder the technological breakthroughs needed to decarbonize hard-to-abate sectors like heavy industry and aviation.

Official Responses and Global Perspectives

The international community remains divided on how to manage these tensions. The World Trade Organization has repeatedly called for a return to multilateral cooperation, warning that a "fragmented trade system will make it impossible to solve the climate crisis." WTO Director-General Ngozi Okonjo-Iweala has emphasized that "trade is a tool for resilience," and that blocking the flow of green goods could be self-defeating for the planet.

On the other hand, the International Energy Agency (IEA) has acknowledged the legitimacy of concerns regarding supply chain concentration. IEA Executive Director Fatih Birol has noted that while trade must remain as open as possible, the world cannot rely on a single country for 80% to 90% of its critical clean tech components. The IEA advocates for "diversified manufacturing," though it cautions that this should be achieved through partnership rather than punitive trade wars.

In the United States, officials maintain that the tariffs are a necessary response to "non-market practices" and overcapacity. The U.S. Trade Representative’s office has argued that without these protections, the American green industrial base would be decimated before it has a chance to mature.

Conclusion: Navigating a Fragmented Future

The spring of 2026 finds the global green economy at a crossroads. The transition from a fossil-fuel-based system to a renewable one is no longer just an environmental imperative; it is the central theater of global economic competition. While the rise of protectionism may succeed in fostering domestic industries in the short term, the long-term consequences of "walled markets" remain uncertain.

As countries continue to navigate this new landscape, the challenge will be to balance the desire for industrial sovereignty with the global necessity for a rapid and affordable energy transition. The current shift toward 200 targeted trade policies and $210 billion in redirected investments suggests that the era of a unified global market for clean technology has, for now, come to an end. The future of the green economy will likely be defined by regional hubs, strategic alliances, and a complex web of restrictions that will test the world’s ability to cooperate in the face of a shared climate threat.