The trajectory of private infrastructure as an asset class over the past decade presents a compelling case study in the challenges of managing overwhelming success. Once a steady, reliable component of institutional portfolios, infrastructure has undergone a profound transformation, driven by a confluence of governmental funding gaps, investor demand for stable returns, and the explosive growth of new, technology-driven sub-sectors. This evolution has led to a more complex and diversified landscape, demanding a nuanced approach from investors and fund managers alike.

The Rise of Infrastructure: From Post-Crisis Necessity to Investment Darling

The origins of the modern infrastructure investment boom can be traced back to the aftermath of the 2008 Global Financial Crisis. Governments worldwide faced significant fiscal constraints, with public funds diverted to stabilizing financial institutions and managing economic fallout. Simultaneously, a growing consensus emerged regarding the deteriorating state of critical public infrastructure and the immense capital required for its modernization and expansion. Projections from institutions like Stanford, which forecasted a $2.6 trillion U.S. funding shortfall through 2029, and McKinsey, estimating global annual infrastructure needs exceeding $9 trillion, underscored the scale of the challenge.

This void in public funding created a fertile ground for private capital. From an investor’s perspective, infrastructure offered an attractive proposition. It represented tangible assets underpinning essential services – utilities, transportation networks, communication systems – that typically experience stable demand, irrespective of economic cycles. Furthermore, many infrastructure assets benefited from regulated pricing mechanisms or long-term contracts, leading to predictable, often inflation-linked cash flows. The inherent monopolistic or oligopolistic nature of many infrastructure businesses also provided significant pricing power. For investors emerging from the uncertainty of the financial crisis, infrastructure emerged as a compelling alternative, perceived as offering the stability of fixed income with the potential for equity-like returns.

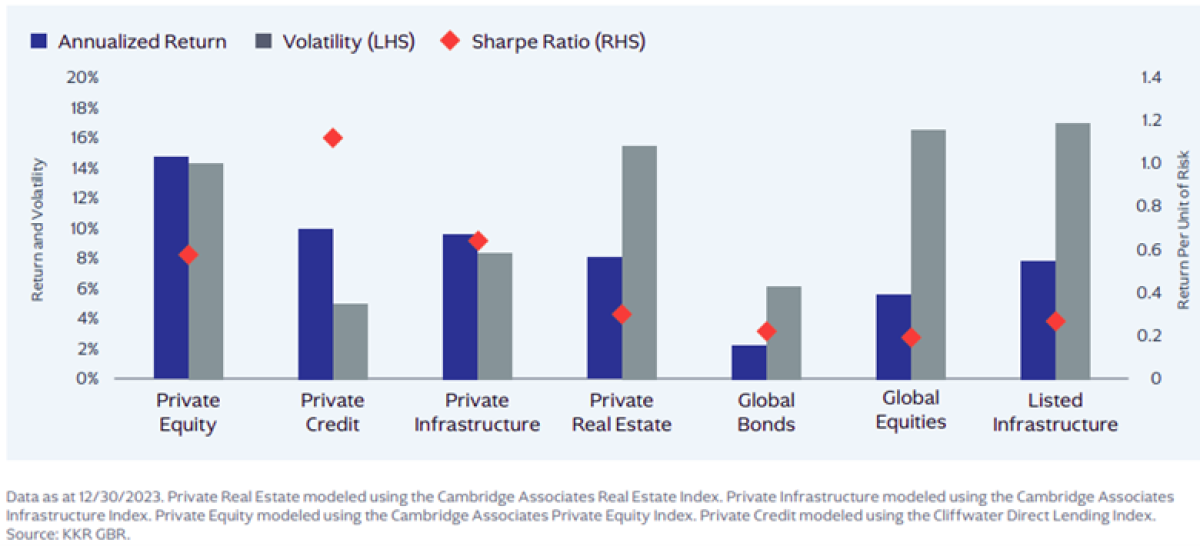

This perception proved largely accurate in the years that followed. Between 2016 and 2022, global infrastructure funds delivered average annual returns of approximately 11%. Crucially, the mark-to-market volatility of these investments often resembled that of public bonds, and their correlation with public equity markets remained within a manageable range of 0.6 to 0.8, as depicted in Figure 1. This period solidified infrastructure’s reputation as a low-volatility, high-return asset class, attracting substantial inflows of capital. The managed assets in private infrastructure funds surged from approximately $60 billion in 2008 to an estimated $1.6 trillion by 2026, representing a compound annual growth rate second only to venture capital among private asset classes.

The Growing Pains of Success: Valuations, Returns, and the Search for Yield

However, this period of unprecedented growth began to present its own set of challenges. By the early 2020s, the asset class was exhibiting signs of "suffering from success." The sheer volume of capital seeking deployment, with infrastructure funds raising a record $130 billion in 2021 alone, led to increased competition among general partners (GPs) to acquire assets. This intense demand inevitably drove up valuations.

The "boring" but stable infrastructure assets that characterized the 2010s – mature utilities, toll roads, and essential service providers – began to project lower future returns, even as their operational complexity remained significant. The readily available, low-risk, high-yield deals that had been a hallmark of the asset class started to disappear. Investors were increasingly faced with a stark choice: accept lower projected returns from established, core assets, or venture further out the risk curve into opportunities that began to resemble the higher-risk, higher-reward profile of private equity. This inflection point marked a departure from the original investment thesis for many.

The Expanding Definition of Infrastructure: Beyond Roads and Bridges

A key driver of this evolution has been the dramatic expansion of what constitutes "infrastructure." Historically, the term was synonymous with long-lived, physical assets such as toll roads, airports, utilities, and schools, characterized by stable demand and predictable cash flows secured through regulatory frameworks or concessions. While undeniably essential, these traditional assets no longer solely define the landscape.

Over the past 15 years, the definition has broadened considerably, and it is within these expanded definitions that much of the new capital has been deployed.

Digital Infrastructure: The New Essential Utility

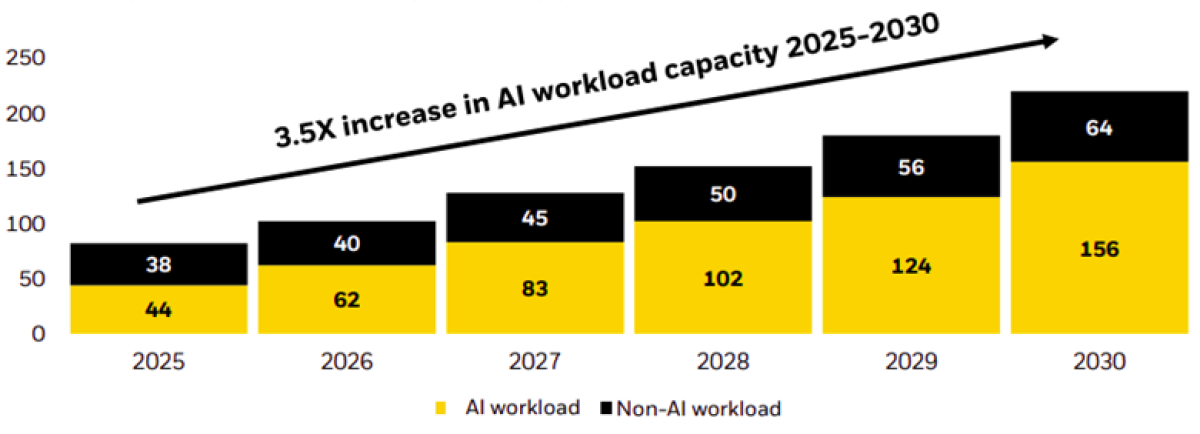

Perhaps the most striking example of this expansion is digital infrastructure. Telecom towers, fiber optic networks, data centers, and 5G infrastructure, once considered niche or technology-driven projects, are now increasingly viewed as the new utilities of the 21st century. The exponential growth in data consumption, fueled by the rise of cloud computing and the burgeoning adoption of artificial intelligence, has rendered digital connectivity as critical as water or power.

This surge in demand has created inelasticity in the market for digital infrastructure assets. Many now feature long-term contracts with creditworthy counterparties, and their cash flow profiles are becoming increasingly predictable. Assets like telecom towers and fiber networks have transitioned from "core-plus" to "core" or even "super-core" status as their revenue streams have stabilized. Projections from McKinsey indicate that global data center capacity could nearly quadruple by 2030, underscoring the immense growth potential in this sector (Figure 2). This expansion could have profound macroeconomic implications, akin to the productivity gains unlocked by the U.S. interstate highway system in the mid-20th century, which contributed an estimated 25% of American productivity gains between 1950 and 1989.

Renewable Energy and Clean Power: A Climate Imperative

Renewable energy and clean power generation have also become central to infrastructure portfolios. A decade ago, this sector was nascent, heavily reliant on subsidies, and bore a resemblance to venture capital investments. Today, it is a critical pillar of global efforts to "climate-proof" economies. In many regions, clean energy has transitioned from subsidy dependence to market competitiveness. The scale of investment required for the energy transition is staggering, with estimates suggesting around $9 trillion annually in physical assets will be needed by 2050.

This imperative has spurred the creation of dedicated energy transition funds and a significant increase in capital allocation towards higher-risk greenfield projects. Investments in offshore wind farms, battery storage solutions, and grid modernization initiatives are crucial components of this transition, addressing areas where governments alone are unable or unwilling to provide the necessary funding.

Conventional Energy and Utilities: Navigating Transition Risks

The landscape for conventional energy and utilities presents a more complex narrative. Natural gas pipelines and fossil-fuel power plants, once considered stable, low-risk cash cows, now face significant transition risks as economies shift towards cleaner energy sources. Assets like gas distribution networks, traditionally categorized as "super-core," may require costly repurposing or eventual decommissioning, pushing them into a higher-risk profile. These traditional assets necessitate a re-evaluation of their long-term viability and risk-return expectations.

Transportation and Logistics: The Backbone Needs Reinforcement

Transportation and logistics assets, including toll roads, airports, and seaports, remain fundamental components of infrastructure portfolios. However, these sectors face substantial ongoing maintenance and repair requirements. Data from BlackRock highlights the scale of this need: U.S. bridges require nearly $375 billion in repairs over the next decade, approximately half of Japan’s roads and tunnels are nearing 50 years of age, and nearly 20% of England’s water supply is lost due to leaks. These figures represent significant opportunities for brownfield upgrades and reinvestment, essential for maintaining the operational functionality of the economy’s traditional backbone.

This expanded definition of infrastructure now encompasses a spectrum from ultra-stable, regulated utilities to high-growth greenfield renewable projects and innovation-supporting digital connectivity. Consequently, investors must now approach infrastructure with the same analytical rigor applied to equity markets, looking beyond the broad label to understand sector-specific dynamics and risk differentiation.

The Political Variable: A New Driver of Infrastructure Returns

The performance dispersion across different infrastructure strategies has become increasingly pronounced. Cambridge Associates data indicates that while diversified infrastructure funds have delivered median returns below 10%, digital infrastructure funds have achieved approximately 14% (Figure 3). More significantly, the distribution of returns reveals insights into geopolitical risk. Digital infrastructure often exhibits extreme positive skew, akin to venture capital, suggesting high upside potential but also significant risk. Renewables and power, conversely, tend to show left-skewed distributions, indicating a greater potential for downside.

The "political will variable" plays a crucial role in shaping these return distributions. Governments’ willingness and ability to support infrastructure development and maintenance can significantly influence outcomes. Extreme left skews can arise when governmental intervention becomes overly burdensome, leading to delays or regulatory uncertainty, particularly in politically fractious environments. This is most evident in traditional utilities and energy assets operating within such contexts. For instance, a clear and consistent infrastructure agenda from a national government, such as Germany’s, can act as a powerful enabler, whereas fragmented decision-making processes, as seen in the United States, can present significant constraints.

In this evolving landscape, infrastructure has transcended its original role as a mere fixed-income replacement. It now serves as a growth allocation and, increasingly, as a bet on governmental ambition and stability. The political environment is no longer a secondary consideration but a primary driver of which infrastructure assets will deliver strong returns and which may falter.

Synthesis: A New Era of Infrastructure Investing

The journey of private infrastructure from a post-crisis necessity to a highly sought-after asset class underscores a critical paradox: success has brought complexity. The original mandate to bridge the government funding gap and provide investors with income and stability has necessitated a dramatic expansion of the asset class. This expansion has created a dual nature: it still offers the predictable cash flows and stability that investors initially sought, but it also incorporates the inherent complexity and risk profiles previously associated with private equity.

Furthermore, the interplay of geopolitical competition and rapid technological transformation means that investing in infrastructure today is not merely about acquiring physical assets. It involves making a sophisticated assessment of which governments possess the foresight, stability, and political will to foster and support these critical investments. Investors must now navigate this intricate web of economic, technological, and political factors to effectively harness the opportunities within the dynamic infrastructure landscape. The ability to adapt to this evolving definition and risk profile will be paramount for long-term success in this crucial asset class.