The collective assets under management for the 17 largest U.S. university endowments have experienced a remarkable surge, growing from approximately $249 billion in Fiscal Year 2016 to an estimated $426 billion by FY2025. This represents a substantial increase of roughly 70-73%, a growth fueled by a combination of robust investment performance and significant new gift contributions. However, a closer examination of these institutional titans reveals a more nuanced story, characterized by distinct allocation philosophies, varied risk profiles, and a notable efficiency gap when benchmarked against global institutional peers. This analysis, drawing on the comprehensive 2025 NACUBO-Commonfund Study of Endowments, individual fund annual reports, and advanced multi-factor statistical risk modeling from FIS-APT, aims to illuminate what the investment strategies of these top endowments reveal about asset allocation, risk management, and overall portfolio efficiency in the current financial landscape.

A Decade of Growth: Strong Returns but Divergent Long-Term Leaders

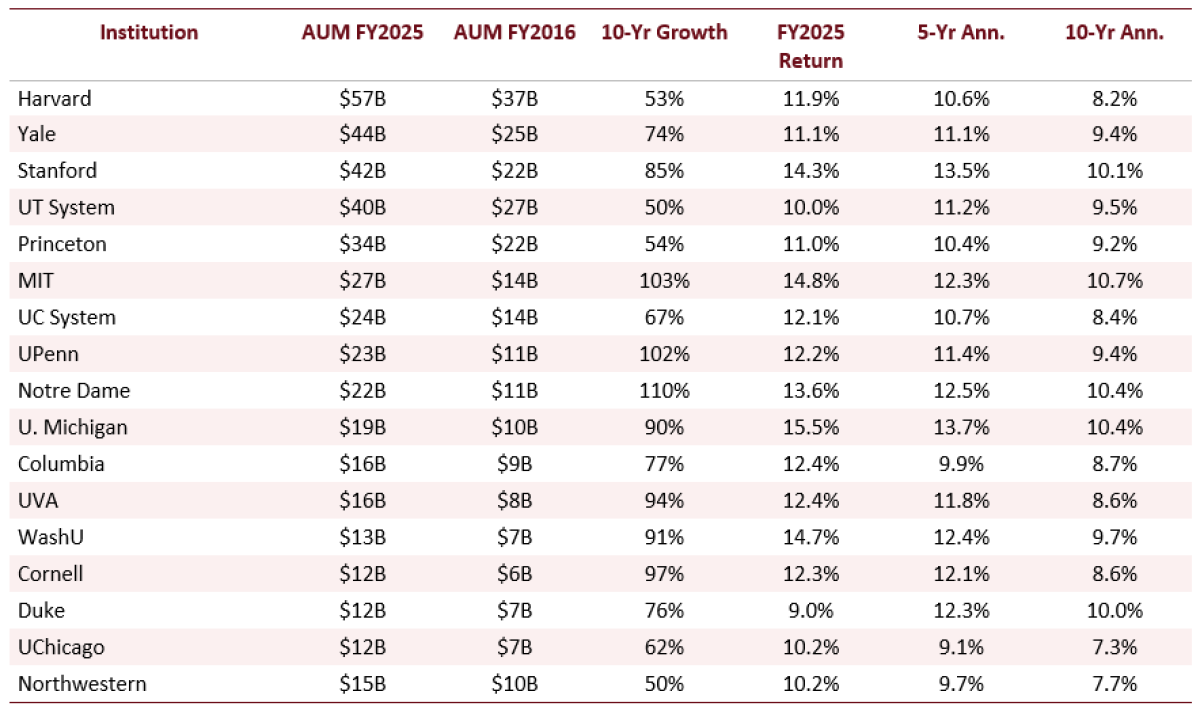

Over the past decade, the aggregate Assets Under Management (AUM) for the top 17 U.S. university endowments has demonstrated impressive growth, increasing from roughly $247 billion in FY2016 to approximately $426 billion by FY2025. This expansion, averaging an annual growth rate of approximately 6.5-7.0%, is a testament to both the power of compounding investment returns and the continued generosity of donors.

Examining individual institutional performance, the fiscal year 2025 saw several endowments achieve particularly strong one-year returns. The University of Michigan led the pack with an impressive net return of 15.5%. Close behind were the Massachusetts Institute of Technology (MIT) at 14.8%, Washington University in St. Louis (WashU) at 14.7%, and Stanford University at 14.3%.

Looking at performance over longer horizons, the picture becomes more varied, highlighting that exceptional short-term gains do not always translate into sustained long-term leadership. Over a five-year period, Michigan, Stanford, the University of Notre Dame, WashU, and MIT have all consistently exceeded 12% annualized returns. The ten-year outlook reveals a similar set of top performers, with MIT, Michigan, Stanford, Notre Dame, and Duke University leading the pack. Notably, Harvard University, despite holding the largest AUM at $57 billion, posted a ten-year annualized return of 8.2%, the lowest among the top five institutions by asset size. This suggests that while scale offers advantages, it does not inherently guarantee superior long-term investment outcomes, and that the best one-year performers are not always the strongest long-term compounders.

Table 1: AUM Growth and Net Returns: Top 17 Endowments (FY2016-FY2025)

(Image of Table 1 would be inserted here, showing AUM and Net Returns for each of the 17 endowments from FY2016 to FY2025)

Note: Source: 2025 NACUBO-Commonfund Study of Endowments; individual endowment annual reports. Returns are net of investment management fees and exclude distributions and operating expenses. AUM growth reflects investment returns and net new gifts. Some figures estimated where not publicly disclosed.

Three Distinct Philosophies: Unpacking Endowment Allocation Strategies

The strategies employed by the largest university endowments are not monolithic. A review of their asset allocations reveals three primary philosophical approaches that illustrate the diverse paths to managing substantial capital. By examining Harvard, Yale, and Michigan, we can gain insight into the spectrum of investment decision-making within this elite group.

Harvard University: The Concentration Model

Harvard’s endowment, the largest among the group at $57 billion, exemplifies a strategy characterized by significant concentration in private equity and hedge funds. With approximately 41% allocated to private equity and 31% to hedge funds, and no dedicated allocation to venture capital, Harvard embraces substantial illiquidity and manager concentration. This approach aims to capture the premium returns associated with private markets. While Harvard has demonstrated strong recent one-year performance at 11.9%, its ten-year return of 8.2% reflects the cost of earlier portfolio adjustments and the inherent challenges of managing such a concentrated, illiquid portfolio.

Yale University: The Diversified Alternatives Model

Yale University stands as the progenitor of the diversified alternatives model, a framework that has profoundly influenced the industry’s approach to endowment portfolio construction. Its allocation strategy reflects this pioneering spirit, with 24% in venture capital, 20% in private equity, and 22% in hedge funds. This broad diversification across alternative asset classes aims to mitigate risk while seeking enhanced returns. Yale’s consistent performance, with an 11.1% one-year return and a 9.4% ten-year annualized return, underscores the enduring strength of its disciplined diversification strategy, which compounds effectively over extended periods.

University of Michigan: The Growth-Concentrated Model

The University of Michigan, the top performer in FY2025 with a 15.5% net return, showcases a growth-concentrated model. Its portfolio features a significant allocation to venture capital (33%) and private equity (11%), complemented by allocations to hedge funds and real assets (13% each). This strategic posture, which has resulted in a robust 13.7% five-year and 10.4% ten-year annualized return, suggests a durable strategic approach that has been built and refined across multiple market cycles, rather than a single-year outcome driven by temporary market conditions, such as the recent surge in AI-related valuations.

Table 2: Three Endowment Case Studies: Harvard, Yale, and Michigan (FY2025 Standardized Allocation Categories)

(Image of Table 2 would be inserted here, showing the allocation percentages for Harvard, Yale, and Michigan across various asset classes)

Note: Source: FY2025 institutional reports and APT/UMass standardized allocation mapping. Categories are presented in comparable asset-class buckets and may differ from each institution’s exact public-report labels. Rows may not sum to 100% due to rounding and category mapping.

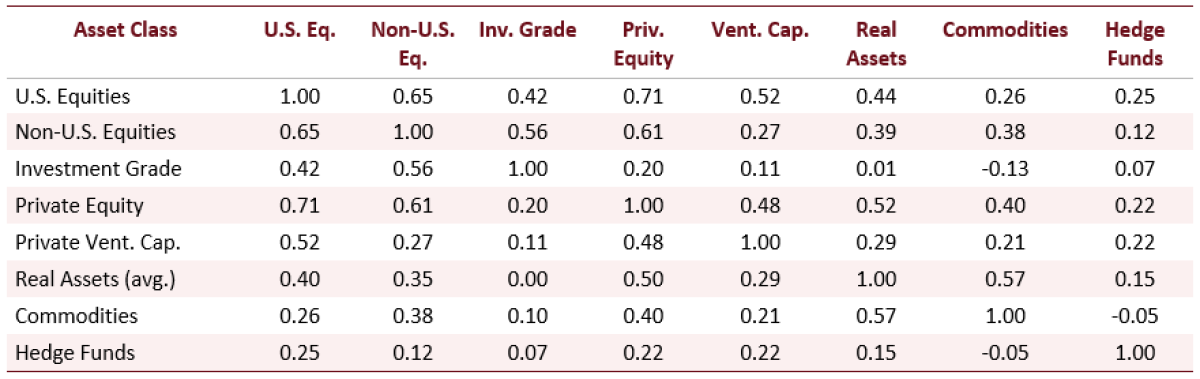

Diversification Nuances: Real Assets and Hedge Funds as Risk Mitigators

While the trend towards alternative investments has been a hallmark of endowment strategy, the efficacy of diversification is not uniform across all asset classes. Analysis of ex-ante correlation estimates from the FIS-APT model reveals important distinctions, particularly between private equity and hedge funds, offering critical insights for investment professionals.

Table 3: Selected APT Correlation Estimates Across Asset Classes (APT Model)

(Image of Table 3 would be inserted here, showing correlation estimates between various asset classes)

Note: Source: APT model, UMass Amherst Endowment Research Project (2026). Real Assets is an approximate composite based on several real asset sub-categories, so pairwise values should be interpreted as selected model estimates rather than a mathematically complete symmetric correlation matrix. Full model correlation output is available in the underlying workbook.

The data indicates that private equity exhibits a correlation of 0.71 with U.S. equities, and venture capital shows a correlation of 0.52. These figures suggest that both asset classes retain a significant exposure to equity beta. Similarly, real estate and private energy investments carry comparable equity-like exposures.

In contrast, hedge funds, as modeled by the Global HFR Index, demonstrate a much lower correlation with U.S. equities (0.25) and non-U.S. equities (0.12). Commodities, an asset class often considered a hedge against inflation, show a negative correlation of -0.05 with hedge funds. This divergence is crucial: even with allocations exceeding 60% in alternatives, a substantial 86% of the ex-ante volatility across large endowments still originates from the equity factor. This implies that endowments have not eliminated equity risk but rather have shifted its manifestation towards manager selection, timing of valuations, and the acceptance of illiquidity.

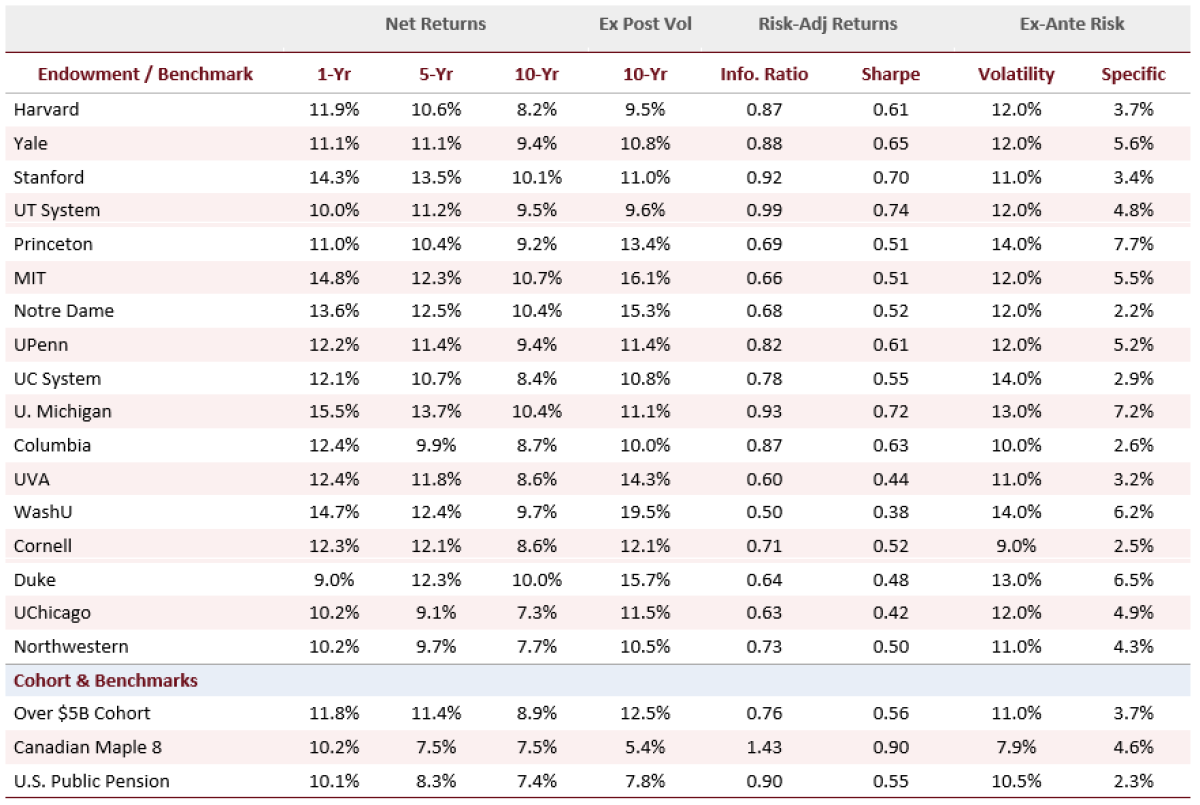

Risk Profile: Balancing Higher Returns with Risk-Adjusted Efficiency

The pursuit of higher returns often comes with an elevated risk profile. The analysis of the top 17 endowments reveals that while they generally outperform their U.S. and Canadian pension fund peers over one, five, and ten-year horizons—with the "Over $5B" cohort achieving returns of 12%, 11%, and 9% respectively—this outperformance is associated with higher ex-ante risk (approximately 11%) and a greater potential for losses. Specifically, these endowments face approximately a 20% potential loss in a 1-in-20-year event.

Consequently, their risk-adjusted returns, as measured by the Sharpe Ratio and Information Ratio, lag behind those of more conservative benchmarks. The "Over $5B" cohort reports Sharpe Ratios of 0.56 and Information Ratios of 0.76, significantly lower than the Canadian Maple 8 benchmark, which achieves ratios of 0.90 and 1.43, respectively.

Table 4: Ex-Ante Risk, Net Returns, and Risk-Adjusted Performance by Endowment Plan (APT Model Output)

(Image of Table 4 would be inserted here, showing risk metrics and performance data for endowments and benchmarks)

Note: Source: APT model output, UMass Amherst Endowment Research Project (2026). Net returns are from 2025 NACUBO-Commonfund Study and individual annual reports. Ex post volatility is 10-year realized. Sharpe Ratio uses the workbook’s 3.1% risk-free rate. Information Ratio is reported directly from the APT workbook. Ex-ante volatility and systematic/specific risk from the TLA_ST tab.

The Sharpe ratio range among the 17 endowments spans from 0.38 (WashU) to 0.74 (UT System). In comparison, the Canadian Maple 8 benchmark achieves a Sharpe ratio of 0.90. WashU’s ten-year ex-post volatility of 19.5% is the highest in the group, which, despite a competitive 9.7% ten-year return, results in a lower Sharpe ratio. Conversely, Cornell and Columbia Universities exhibit the lowest ex-ante volatility within the individual endowment group (9.1% and 9.6%, respectively) and achieve above-average Sharpe ratios relative to peers with higher headline returns. The Maple 8’s Information Ratio of 1.43, compared to the "Over $5B" cohort’s 0.76, serves as a stark indicator of the efficiency gap. This suggests that while U.S. endowments are growing their assets, they are not necessarily doing so as efficiently on a risk-adjusted basis when compared to certain sophisticated global institutional investors.

Stress Tests: The Persistent Dominance of Equity Risk

Even with significant allocations to alternative investments, the impact of equity market movements remains a dominant factor in portfolio performance, particularly during periods of market stress. An analysis of factor attribution reveals that 86% of the ex-ante volatility across large endowments is attributable to equity factor risk, a factor that significantly influences losses during severe market downturns.

In a simulated COVID-19 scenario (March-April 2020), most endowments experienced losses ranging from 21% to 27%, underscoring the pervasive impact of equity beta during rapid global liquidity events. However, in a simulated early 2022 inflationary environment, endowments fared comparatively better than their pension fund counterparts. The "Over $5B" cohort lost approximately 8%, while benchmark portfolios saw losses between 22% and 25%. This resilience is attributed to the partial inflation hedging provided by real assets and hedge fund exposures.

Table 5: Potential Losses and Factor Risk Attribution by Endowment Plan (APT Model Output)

(Image of Table 5 would be inserted here, showing stress test results and factor attribution)

Note: Source: APT model output, UMass Amherst Endowment Research Project (2026). VaR and Average Loss are 1-in-20-year annual loss estimates. Max Drawdown Horizon is 20 days. Factor attribution percentages are selected model factors and may not sum to 100% because Currencies and Other factor exposures are omitted for space. Stress test losses are scenario-based estimates: Financial Crisis (June-December 2008), COVID (March-April 2020), Stagflation (January-October 2022).

Several findings from these stress tests are particularly noteworthy:

- Notre Dame’s Equity Sensitivity: Notre Dame exhibits a striking 96% equity factor attribution, leading to a significant stagflation loss of -18.1%. This reflects its pronounced reliance on public equities within its investment strategy.

- Duke’s Inflation Hedge: Duke’s portfolio benefits from an 11.7% commodities factor share, the highest among its peers. This exposure contributed to a comparatively smaller stagflation loss of -4.3%, demonstrating the effectiveness of real assets and natural resources in hedging against inflation.

- Maple 8’s Fixed Income Exposure: The Canadian Maple 8 benchmark’s 7.0% duration factor attribution, in contrast to the minimal exposure ( -0.1% to 0.3%) for most endowments, highlights its greater allocation to fixed income. While this strategy resulted in a larger stagflation loss (-10.0%) due to rising interest rates, it also contributed to its lower overall volatility profile.

- Systemic Losses in Stagflation: The University of California System and Notre Dame recorded the most substantial stagflation losses (-15.7% and -18.1%, respectively), driven by their high equity factor concentrations. The U.S. Public Pension benchmark also experienced a significant stagflation loss (-18.8%), attributable to its mandatory fixed income allocation, which incurs mark-to-market losses during sharp rate increases. The COVID scenario showed less dispersion, with most portfolios experiencing similar losses, confirming the widespread impact of equity beta.

Key Takeaways for Investment Professionals

The performance and risk profiles of the largest U.S. university endowments offer several critical insights for investment professionals navigating complex market environments:

-

Volatility Adjustment is Crucial for Performance Comparison: Headline returns alone can be misleading. For instance, WashU’s 9.7% ten-year return and Cornell’s 8.6% ten-year return appear comparable in isolation. However, WashU’s ex-ante volatility of 14.1% versus Cornell’s 9.1% reveals a significant difference in risk-taking. Cornell’s more disciplined approach yields a more efficient outcome for the risk assumed, as evidenced by its superior Sharpe ratio. Table 4 provides a comprehensive comparison of risk-adjusted performance across all 17 institutions.

-

Factor Attribution Trumps Allocation Labels in Stress Testing: Understanding how portfolio components behave under stress is paramount. Institutions with similar broad alternative asset allocations can exhibit vastly different equity factor exposures. This equity factor exposure is the primary determinant of losses during significant market events like the Financial Crisis and the COVID-19 pandemic. Differentiated outcomes in stagflation scenarios, such as those observed in 2022, are often driven by specific exposures to real assets, commodities (particularly energy and natural resources), and infrastructure.

-

The Maple 8 Approach: Structural Differences in Diversification: The divergence in strategies between U.S. endowments and benchmarks like the Maple 8 highlights fundamental differences in portfolio construction. U.S. endowments primarily utilize real assets and hedge funds to de-correlate from equity markets. In contrast, the Maple 8 employs leverage—derived from debt, repurchase agreements, and derivatives markets—to diversify exposures, notably through fixed income. Both approaches enhance risk-adjusted returns compared to traditional portfolios but achieve this through distinct mechanisms with differing risk profiles. The Maple 8’s superior Sharpe and Information Ratios suggest that closing this efficiency gap would necessitate U.S. endowments embracing balance sheet leverage and direct investment in infrastructure, elements that may face governance challenges within current institutional frameworks.

The decade-long trajectory of these large endowments underscores a dynamic interplay between ambitious growth objectives, evolving allocation strategies, and the persistent realities of market risk. While diversification into alternatives has become a cornerstone, a deeper understanding of factor exposures and risk-adjusted efficiency remains critical for optimizing long-term financial stewardship.