Chief Executive’s latest poll reveals a slight uptick in CEO confidence regarding current business conditions, a trend that has persisted for four consecutive months. However, this cautious optimism is tempered by significant divergence in outlooks for the year ahead, primarily driven by persistent geopolitical instability, elevated inflation, and policy uncertainty. While leaders perceive a more stable present, their expectations for the future remain a complex tapestry of competing forces.

A Cautious Advance: Navigating Present Realities

The June reading of Chief Executive’s CEO Confidence Index indicates a modest improvement, with business leaders reporting a more favorable view of the current economic landscape. The index, measuring CEO sentiment on a scale of 1 to 10, saw its rating of current business conditions rise by approximately 2 percent, reaching 5.7 from 5.6 in May. This marks the fourth consecutive month of gradual improvement, suggesting a stabilization after what was characterized as the worst year for CEO confidence since 2012.

Despite this positive momentum, overall confidence levels remain subdued when compared to historical benchmarks from previous years. The report cautions that without sustained improvement, 2026 could potentially emerge as the second-worst year for CEO confidence in the past decade. This dichotomy highlights the delicate balance between acknowledging immediate improvements and grappling with the persistent headwinds that cloud future projections.

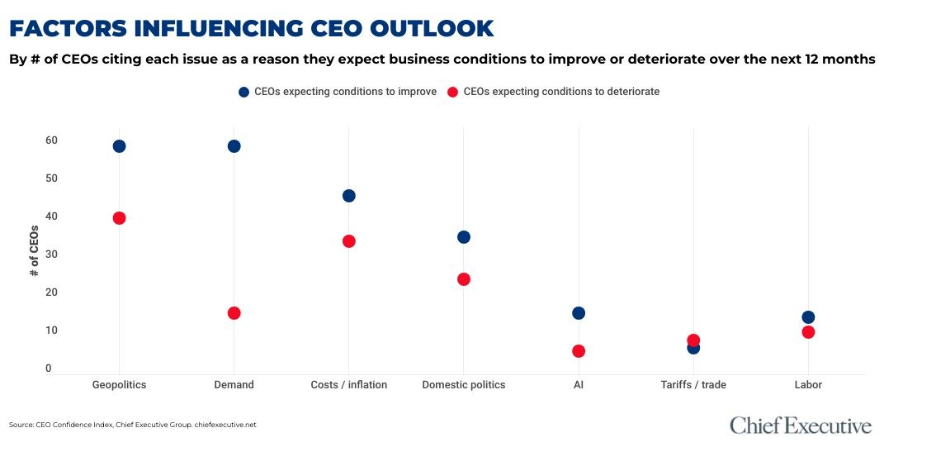

The survey, which polled 315 CEOs between June 2nd and 3rd, identified geopolitics as the most significant factor influencing their perspectives, cited by 42 percent of respondents. This was closely followed by demand, sales, and backlog, mentioned by 40 percent. These intertwined themes underscore the interconnectedness of global events and their direct impact on corporate operations and strategic planning.

Divergent Futures: Optimism Meets Apprehension

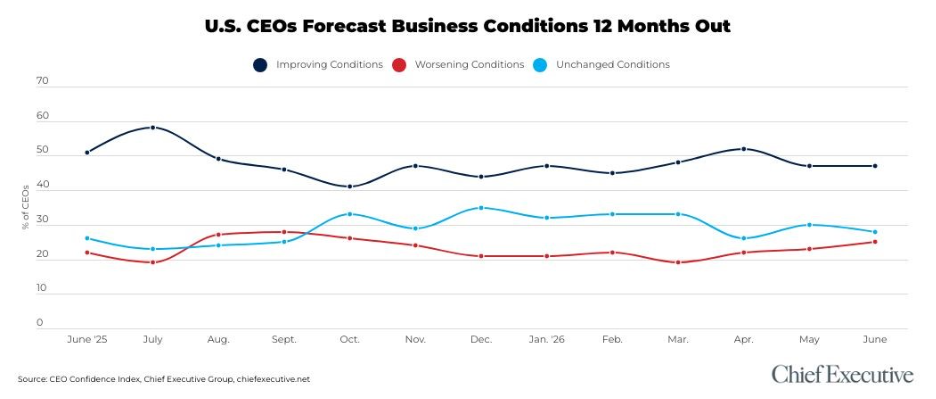

While current conditions are viewed with a slightly more favorable lens, the outlook for the year ahead remains a point of considerable division among business leaders. The forward-looking indicator of the CEO Confidence Index has shown little change since May, suggesting that the underlying anxieties and hopes are largely static. CEOs anticipate business conditions to register at 6.1 by this time next year, a marginal increase from 6.0 in May, representing a 7 percent improvement from current levels.

This modest projected growth is underpinned by a spectrum of expectations. Nearly half (47 percent) of the polled CEOs foresee an improvement in conditions in the coming months. For some, this optimism is fueled by the expectation that delayed demand will rebound once greater clarity emerges on critical issues such as ongoing conflicts, trade tariffs, interest rate trajectories, and evolving government policies. Others point to factors such as the successful launch of new products, the strategic advantage of onshoring manufacturing, the robustness of existing backlogs, and pent-up consumer demand as drivers of future growth.

Steven A. Schneider, CEO and executive chair of SHS Group Holdings, expressed a common sentiment of cautious optimism, stating, "One year from now, things should be more stabilized, and business will have a clear picture going forward." This view is echoed by Jason Stanczyk, president and CEO of EDCO, a family-owned manufacturer that has benefited from its commitment to U.S.-based operations. Stanczyk reported, "Orders are up over 12 months ago. And the industries we serve are predicting growth over the next 24 months." This suggests a segment of the business community is finding avenues for expansion despite broader uncertainties.

Conversely, a significant portion of CEOs anticipate a deterioration in business conditions, viewing the same global landscape through a more somber lens. These leaders frequently link geopolitical events, trade policies, and broader economic uncertainty to escalating operational costs. Specific concerns include rising prices for materials, flattening demand, and the inflationary impact of current policies.

"Prices for materials are up, demand is flattening, current policy is driving costs up," lamented the CEO of a family-owned manufacturing business in the Midwest, highlighting the immediate pressures on profitability. Another CEO of a PE-backed wholesale distribution company with global operations cited "Uncertainty over Iran, continued inflationary pressures on fuel, tariffs and overall cost of living" as the primary reasons behind their pessimistic outlook. These perspectives underscore the tangible impact of global volatility on corporate bottom lines and strategic decision-making.

A notable segment of CEOs, however, are forecasting a relatively flat year ahead. Twenty-eight percent of respondents anticipate a status quo scenario, a larger proportion than those expecting a negative outcome (25 percent). This group appears to be navigating the complexities by adapting to the prevailing environment. Steve Schlesinger, CEO of global research firm Sago, anticipates business conditions to remain steady at 7 out of 10 well into 2027 and forecasts the U.S. economy to be flat by the end of the year. He observed, "[It’s] not necessarily great geopolitically, but the world seems to be adjusting to it."

Peter Ensch, CEO of Sani-Matic, a manufacturer of cleaning systems for the food and beverage industry, emphasized the importance of resilience and adaptation. He noted, "Business leaders have grown accustomed to the constant chaos of the current administration." This ability to filter out noise, combined with pent-up demand, is helping to offset challenges such as rising food prices.

Economic Forecasts: A Growing Consensus on Growth, Lingering Inflationary Worries

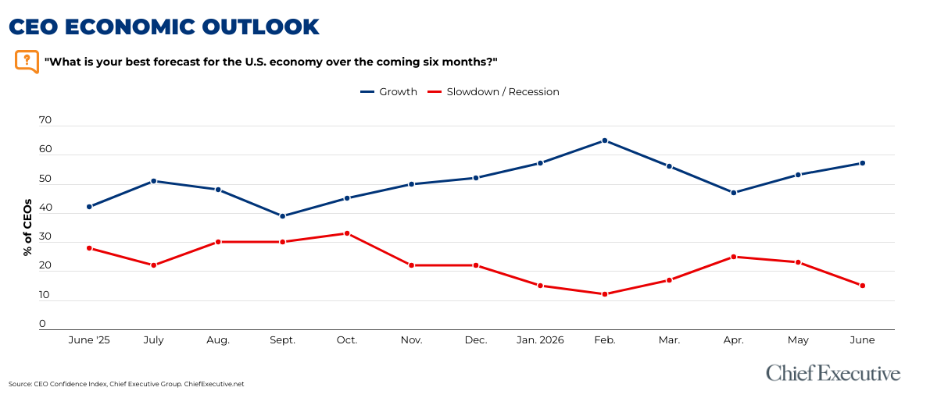

Beyond individual company outlooks, the broader economic forecast among CEOs shows a discernible shift towards growth. Fifty-seven percent of those polled in June now expect the U.S. economy to continue expanding through the end of the year. This represents an increase from 53 percent in May and marks the highest share of growth optimism recorded since February, prior to heightened geopolitical tensions.

Concurrently, the specter of recession appears to be receding in the minds of many CEOs. Only fifteen percent now anticipate a recession within the next six months, a decrease from May and the lowest level since February, when 12 percent held this view. This suggests a growing confidence in the economy’s ability to withstand immediate downturns.

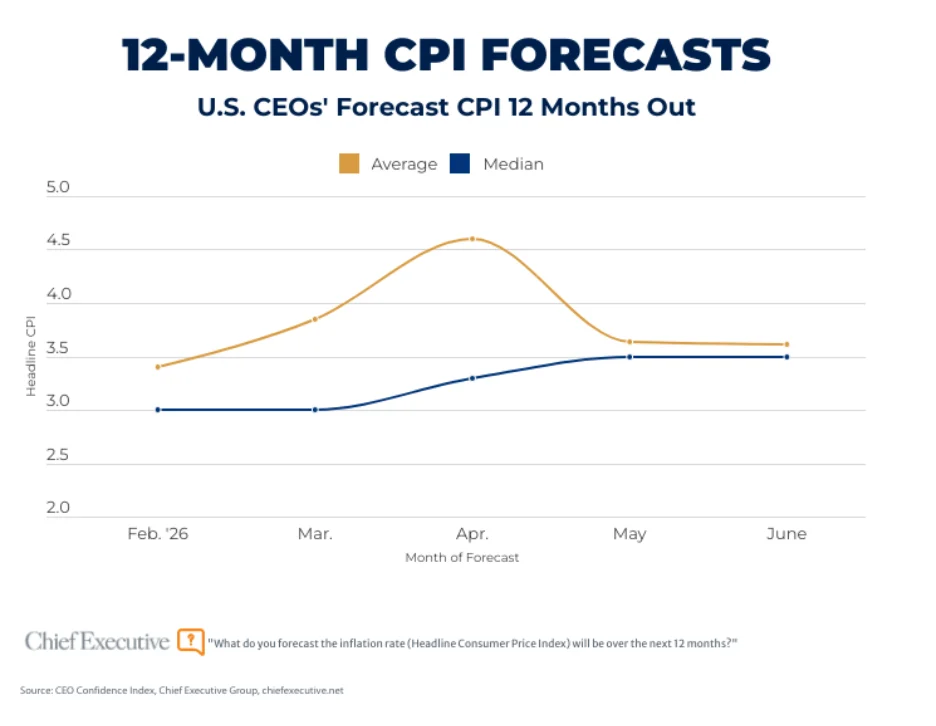

However, the persistent challenge of inflation continues to cast a long shadow. Inflation expectations remain elevated compared to earlier in the year. CEOs currently forecast headline Consumer Price Index (CPI) inflation to stand at 3.5 percent over the next 12 months, a figure that has remained unchanged from May but is up from 3.0 percent in February and March. The median forecast saw an increase in April, reaching 3.28 percent before settling at 3.5 percent in May and holding steady in June. This indicates that while economic growth is anticipated, the cost pressures associated with inflation are expected to persist, impacting both consumer spending and corporate margins.

Corporate Outlooks: Resilience in Demand and Revenue, Softening in Hiring

At the corporate level, CEO forecasts point to sustained confidence in demand, revenue growth, and productivity gains over the coming 12 months. This resilience in core business operations suggests that companies are finding ways to navigate the complex economic environment and maintain forward momentum.

However, expectations for hiring have softened. While specific figures were not detailed in the provided excerpt regarding hiring, the mention of "softened" expectations suggests a cautious approach to workforce expansion, likely influenced by the prevailing economic uncertainties and cost pressures.

Operating expenses, while still elevated, are showing some signs of easing. Seventy-three percent of CEOs anticipate an increase in operating expenses over the next 12 months, a slight decrease from the high of 77 percent recorded in April. This marginal reduction in expected expense growth could offer a small measure of relief to businesses grappling with rising costs.

The Geopolitical Crucible: Iran Conflict and its Ramifications

The persistent mention of "the war" and "uncertainty over Iran" in the context of CEO outlooks is a significant indicator of the geopolitical climate’s pervasive influence. While the specific nature of this conflict and its direct economic ties were not elaborated upon in the provided text, its consistent emergence as a primary concern highlights its substantial impact on business confidence and strategic planning.

The conflict’s implications likely extend beyond direct economic disruption, encompassing increased energy price volatility, potential impacts on global supply chains, and heightened uncertainty in international trade relations. The fact that this geopolitical factor preceded a dip in economic growth expectations in February further underscores its weight in the minds of business leaders. The current stabilization in economic growth forecasts, despite the ongoing geopolitical concerns, suggests that businesses may be adapting to a new normal of persistent international instability.

Inflationary Pressures: A Persistent Drag

The sustained elevation of inflation expectations, even as economic growth is projected, presents a complex challenge for businesses. A 3.5 percent forecast for headline CPI inflation over the next 12 months signifies a continued erosion of purchasing power for consumers and an increase in input costs for businesses. This persistent inflationary environment necessitates careful management of pricing strategies, cost controls, and investment decisions.

The median inflation forecast has been on an upward trajectory, indicating that this is not a fleeting concern but a sustained economic reality. Businesses must therefore continue to factor in the impact of inflation on their profitability and competitive positioning. The dual challenge of fostering growth while managing rising costs will likely remain a central theme for CEOs throughout the remainder of the year.

Policy Uncertainty: A Wildcard for Future Planning

The recurring theme of policy uncertainty, alongside geopolitical and inflationary concerns, adds another layer of complexity to the CEO outlook. Ambiguity surrounding government policies, whether related to fiscal stimulus, taxation, trade regulations, or monetary policy, creates a challenging environment for long-term strategic planning and investment.

When combined with geopolitical volatility and persistent inflation, policy uncertainty can lead to a more risk-averse approach among business leaders. The desire for a "clear picture going forward," as expressed by Steven A. Schneider, is directly tied to the need for predictable and stable policy frameworks. Until such clarity emerges, businesses may continue to adopt a more cautious stance, prioritizing short-term resilience over long-term, ambitious expansion.

In conclusion, the latest CEO Confidence Index paints a picture of a business landscape characterized by a cautious step forward in current conditions, yet marked by significant divisions regarding the future. While the immediate environment offers glimmers of stability, the persistent influence of geopolitics, inflation, and policy uncertainty necessitates a strategic approach that balances immediate operational needs with a keen awareness of evolving global dynamics. The coming months will be critical in determining whether this fragile optimism can translate into sustained growth or if the weight of external factors will continue to temper future expectations.