A recent survey of U.S. Chief Executive Officers reveals a significant dichotomy in corporate strategy: while a substantial majority recognize the critical importance of expanding into new categories, markets, and offerings for future growth and competitiveness, their current revenue streams remain heavily anchored to products and services developed over five years ago. This paradox highlights a potential challenge for businesses navigating an increasingly dynamic economic landscape, where innovation and adaptation are paramount.

The findings, compiled from a survey of 315 U.S. CEOs conducted by Chief Executive, indicate that a significant portion of corporate revenue is derived from established, long-standing business activities. Specifically, 58 percent of surveyed CEOs reported that less than 10 percent of their company’s current revenue originates from products or services introduced within the last five years. Conversely, only approximately one in four CEOs indicated that at least 20 percent of their revenue now stems from newer offerings, underscoring a prevailing reliance on their existing business models.

Despite this current revenue reality, forward-looking strategies reveal a strong consensus on the necessity of diversification. Looking ahead three to five years, a striking 77 percent of CEOs identified expansion into new categories, markets, or offerings as either "critical" or "important" for their company’s ability to grow and maintain a competitive edge. Nearly 30 percent of this group deemed such expansion "critical," signaling a high level of strategic urgency. This sentiment is further reinforced when CEOs were asked about their companies’ past five years of activity; while 43 percent acknowledged entering new sectors, customer categories, markets, or use cases, they reported these initiatives have had only a limited impact on revenue. Only 22 percent stated that these new ventures have become a significant source of revenue or growth.

This situation arises in an era where technological advancements, particularly in artificial intelligence (AI), are rapidly compressing product cycles and creating novel use cases. Competitive threats are no longer confined to direct rivals; they increasingly emanate from adjacent market segments, disruptive business models, and companies that fundamentally redefine customer problems. Mark Grosskopf, CEO of New Resources Consulting, articulated this evolving threat landscape, stating, "AI will have a very large impact much sooner than most expect… all need a plan to address their business model." His assessment underscores the imperative for businesses to proactively re-evaluate their strategies in light of impending technological shifts.

Investment in Research and Development: A Mixed Picture

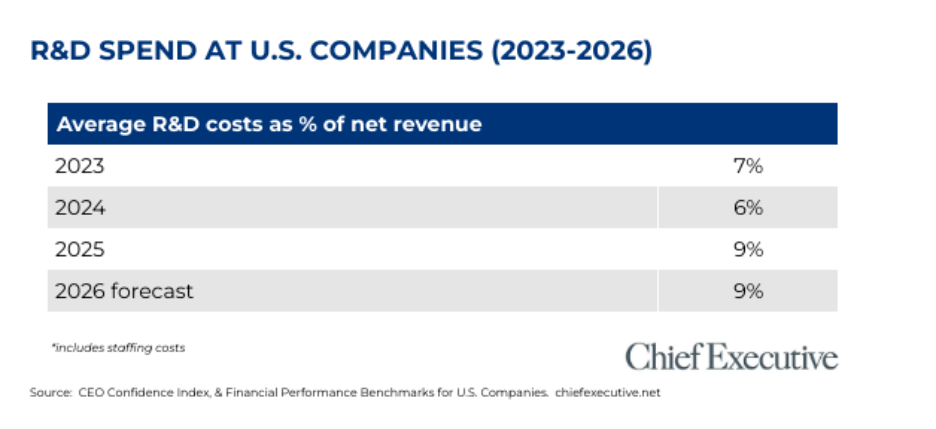

While the drive for innovation is acknowledged, the level of investment in Research and Development (R&D) presents a varied picture across U.S. companies. According to Chief Executive‘s Financial Performance Benchmarks Report for U.S. Companies, R&D costs represented an average of 8.8 percent of net revenues in 2025, with a projected increase to 9.4 percent for 2026. This marks an increase from prior readings of 7 percent in 2023 and 6 percent in 2024.

However, these averages warrant careful interpretation. R&D spending can be significantly skewed by early-stage companies or those in technology-intensive sectors, which often have lower revenue bases and consequently higher R&D-to-revenue ratios. The median response for R&D spending offers a more nuanced perspective, standing at a more modest 5 percent for both 2025 and 2026. This suggests that for a considerable number of companies, formal R&D activities constitute a relatively small proportion of their overall revenue. This median figure might indicate a cautious approach to R&D investment for many established businesses, potentially creating a lag in their ability to translate future growth aspirations into tangible new revenue streams.

Ownership Structure and Expansion Propensity

A key differentiator emerging from the survey is the influence of ownership type on a company’s propensity for expansion. Private equity-backed companies, in particular, demonstrated a strong orientation towards expansion. Nearly one-third of these firms reported that new sectors, categories, markets, or use cases have become a significant source of revenue or growth. Furthermore, an impressive 88 percent of private equity-backed CEOs deemed expansion into new areas critical or important for future competitiveness. This aggressive posture is often characteristic of private equity’s investment thesis, which typically involves driving growth and market share through strategic acquisitions and the development of new revenue streams within portfolio companies.

In contrast, family-owned companies exhibited a more conservative approach. They were less likely to report that new areas have become significant revenue sources and were also less inclined to categorize future expansion as critical or important for their competitiveness. Taymi Marrero, CEO of manufacturer Ground Power Parts, expressed concern over this disparity. "As a small business owner for over 10 years," Marrero stated, "the biggest challenge I see in the future is big Corps taking over market share and leaving little to no opportunity for growth recovery and expansion for smaller family-owned companies. That is where our country is headed in almost every sector." Her observation highlights a potential vulnerability for smaller, family-run businesses in an increasingly consolidated market, where larger, more aggressive entities might be better positioned to capitalize on expansion opportunities.

Sectoral Variations in Innovation and Growth

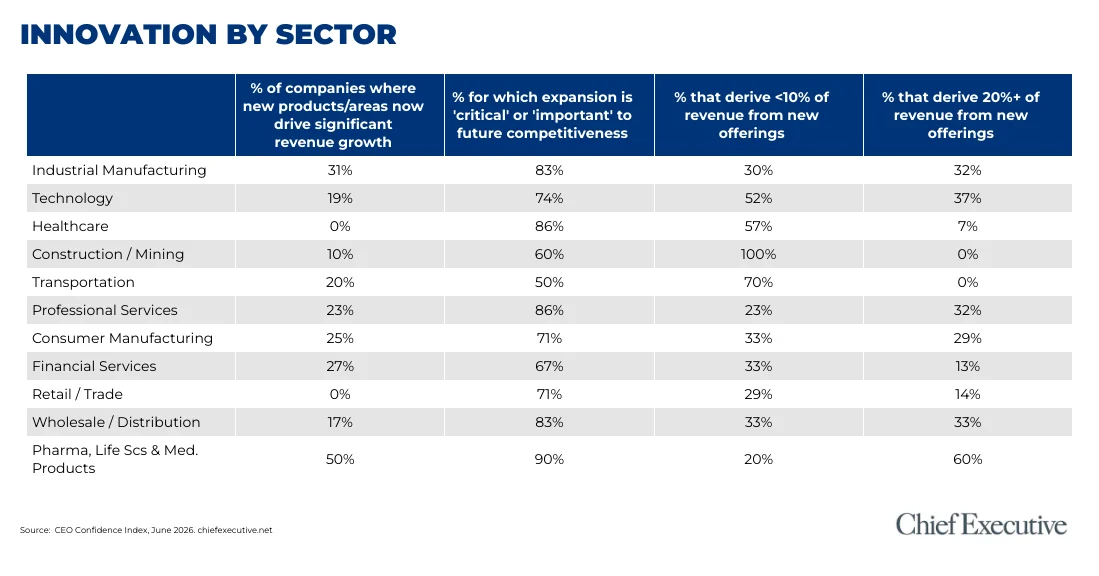

The survey also revealed significant variations in innovation and expansion strategies across different industry sectors. Industrial manufacturing, representing the largest industry group surveyed, stood out for its proactive approach to innovation. A notable 31 percent of CEOs in this sector indicated that expansion into new sectors, customer categories, markets, or use cases had already become a significant source of revenue or growth. This figure surpasses the overall average of 22 percent. Moreover, over 80 percent of industrial manufacturing CEOs believe that such expansion will be critical or important for their competitiveness over the next three to five years. This suggests a sector that, despite its traditional roots, is actively embracing diversification as a core strategic pillar.

Companies in the technology, software, and telecommunications sectors also reported robust R&D spending as a share of revenue. These firms were also more likely than the general surveyed group to state that at least 20 percent of their revenue has come from offerings introduced within the past five years. This aligns with the inherent nature of these industries, which are characterized by rapid technological evolution and a constant need for product and service updates to remain competitive.

However, the picture is less optimistic in other sectors. In healthcare, none of the surveyed CEOs reported that expansion into new sectors, customer categories, markets, or use cases had become a significant source of revenue or growth. Despite this, a substantial 86 percent of healthcare CEOs still consider such expansion critical or important for future competitiveness. This indicates a clear strategic intent that has not yet translated into significant current revenue generation, pointing to potential long-term challenges or delays in the adoption and commercialization of new healthcare innovations. Similarly, in the construction and mining sectors, CEOs reported that less than 10 percent of their revenue is derived from products or services not offered five years ago, suggesting a slower pace of innovation and diversification within these industries.

Implications for the Future

The findings from the Chief Executive survey paint a complex picture of corporate America. On one hand, there is a clear strategic vision among CEOs recognizing the indispensable role of expansion and innovation in securing future growth and competitiveness. On the other hand, the persistent reliance on legacy revenue streams suggests a considerable gap between strategic intent and current operational reality.

This discrepancy could pose significant risks. In a global economy characterized by rapid technological disruption, evolving consumer preferences, and intense competition, companies that fail to effectively translate their expansion strategies into tangible revenue growth may find themselves outmaneuvered by more agile competitors. The relatively modest median R&D spending, especially for non-technology-centric businesses, further amplifies this concern, potentially indicating a reluctance to invest sufficiently in the foundational research and development required to create truly novel offerings.

The observed differences based on ownership type also highlight a potential divergence in market dynamics. The aggressive expansion strategies of private equity-backed firms could lead to increased market consolidation, potentially creating greater challenges for family-owned and other privately held businesses that adopt a more cautious approach.

As the business landscape continues to evolve, the ability of CEOs to bridge the gap between their stated growth ambitions and their current revenue generation will be a critical determinant of long-term success. The insights from this survey serve as a timely reminder that while acknowledging the importance of future expansion is a crucial first step, the real test lies in the execution and successful integration of new categories, markets, and offerings into the core of their business operations. The next few years will likely reveal which companies are truly prepared to embrace the transformative changes necessary to thrive in the modern economy.