The allocation to alternative assets, particularly private debt and infrastructure, has surged over the past decade, extending beyond institutional investors to encompass wealth management clients. This trend is bolstered by regulatory shifts like the introduction of ELTIF structures in Europe and governmental calls to broaden access to private investments for individual retirement plans. While investors are drawn to private markets for their potential for higher risk-adjusted returns and unique sustainable investing opportunities, they are concurrently facing the challenge of managing increasingly complex portfolios. This article delves into strategies for effectively managing the pervasive impact of liquidity risk across various facets of the investment process, building upon previous discussions on strategic asset allocation and implementation.

Understanding the Nuances of Illiquidity Risk

Illiquidity risk, inherent in assets lacking deep secondary markets and characterized by lengthy transaction processes, profoundly affects traditional asset owner investment practices, commencing with asset-liability management (ALM) studies. The absence of readily available buyers and sellers introduces considerable uncertainty regarding the timing and quantum of cash inflows and capital calls. This unpredictability can lead to significant over- or under-allocations to illiquid assets, complicating the execution of de-risking strategies when market conditions necessitate such adjustments. A substantial proportion of illiquid assets inherently curtails an investor’s flexibility to reallocate capital between asset classes. In practice, this often translates to delayed rebalancing or smaller-than-intended transactions.

A related concern is the "denominator effect." During periods of significant market correction, such as the notable downturn in 2022, the proportion of illiquid assets within a portfolio can swell considerably, even without any new investment. This is particularly acute for investors with a high concentration of interest-rate sensitive assets, like pension funds, which are vulnerable to adverse consequences. The constrained ability to rebalance can result in substantial deviations from the pre-defined investment strategy, potentially jeopardizing long-term objectives.

Furthermore, the absence of robust secondary markets raises the risk that asset prices may not accurately reflect their true value in an arms-length transaction. The reliance on valuation models for illiquid assets introduces model risk. Consequently, investors might find themselves in a position where an asset’s value has diminished, but its reported price has yet to catch up. This phenomenon, often termed "stale pricing," means that valuations for illiquid assets tend to be less volatile and lag behind major market movements. This lag complicates the evaluation of traditional risk measures and correlations between illiquid asset classes and their liquid counterparts, compelling allocators to rely more heavily on qualitative judgment.

Information pertaining to individual illiquid investments is frequently proprietary and not widely disseminated. This scarcity of data makes it increasingly arduous for asset owners to ascertain the quality of their holdings, especially when external asset managers act as intermediaries. The bankruptcy of First Brands Group, for instance, caught some private market lenders off guard due to undisclosed significant off-balance sheet liabilities. In such scenarios, asset owners cannot solely depend on the asset manager for accurate and timely information regarding loan quality. Demanding transparency beyond the standard information package, particularly when investing with established managers overseeing substantial strategies, can prove challenging.

Strategic Approaches to Mitigating Illiquidity Risk

Addressing the multifaceted challenges posed by illiquid assets requires a comprehensive approach, integrating measures across the entire investment lifecycle. A combination of these strategies can effectively mitigate, if not entirely neutralize, certain aspects of illiquidity risk.

Integrating Illiquidity into ALM Studies

The ALM process must explicitly incorporate the impact of illiquidity. The inherent lag in pricing for illiquid assets creates an artificial impression of lower correlation with liquid asset classes and reduced volatility. In unconstrained optimization models, this can lead to allocations to illiquid assets that expose the portfolio to substantially higher risks than suggested by traditional metrics. Consequently, for real-world portfolios, imposing constraints on optimization models is often prudent. This can include setting maximum allocation limits for specific asset classes or groups of asset classes. Employing stress tests is a recommended practice for informing these maximum allocation thresholds. For instance, one might mandate that the proportion of illiquid assets does not exceed a defined limit following the impact of rising interest rates or a severe downturn in liquid markets.

Another method to address illiquidity in ALM studies is to introduce a "liquidity penalty" into the optimization function. This could involve deliberately adjusting the risk measures of illiquid asset classes upward, beyond what the data might otherwise suggest, or incorporating a penalty factor for these asset classes alongside their risk and return profiles. Furthermore, enforcing greater portfolio diversification by penalizing concentration can enhance resilience.

Correlations and risk metrics for illiquid asset classes can also be derived from comparable liquid asset classes. For example, it might be reasonable to assume that over a defined horizon, such as one year, direct lending spreads exhibit a high correlation with single-B rated high-yield bond spreads and senior bank loan spreads. The correlation of direct lending with other asset classes, like equities, can then be inferred from the correlation between high-yield bonds and equities.

Liquidity stress testing should also be a standard component of ALM studies. Asset mixes must possess sufficient liquidity under stressed market conditions. This is particularly critical for investors managing portfolios with long durations in interest-rate or inflation derivatives, as these positions necessitate liquid collateral when real or nominal rates move adversely. Best practice dictates pre-defining a liquidity waterfall and applying haircuts to simulate the effects of forced selling under potentially stressed market circumstances. As demonstrated by the 2022 UK Gilt crisis, even highly illiquid investments like private equity can be sold rapidly, but this often comes at the cost of significant discounts.

Enhancing Implementation Strategies

Given that adjustments to private market asset class allocations cannot be made swiftly, investors incorporating these segments must establish a clear plan for building, maintaining, and adjusting their exposures. Investment teams and managers need a precise understanding of capital deployment targets for each vintage year. This is an integral aspect of liquidity planning, ensuring the capacity to meet capital calls and other potential payment obligations, such as pension disbursements. Investors should position themselves to minimize the likelihood of being compelled to sell assets under duress. Liquidity can evaporate during market turbulence, and investment redemptions may be subject to fees, penalties, and gating mechanisms.

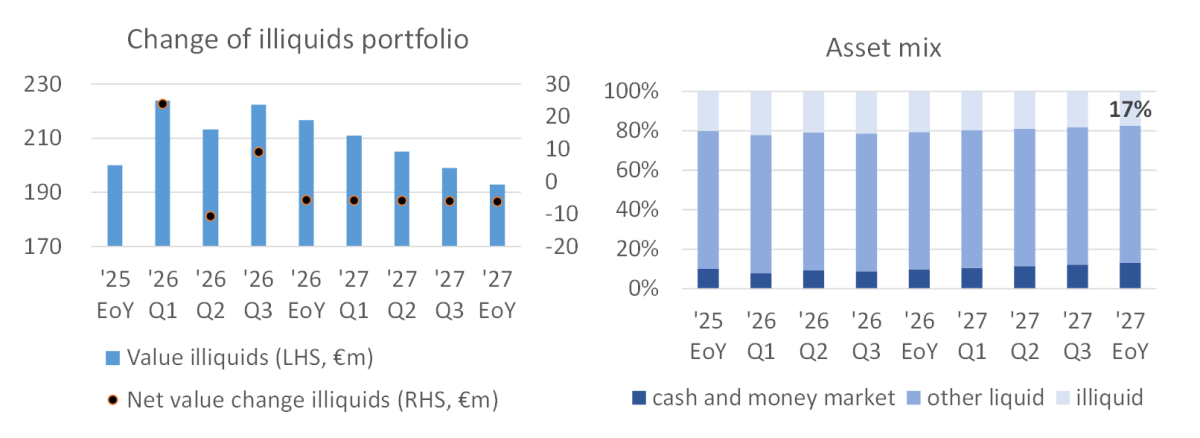

To illustrate the potential investment quandaries arising from illiquid asset investments, consider a hypothetical scenario involving an investor with a substantial illiquid investment program, initially allocating 20% of a €1 billion balance sheet. This 20% represents the target exposure for illiquid investments. By the end of 2025, outstanding commitments necessitate capital calls, while simultaneously, there are anticipated (though uncertain) distributions from the illiquid asset portfolio. The initial charts in Figure 1 depict the expected portfolio evolution by the end of 2025. Anticipated distributions are projected to outweigh capital calls, leading to a gradual run-off of the illiquid allocation, reaching approximately 17% by the close of 2027. At the beginning of 2026, a decision is made to commit €40 million to new illiquid investments, with capital expected to be called over the eight quarters following the end of 2026.

Fast-forwarding to the future, the middle panel of Figure 1 illustrates the portfolio’s development with this additional capital, assuming realizations align with the expectations formulated at the end of 2025. If all projections hold true, the allocation to illiquid assets by the end of 2027 stands at 20%, precisely on target.

The bottom panel reveals a different outcome if plans are disrupted. Suppose that after committing the €40 million, the investor learns that the planned distributions throughout 2026 and 2027 are deferred by an additional year. Instead of addressing a 3% allocation gap (a 17% allocation to illiquid investments if no new capital were committed versus the 20% target), the allocation to illiquid assets by the end of 2027 is projected to be 3% above the target.

Figure 1: Charts on the left depict the stock of illiquid assets and their mutations. Charts on the right show the asset mix. The top panels reflect expectations at the end of 2025. The middle and bottom panels illustrate the realization of these expectations when additional commitments are made to illiquid assets during 2026. The middle panel represents a base-case scenario with the same distribution assumptions as the top panel. The bottom panel demonstrates the impact of a one-year delay in expected distributions.

The inherent nature of illiquid markets makes forecasting capital deployment and repatriation timelines challenging. As investors in private equity are currently experiencing, private equity firms often struggle to return cash to their investors when market circumstances shift. While investors can rely on estimates of deployment and repayments from external asset managers or internal teams, supplementing this with stress testing and scenario analysis on expected cash flows is crucial. A second strategy for managing these implementation issues involves acknowledging in ALM studies that exposure to illiquid asset classes will naturally deviate from targets and stress-testing the asset mix under scenarios where both portfolio ramp-up and distributions significantly exceed or fall below expectations.

There is, unfortunately, no panacea. Investors are ultimately subject to external developments when committing capital. However, through meticulous planning and the utilization of stress testing to maintain adequate buffers, the associated risks can be effectively managed.

Optimizing the Operational Framework

Investing in illiquid alternative assets is not only more complex from a modeling perspective but also presents greater day-to-day operational demands. The staffing of both the investment and back-office teams must be commensurate with the complexity of the investor’s portfolio. Beyond internal resources, this can involve engaging external partners such as specialized investment consultants and investment reporting services. An organization must possess appropriate systems and adequate personnel to manage pending capital calls. A larger asset base or significant internal resources can facilitate the management of more complex portfolios. As a general rule, organizations should identify an asset allocation that aligns with their size and available team resources, gradually building additional capacity where necessary.

It is widely recognized that the dispersion of manager performance in illiquid asset classes can be substantial. Consequently, manager selection in alternatives is even more critical than in traditional asset classes. Organizations must therefore dedicate considerable time to designing a robust manager selection process. Investors may also consider diversification within asset classes by incorporating dimensions such as manager, sector, and vintage year.

Conclusion: Navigating the Illiquid Landscape

Over the past decade, the proportion of alternative assets in institutional and private wealth portfolios has grown significantly, leading to increased portfolio complexity and illiquidity. Investors are well-advised to develop a clear understanding of their liquidity requirements, which will, in turn, inform the definition of target allocations for illiquid asset classes within their strategic asset allocation framework. In the implementation phase, liquidity planning and investment planning are paramount for building out asset classes and managing cash flows effectively. Within illiquid asset classes, diligent manager selection and diversification across multiple dimensions are key to mitigating selection risk.

Andreas Rothacher is the Head of Investment Research at Complementa AG, advising institutional clients on strategic asset allocation and manager selection. He is a co-author of Complementa’s annual Swiss pension fund study (Risk Check-up) and has authored numerous articles and publications. Andreas serves as the Chapter Head of the CAIA Zurich Chapter and is a member of the CFA Swiss Pensions Conference Committee. His prior experience includes roles at a German family office, UBS, and Credit Suisse.

Richard Sanders is an experienced asset allocator specializing in fixed-income portfolios for institutional investors. He has advised sovereign wealth funds, pension funds, and insurance companies on manager selection and asset allocation, and managed the liquid investments of insurance firm NN Group. He currently leads asset allocation and external manager selection activities at Cöoperatie VGZ, a Dutch healthcare insurance organization.

Learn more about CAIA Association and how to become part of a professional network shaping the future of investing by visiting https://caia.org/