Eleanor Viney, Neil McCarthy, and Emily Drazan Chapman, with contributions from DragonGC, present a comprehensive analysis of the diminishing prominence of the Environmental, Social, and Governance (ESG) framework. Their findings, detailed in a recent DragonGC memorandum, reveal a significant retreat in both corporate disclosures and investor focus, driven by a confluence of regulatory, political, and market developments. This report quantifies this shift through an examination of ESG terminology in S&P 500 and Fortune 1000 filings and an analysis of capital flows out of ESG-designated mutual funds and ETFs.

Executive Summary: The Ebbing Tide of ESG

The ESG framework, once a cornerstone of corporate governance and sustainable finance, is experiencing a notable decline. This contraction is evident in two key areas: the strategic elimination and rebranding of ESG terminology within corporate disclosures, particularly in S&P 500 and Fortune 1000 DEF 14A proxy and Form 10-K filings, and a sustained capital exodus from ESG-designated mutual funds and Exchange Traded Funds (ETFs). The collective impact of recent regulatory pressures, political shifts, and evolving market dynamics indicates a significant turning point, signaling a waning influence of ESG narratives and investment strategies.

ESG Disclosures: A Narrative Shift in Corporate Filings

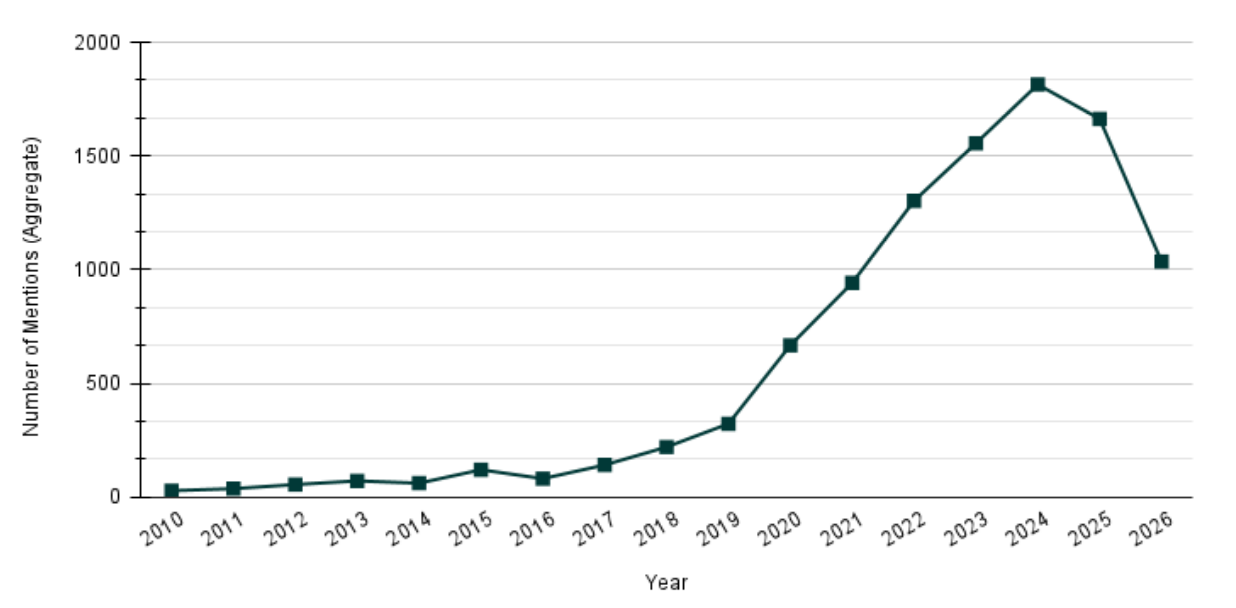

At the disclosure level, an analysis of aggregate "sustainability" keyword mentions in S&P 500 DEF 14A proxy filings reveals a peak in 2024, followed by the first recorded decline in 2025. Recent 2026 proxy filings suggest this decline is accelerating, indicating a more pronounced shift away from explicit ESG language. The case of Target Corporation provides a compelling illustration of this trend, showcasing a deliberate "greenhushing" strategy where ESG elements are progressively downplayed or reframed.

However, a nuanced perspective emerges when examining Form 10-K filings. Within the "Item 1A. Risk Factors" section, the term "sustainability" continues to see increased usage at the aggregate index level. This suggests that while companies may be reducing overt ESG pronouncements in public-facing disclosures, there remains a heightened awareness and ongoing monitoring of sustainability-related risks, particularly in the context of potential litigation and regulatory scrutiny. This dichotomy highlights a strategic repositioning rather than a complete abandonment of the underlying concerns.

Capital Flows: Investors Withdraw from ESG Funds

DragonGC’s analysis of data published by the Investment Company Institute (ICI) quantifies the waning investor support for ESG investments. ESG-designated funds experienced a net outflow of $935 million in January 2026, marking the fourteenth consecutive month of negative flows. This trend is further underscored by a contraction in the number of ESG funds, which has decreased by 100 since January 2025. The reported total Assets Under Management (AUM) of $629 billion reflects market appreciation on existing holdings rather than new investor conviction, a critical distinction that can mask underlying withdrawal trends.

Key Finding: Regulatory Pressure Drives the ESG Retreat

The synchronized decline in ESG disclosures and the capital retreat from ESG funds can be directly attributed to a heightened regulatory and political environment. The proliferation of anti-ESG state legislation, mandates for pension fund divestment, and an emerging judicial framework that characterizes ESG mandates as potentially exhibiting "unconstitutional vagueness" in fiduciary contexts have collectively created significant headwinds. The once-powerful momentum behind ESG initiatives appears to be significantly abating.

Section I: Trends in ESG Disclosures

Industry-Wide Proxy Disclosure Data

An extensive analysis of S&P 500 and Fortune 1000 DEF 14A proxy filings and Form 10-K filings spanning from 2010 to 2026 provides a clear picture of the evolving disclosure landscape. The frequency of the term "sustainability" serves as a key metric for quantifying these shifts.

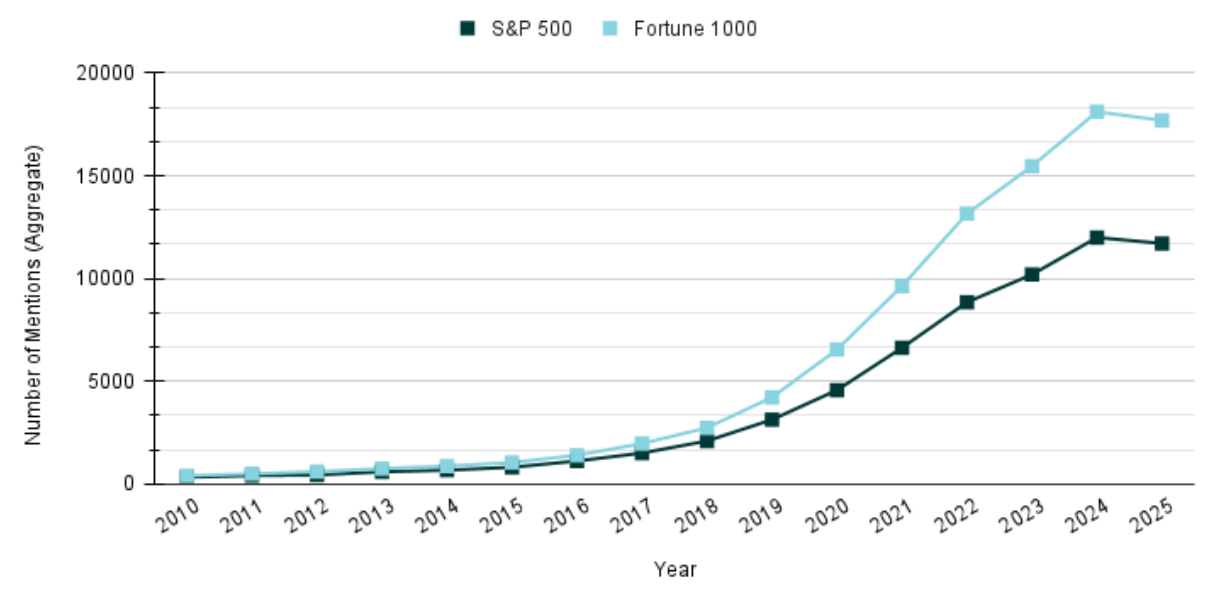

Chart 1: DEF 14A Proxy Filings: "Sustainability" Keyword Count (2010-2025)

From 2010 through 2024, both the S&P 500 and Fortune 1000 indices demonstrated consistent growth in the mentions of "sustainability" within their DEF 14A proxy filings. This period of expansion, particularly around 2020, coincided with a generally favorable political and regulatory climate for ESG initiatives. The modest decline observed in 2025, with approximately 289 fewer mentions for the S&P 500 and 413 for the Fortune 1000, is statistically significant as it marks the first reversal of a multi-year growth trend. This contraction is largely attributed to companies responding to mounting pressure from anti-ESG legislation by adopting "greenhushing" practices, a strategy of deemphasizing voluntary sustainability disclosures.

- Key Observations from Chart 1:

- The Fortune 1000 consistently shows a higher mention count, approximately 1.5 times that of the S&P 500, reflecting the larger corporate pool. The proportional adoption rate, however, remains consistent across both groups.

- The simultaneous peak in 2024 and subsequent modest decline in 2025 across both indices suggest a collective corporate response to prevailing political and regulatory pressures.

- Despite the decline, "sustainability" mentions in 2025 remained at historically elevated levels, exceeding 2023 figures, indicating that the retreat is still in its nascent stages.

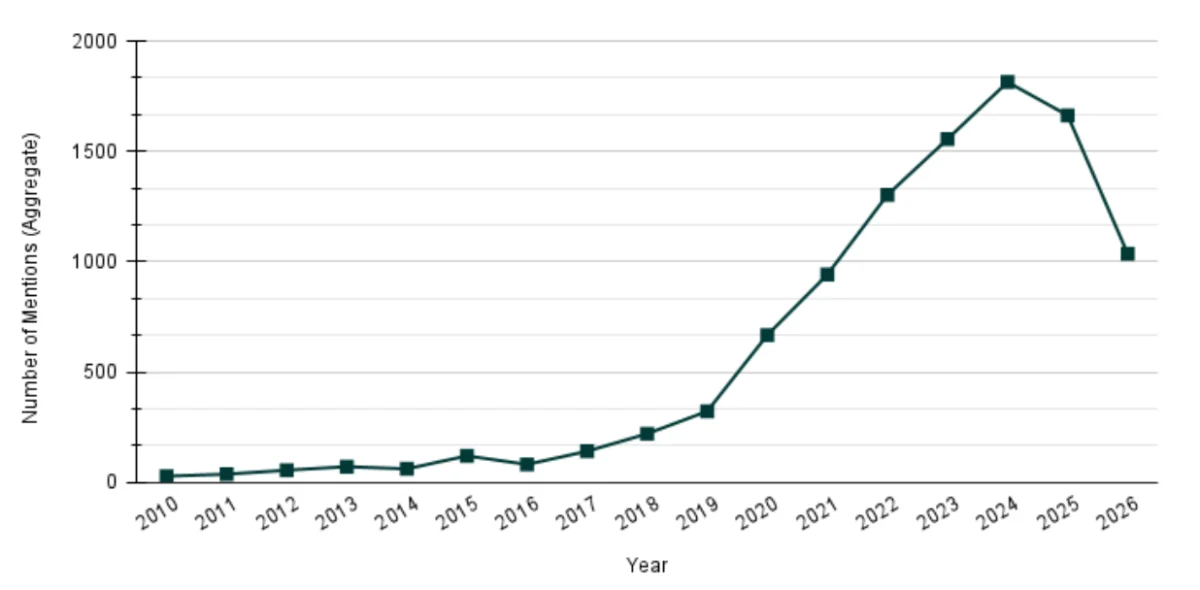

Chart 2: DEF 14A Proxy Filings: "Sustainability" Keyword Count (2010-2026 YTD)

Early analysis of 2026 DEF 14A proxy filings paints a more concerning picture for ESG disclosures. Data from a subset of 50 Fortune 1000 companies that have filed their 2026 proxy statements reveals a more dramatic decline in the "sustainability" keyword count compared to 2025, falling below 2022 levels. This suggests that the impact of anti-ESG regulation continues to be a potent force shaping corporate disclosures during the current proxy season.

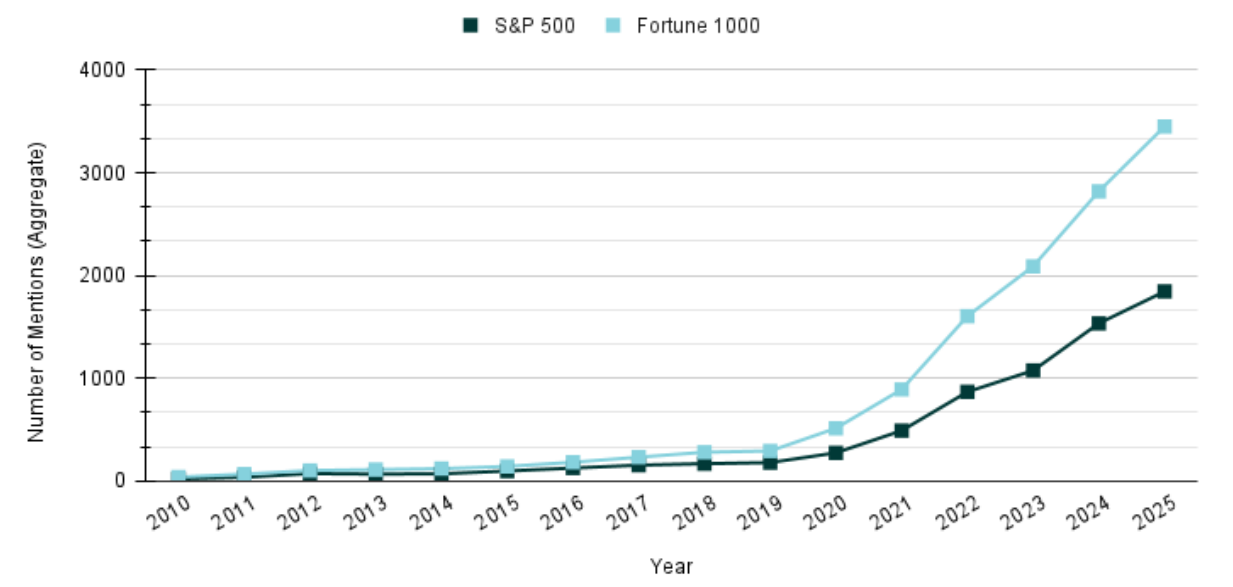

Chart 3: Form 10-K Filings: "Sustainability" Keyword Count (2010-2025)

In contrast to the voluntary disclosures in proxy statements, Form 10-K filings offer a different perspective. The "Item 1A. Risk Factors" section of these annual reports shows a continuous growth in the mentions of "sustainability" from 2010 through 2025 for both S&P 500 and Fortune 1000 companies, with significant acceleration post-2020. This divergence indicates that while companies are reducing explicit ESG pronouncements, they are increasingly recognizing and disclosing sustainability as a material risk factor. This strategic inclusion is likely driven by a desire to manage liability and avoid potential litigation stemming from investor losses if sustainability-related risks are not adequately disclosed. The legal and regulatory pressures influencing these disclosures are distinct from those impacting proxy statements.

Case Study: Target Corporation – A Stark ESG Rebranding

Target Corporation’s proxy statement history from 2021 to 2025 provides a granular view of the ESG narrative retreat. Over four proxy cycles, Target transitioned from minimal disclosure in 2021 to peak ESG branding in 2023, followed by a complete elimination of explicit ESG terminology by 2025.

-

Target Corp: ESG & Sustainability Proxy Mention Counts (2021-2025)

- 2021: A baseline year with only one mention of "sustainability" and 12 mentions of "ESG," confined to the Board’s Risk Oversight section. ESG was viewed primarily as a compliance and risk function.

- 2022: Marked a significant shift with the launch of "Target Forward" and the renaming of the Governance Committee to the "Governance & Sustainability Committee." Mentions increased to 49 for "sustainability" and 46 for "ESG." "ESG Understanding" was added as a director skill criterion.

- 2023: Reached peak disclosure density, with 70 "sustainability" mentions and 62 "ESG" mentions. ESG was framed as a core strategic and brand identity, with ESG skills highlighted in director biographies and comprehensive documentation of stakeholder engagement.

- 2024: The rebranding initiative began, with a significant reduction in explicit "ESG" references (down to 2) and a preference for "sustainability." The "Sustainability & ESG" section was renamed "Sustainability Matters," and sustainability was reframed to serve "long-term growth and value creation."

- 2025: Completed the ESG elimination. "ESG" appeared zero times. Most "sustainability" mentions originated from the committee name. Target Forward was removed, and the "Sustainability Matters" section was significantly reduced. The director skills criterion was redefined as "Sustainability and governance," with a focus on "business resiliency matters," stripping away explicit environmental, social, or governance content.

This progression demonstrates a clear "U-turn" where "sustainability" has been reframed from environmental stewardship to principles of long-term value creation and business resiliency, effectively distancing it from the politically charged ESG label.

Section II: ESG Retreat in Numbers

Key Findings at a Glance

The data on ESG fund flows and performance offers a stark quantitative perspective on the retreating investor interest.

Executive Overview: The Investor Exodus

ESG mutual funds and ETFs are experiencing a sustained investor exodus that began in mid-2022 and has intensified since the 2024 elections. DragonGC’s analysis of ICI data indicates a net outflow of $935 million from ESG-designated funds in January 2026, the fourteenth consecutive month of negative flows. The number of ESG funds has declined by 100, a 12% contraction, since January 2025. While total ESG fund assets have grown to $629 billion, this figure is largely driven by market appreciation on existing investments, not new capital inflows.

Core Distinction Between Assets and Flows

It is crucial to differentiate between total AUM and net fund flows. Rising total assets can be misleading, as they can reflect market gains on existing investments rather than new investor enthusiasm. A fund may report record AUM while simultaneously experiencing significant outflows. The $935 million net outflow in January 2026 unequivocally represents deliberate investor withdrawal.

Flow Reversal: From Expansion to Sustained Outflows

Between 2019 and early 2022, ESG funds were a rapidly growing segment of the investment industry, fueled by strong performance in ESG-aligned technology stocks and increasing regulatory encouragement for sustainability frameworks. This trend reversed sharply in mid-2022 as rising interest rates disproportionately impacted growth stocks, which often form the core of ESG portfolios. This was followed by significant political headwinds, including anti-ESG legislation in Republican-led states that mandated pension fund divestments from major asset managers. By late 2022, monthly outflows became the norm for dedicated ESG funds.

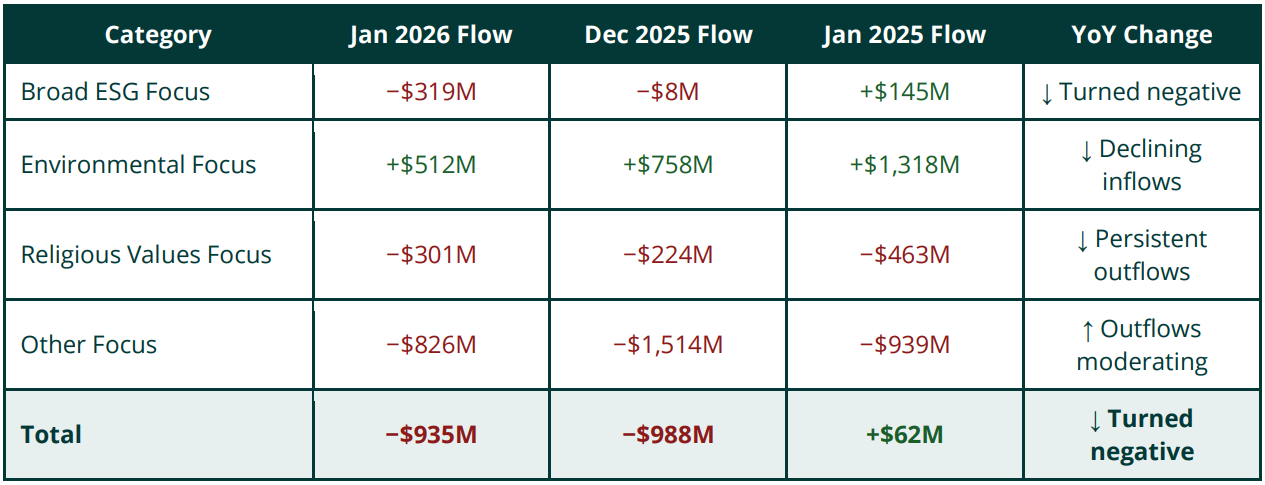

Monthly Net Flows by Category – January 2026

The ICI categorizes ESG fund flows into four segments, revealing varied performance:

- Broad ESG Focus: This category experienced a $319 million outflow in January 2026, a significant turnaround from a $145 million inflow one year prior, representing a $464 million swing in twelve months.

- Environmental Focus: This segment remains the most resilient, sustaining net inflows of $512 million. However, this represents a sharp decline from $1.318 billion in inflows a year earlier.

- Religious Values Focus and Other Focus: These categories also saw mixed results, with the "Other Focus" category experiencing net outflows.

Environmental Focus: Growing, But at a Slower Pace

Environmental Focus funds have consistently maintained positive net inflows throughout the 14-month outflow streak affecting broader ESG categories. This resilience is likely attributable to the strong performance of clean energy and climate solutions equities, attracting investors who may be less sensitive to political shifts. Nevertheless, the rate of these inflows is rapidly decelerating, raising questions about the long-term sustainability of this trend, especially if this category also enters a period of sustained outflows.

Total Assets: Market Appreciation as a Headline Distortion

The Environmental Focus category, despite being the smallest in absolute AUM at $83.5 billion, displayed the highest year-over-year asset growth at 24.7%. This growth is primarily driven by the robust performance of clean energy equities. In contrast, the Broad ESG Focus category grew by a mere 2.1%, barely keeping pace with inflation and reflecting both sustained outflows and an equity composition that is underperforming the broader market.

Fund Count Contraction: Further Evidence of Retreat

The Broad ESG Focus category has seen a significant reduction of 69 funds, representing over one-fifth of its January 2025 total. Overall, the total ESG fund count has declined from 835 to 735, a 12% year-over-year decrease. This structural contraction indicates a deliberate strategic retreat by fund sponsors from ESG-labeled investment products, as they deem the ESG label insufficient to attract the necessary flows to maintain viable fund economics.

Conclusion: Retreat Across Language and Capital

The data analyzed unequivocally confirm that anti-ESG sentiment is driving a significant retreat from the ESG framework, impacting both corporate disclosure language and investor capital allocation. ESG disclosures, as measured by keyword counts, declined in 2025, with early 2026 data forecasting a more pronounced reduction for the upcoming proxy season. The rebranding efforts, exemplified by Target Corporation, and the substantial capital outflows from ESG-labeled funds underscore this trend.

The common denominator fueling this retreat is a challenging regulatory and political environment that has introduced material legal, reputational, and fiduciary risks to explicit ESG positioning.

- State-Level Regulatory Pressure: Over 20 states have enacted anti-ESG legislation, creating enforceable prohibitions on state pension fund allocations to managers perceived as prioritizing ESG factors over financial returns. This has led to documented pension fund withdrawals from major asset managers, disincentivizing ESG investment.

- Federal Judicial Scrutiny: Emerging legal cases in 2025-2026 are testing ESG mandates under the doctrine of "unconstitutional vagueness," arguing that ill-defined ESG criteria cannot serve as legally enforceable fiduciary standards. While no definitive circuit precedent has been established, the litigation risk is significant enough to prompt preemptive rebranding efforts by corporations. Legal counsel is advising that explicit ESG commitments in governance documents could be used as admissions in derivative litigation or state enforcement actions.

- Federal Regulatory Rollbacks: The SEC’s rollback of its climate disclosure rule has removed a compliance-driven incentive structure that had sustained ESG adoption through 2023.

Concluding Assessment

The ESG framework is not being entirely abandoned by corporations; rather, it is undergoing a process of renaming and rebranding using non-ESG terminology. The evidence from capital markets is more definitive: investors are withdrawing from ESG-labeled products at a rate that cannot be solely attributed to performance differentials. The ESG label has become a liability in political landscapes where institutional capital is subject to significant state oversight. This shift suggests a recalibration of corporate and investor priorities, driven by a complex interplay of regulatory, legal, and market forces that are fundamentally reshaping the discourse around corporate responsibility and sustainable finance.