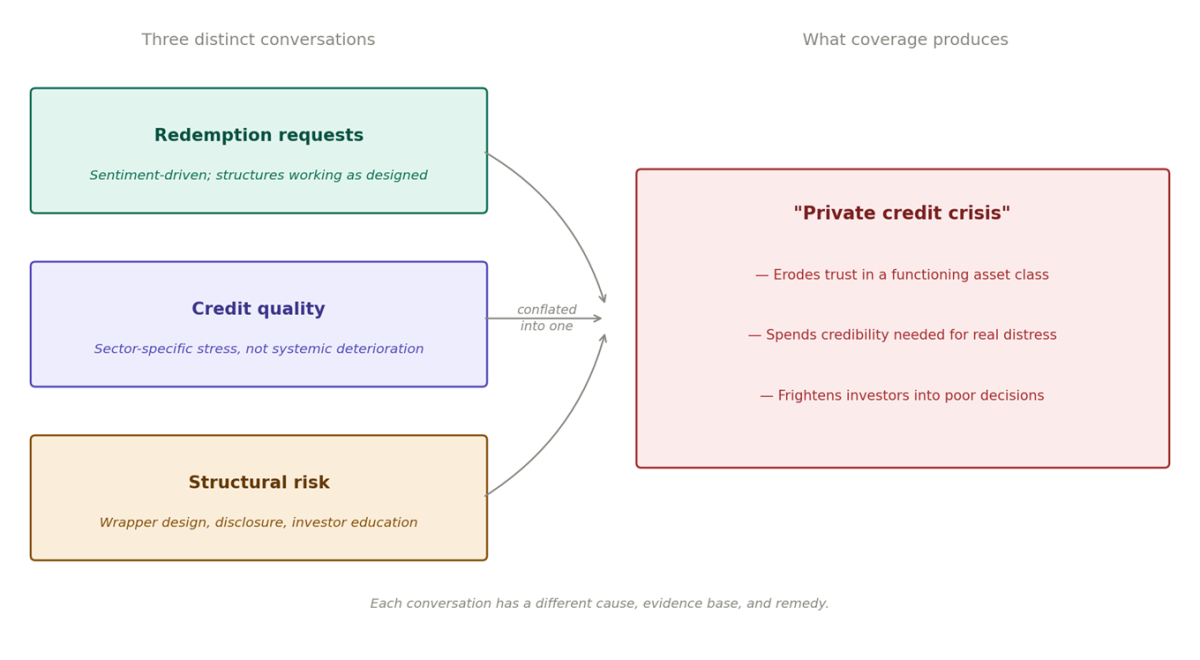

The financial headlines have been a cacophony of alarm bells, heralding doom for the $2.02 trillion private credit market. Reports range from predictions of systemic collapse to the chilling echoes of the 2008 financial crisis. However, a closer examination of the data reveals a more nuanced reality, a landscape where legitimate concerns are being conflated into a single, misleading crisis narrative. This aggregation of distinct issues – redemptions, defaults, and structural risks – risks eroding trust in a vital asset class and diminishing the industry’s analytical credibility for future, more critical junctures. It is imperative to disentangle these conversations to foster a clearer understanding of the private credit market’s current state and future trajectory.

The Surge in Redemption Requests: Sentiment Over Systemic Failure

A significant driver of the current market anxiety stems from a surge in redemption requests from retail investors in non-traded Business Development Companies (BDCs) and semi-liquid vehicles. These requests have triggered quarterly caps, leading to gates and capital lock-ups, which have been widely interpreted as evidence of a collapsing asset class. However, this interpretation conflates two fundamentally different dynamics: actual redemptions and redemption requests.

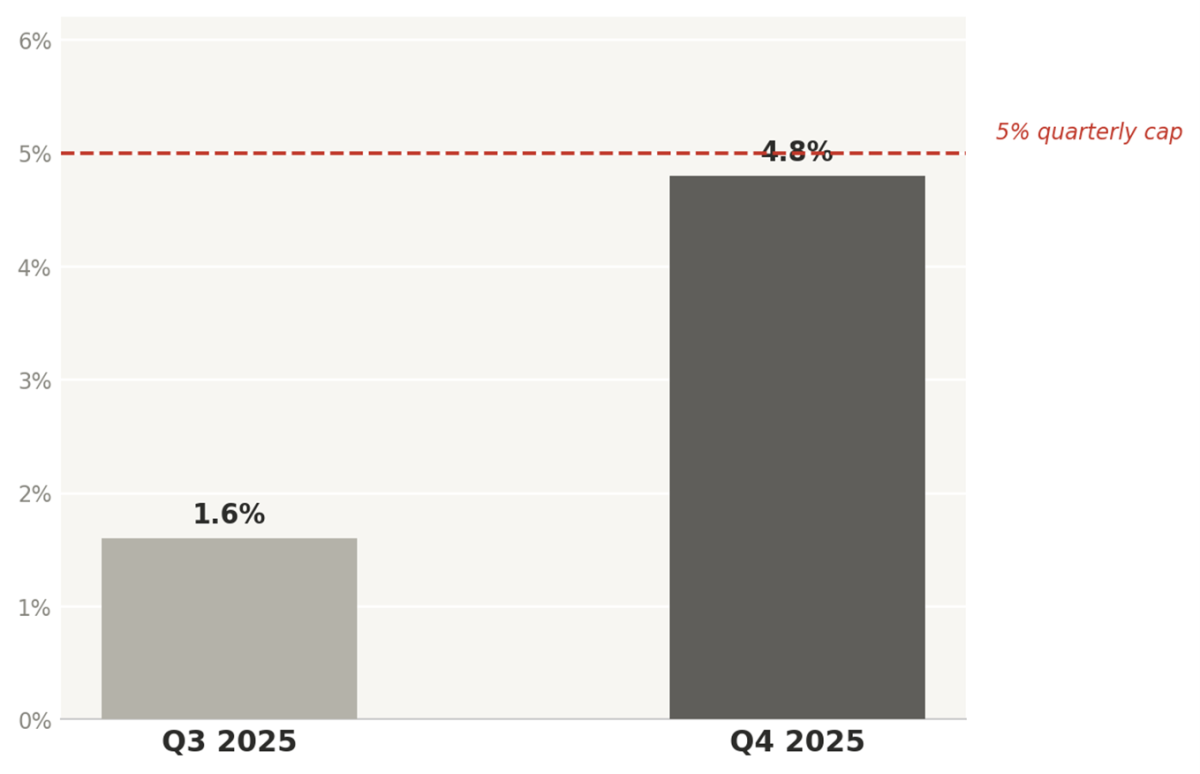

Actual redemptions, representing capital returned to investors, are capped at 5% of Net Asset Value (NAV) per quarter by design. What has surged is the volume of investors seeking to exit. This distinction is crucial. A spike in redemption requests is a powerful signal of investor sentiment, not an inherent indicator of credit deterioration. In the fourth quarter of 2025, average redemptions for perpetually non-traded BDCs rose to 4.8% of NAV, a significant increase from 1.6% in the third quarter of 2025. Five BDCs even funded tenders exceeding the standard 5% quarterly cap, a development that ignited widespread media attention and, according to some observers, an almost frenzied reaction.

Fitch Ratings attributes this surge in redemption requests primarily to sentiment rather than a broad-based decline in credit quality. A key concern appears to be investor apprehension regarding the potential disruption risk posed by Artificial Intelligence (AI) to software companies, a sector with significant exposure within many BDC portfolios. While this sentiment-driven outflow is concerning from a narrative perspective, it does not, in itself, represent a widespread judgment on the underlying quality of private credit portfolios.

The structures in place, including the 5% quarterly cap, are functioning as designed. These caps are not emergency measures but pre-existing features intended to safeguard the integrity of the loan book, maintain underwriting discipline, and protect the return profile for remaining investors. A manager adhering to these caps is acting within established parameters. The fact that these caps are being substantially oversubscribed, however, raises a more profound question: was the long-term, illiquid nature of these vehicles adequately communicated and understood by the investors who initially purchased them?

Supporting Data on Redemption Trends:

- Q4 2025 Redemption Surge: Non-traded BDCs saw average redemptions rise to 4.8% of NAV, up from 1.6% in Q3 2025.

- Exceeding Caps: Five BDCs funded tenders above the standard 5% quarterly cap in Q4 2025.

- Fitch Analysis: Sentiment, particularly concerning AI disruption risk for software companies, is identified as the primary driver of elevated redemption requests.

The liquidity and asset coverage cushions within these structures appear sufficient to absorb the current spike in redemptions. While sustained tenders above the 5% cap could eventually pressure credit profiles, this is not Fitch’s base case scenario. For instance, the average debt-to-equity ratio for seven rated perpetually non-traded BDCs stood at a conservative 0.71x, notably lower than the 1.13x for other rated BDCs. Furthermore, asset coverage cushions averaged a robust 38.6%, significantly above the 22% average for Fitch-rated public and private BDCs. These balance sheet metrics do not indicate a sector on the brink of crisis.

Interestingly, Fitch also identifies a potential structural silver lining. If fundraising remains subdued, the intense competition that has compressed spreads and weighed on BDC earnings in recent years could ease, leading to a market rebalancing rather than a crisis.

Credit Quality Under Scrutiny: Concentrated Stress in Specific Sectors

While the redemption narrative often overshadows other factors, the actual credit quality of private credit assets warrants careful and independent examination. There are indeed meaningful pockets of stress, particularly within the software and technology sectors, which constitute an estimated 26% of direct lending portfolios. The accelerating pace of AI development presents genuine challenges to the business models of many Software-as-a-Service (SaaS) companies, which were underwritten on the assumption of predictable, recurring revenue streams.

Beyond technology, highly leveraged healthcare roll-ups and smaller middle-market borrowers, who benefited from an era of historically low interest rates, are now demonstrating strain. The prevalence of covenant-lite structures, which became commonplace during the robust inflow environment of 2021-2024, offers lenders less protection than initially anticipated in identifying and addressing borrower distress early on.

Indicative Stress Indicators:

- "Bad PIK" Interest: As of Q4 2025, 6.4% of private credit loans carried "bad PIK" interest – interest deferred mid-loan due to liquidity strain rather than structured in at origination. This figure is nearly triple that of 2021 levels, suggesting a shadow default rate approaching 6% against a headline default rate of around 2%.

- Covenant-Lite Structures: Approximately 70% of private credit issuance is not covenant-lite, meaning traditional early warning systems for borrower stress are largely absent.

Morgan Stanley has cautioned that direct lending default rates, currently around 5.6%, could rise to 8%, a significant increase from the historical average of 2-2.5%. While this is a notable increase, it is characterized by the firm’s own analysts as "significant but not systemic." Similarly, KBRA’s rated BDC universe showed no rating changes or negative outlook revisions through Q3 2025, with selective downgrades occurring in Q4. The stress is real and concentrated, but it is not indicative of a broad-based deterioration across the entire $2 trillion market.

The distinction between concentrated sector-specific stress and systemic market failure is critical. Stress in software and leveraged healthcare is primarily a reflection of manager selection and underwriting discipline rather than a fundamental flaw in the private credit asset class itself. While AI disruption risk is a tangible concern, its impact is not universal across all private loans and, importantly, does not inherently extend to the entirety of the private credit market.

Structural Risks and Systemic Contagion: A Different Kind of Threat

The invocation of the 2008 Global Financial Crisis (GFC) is a common reflex whenever complex financial structures encounter stress. While understandable, this comparison often proves inaccurate and, in this instance, is misleading. Private credit differs structurally from the GFC landscape. It lacks depositors to run, repo lines to be pulled, or overnight funding markets to freeze. The feedback loops that rendered subprime mortgages systemic – losses embedded in bank balance sheets backstopped by government-insured deposits – do not manifest in the same way within private credit.

However, this does not equate to zero systemic risk. The contagion channels are different but undeniably present. Mark-to-model valuations can mask deterioration until it becomes undeniable, leading to sudden, sharp corrections. The increasing entanglement of insurance companies, which now fund a growing share of private credit, introduces a risk that losses could ultimately impact the retirement savings of policyholders who are unaware of their exposure. These are genuine risks, albeit distinct from those seen in 2008.

A more subtle and less-discussed wrinkle lies within the AI ecosystem itself. The disruption it poses to SaaS companies is built upon circular dependencies that bear a resemblance to the pre-2008 financial system. Major AI players like Microsoft are deeply intertwined with OpenAI, Google and Amazon with Anthropic, and Nvidia underpins a vast majority of AI models in production. Mapping these relationships reveals an interconnected organism rather than a purely competitive technology sector. This structure mirrors the counterparty exposure diagrams prevalent in 2007, where the question shifted from "who has the risk?" to "who doesn’t?" A significant stumble by a key node in this ecosystem could have ripple effects through private credit portfolios exposed to SaaS companies reliant on its stability. The diversification that many investors believe they possess may prove more theoretical than tangible. This requires informed analysis, not a new wave of hysteria, but it also underscores the importance of learning from past mistakes.

Timeline of Key Events and Developments:

- 2015-2025: Outstanding loans to SaaS firms surge from approximately $8 billion to over $500 billion, representing 19% of total direct loans.

- 2021-2024: Inflow frenzy in private credit leads to increased leverage and a prevalence of covenant-lite structures.

- Early 2025: Anthropic unveils new agentic AI tools, sparking investor concerns about AI’s impact on traditional SaaS business models.

- Weeks Following AI Product Launches: Over $10 billion is sought for withdrawal from private credit funds due to fears of over-exposure to software companies.

- Q4 2025: Redemption requests surge in non-traded BDCs, triggering quarterly caps and media scrutiny.

- Late 2025/Early 2026: Blue Owl faces significant redemption requests, leading to proposed restructuring and subsequent legal challenges.

- Q1 2026: Moody’s notes a shift from inflows to outflows for perpetually non-traded BDCs.

The Problem of Conflation: Diluting the Signal of True Distress

The conflation of these distinct issues—redemptions, defaults, and structural risks—into a single crisis narrative poses a significant problem for market understanding and effective risk management. Redemption requests do not directly precipitate defaults. A company’s inability to meet loan obligations is not typically caused by retail investors in a non-traded BDC seeking liquidity.

While the ecosystem is interconnected, and persistent outflows can tighten lending conditions, the chain of causation is long and indirect, not immediate. The media narrative has compressed this chain into an alarming, unified story. This compression has tangible consequences. When every instance of a redemption gate is framed as a systemic crisis, and every gated fund is presented as evidence of a collapsing asset class, the media loses its capacity to accurately signal true distress when it genuinely occurs.

Analysis of Implications:

- Erosion of Trust: The mischaracterization of market dynamics can lead to a loss of investor confidence in private credit, an asset class vital for capital formation and innovation.

- Diminished Analytical Credibility: The industry’s ability to accurately assess and communicate future risks is undermined when current, less severe issues are overblown.

- Misallocation of Resources: Focusing on a manufactured crisis can distract from addressing the real, albeit sector-specific, credit challenges and structural issues within wrappers.

- Investor Education Gap: The current narrative highlights a potential failure in communicating the illiquid nature of private credit investments, particularly to retail investors.

Private credit may not be experiencing a systemic crisis, but it is undoubtedly undergoing a recalibration. This recalibration involves genuine stress in specific sectors, critical structural questions regarding the design of semi-liquid wrappers, and real risks that demand rigorous oversight and honest analysis. What it does not deserve is the breathless conflation that blurs the lines between wrapper problems, sector-specific issues, and genuine systemic threats. The distinction is not merely analytical; it is the difference between informed markets and markets driven by fear.

The industry faces a distribution challenge, an education imperative, and a need for wrapper redesign. While private credit offers access to attractive risk-premia and is a significant engine for new economy innovation, its expansion into the retail channel requires a fundamental re-evaluation of how these products are marketed, structured, and understood by investors. Until the messaging, structures, and investor education are genuinely fit for purpose, it is difficult to argue that these products are serving investors or the broader financial system optimally. The path forward necessitates a return to the drawing board on wrapper design before further expansion into the retail market is pursued.