The Shareholder Rights Group (SRG), represented by General Counsel Sanford Lewis, Associate Counsel Khadija Foda, and Research Associate Tanya Agarwal, has submitted a comprehensive comment letter to the Securities and Exchange Commission (SEC) urging the agency to preserve and enhance the existing disclosure ecosystem, rather than diminish it, as the Division of Corporation Finance undertakes a broad review of Regulation S-K. The SRG’s submission, a detailed response to the SEC’s initiative, argues that reducing disclosure requirements would undermine a vital mechanism for investor protection and corporate accountability.

The SEC’s review, prompted by Chairman Paul Atkins’ assertion that the current disclosure regime often generates "significant volumes of immaterial information," signals a potential move towards streamlining reporting obligations. However, the SRG contends that this perspective overlooks the symbiotic relationship between mandatory SEC disclosures and the dynamic process of shareholder engagement, which frequently brings emerging risks to light.

The Interplay of Shareholder Proposals and Regulation S-K

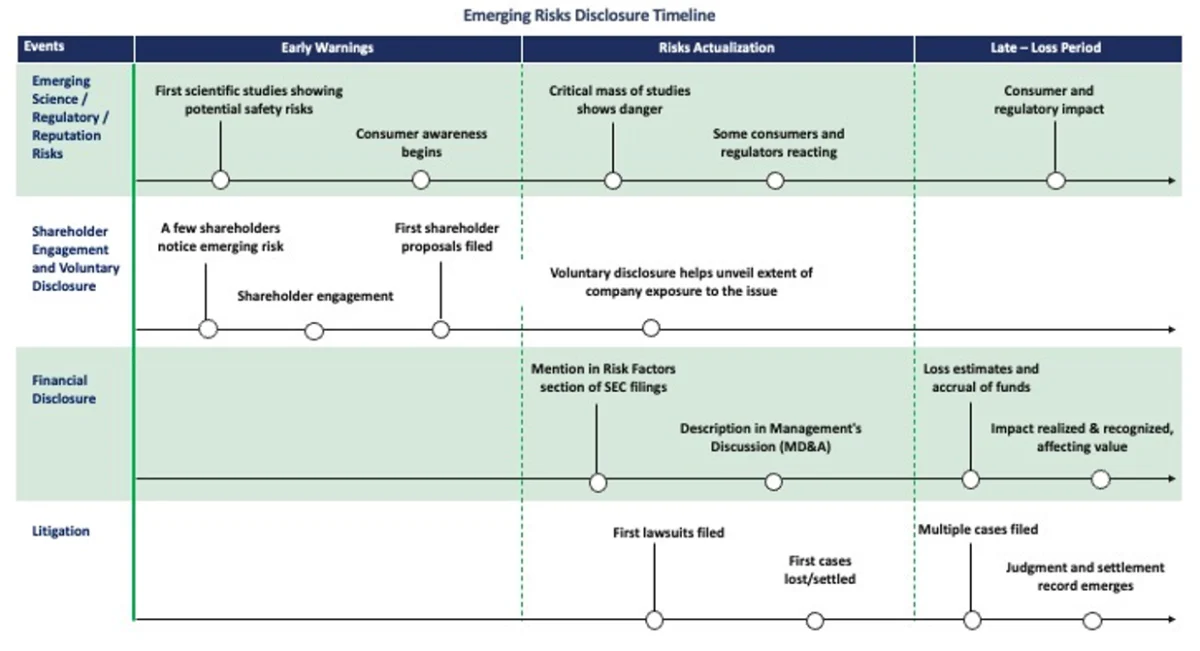

At the core of the SRG’s argument is the concept of a "disclosure ecosystem" where shareholder proposals and Regulation S-K disclosures act in concert. Shareholder engagement, often initiated through the filing of proposals under Rule 14a-8, serves as an early warning system for potential risks. This engagement frequently spurs companies to initiate voluntary reporting, such as sustainability reports. These voluntary disclosures, in turn, can inform and eventually expand the scope of information mandated under Regulation S-K.

The SRG emphasizes that emerging investor concerns about risks, whether environmental, social, or governance-related, are often first identified and amplified through shareholder activism. Companies, driven by incentives to meet market expectations rather than provide a complete risk assessment, may be reluctant to highlight potential negative developments. Financial economist Michael C. Jensen’s observation that corporate reporting can be shaped by the desire to "meet or beat market expectations rather than to present a full account of risk" remains a salient concern. This echoes former SEC Chairman Arthur Levitt’s 1998 warning about the potential for "a game of nods and winks" when earnings expectations dominate corporate communication.

The SEC’s own staff has acknowledged this tendency, reportedly examining whether information disseminated through press releases, conference calls, and other non-filed communications reveals material information omitted from official SEC filings. The SRG asserts that shareholder proposals often catalyze a company’s internal measurement, analysis, and board-level attention to these issues. As companies develop metrics for public disclosure, they naturally scrutinize the underlying concerns more closely. This scrutiny prompts management to assess whether an issue constitutes a material risk requiring disclosure under Regulation S-K and whether existing disclosures are sufficient to qualify for safe harbor protections. While management and shareholders may initially disagree on the significance of a risk, this iterative process of engagement and disclosure refinement helps the market identify and define emerging risks.

Disclosures are crucial for investors actively engaged in stewardship. They enable investors to assess whether management is identifying and actively managing risks that could impact long-term financial performance, evaluate the adequacy of the company’s risk oversight framework relative to its exposure, and determine if further engagement or escalation through the proxy process is warranted. These disclosures also provide a baseline for assessing the need to file shareholder proposals requesting enhanced reporting or management action on identified risks.

Emerging Risks Highlighted by Shareholder Proposals

The SRG’s comment letter provides several compelling examples of how shareholder proposals have effectively surfaced potentially material risks, subsequently influencing corporate disclosures.

Artificial Intelligence and Emerging Risks

The period between 2022 and 2025 has witnessed a significant surge in AI-related shareholder proposals, driven by investor demand for greater transparency regarding the associated risks and opportunities.

In 2025, investors filed proposals at major technology firms like Alphabet and Amazon, seeking increased disclosure on the substantial water and energy demands of AI infrastructure. A similar proposal submitted to Salesforce preceded the company’s launch of a dedicated water program as part of its updated sustainability strategy.

In 2024, shareholders at Meta and Alphabet filed proposals requesting annual reporting on the risks posed by generative AI, including misinformation and broader societal harms. These proposals garnered significant support, with Meta’s receiving 56.3% support from independent shareholders and Alphabet’s securing 45.7% of the independent vote. At Apple, a 2024 proposal seeking greater transparency regarding the company’s AI use and ethical guidelines received 37.5% support of votes cast. These figures underscore a growing investor consensus on the material nature of AI-related risks, even if not yet fully reflected in Regulation S-K disclosures.

Online Child Safety

Faith-based investors co-filed a proposal at Meta in 2024, requesting annual reporting on child safety risks, including cyberbullying and mental health impacts on young users. This proposal achieved 59.1% support from independent shareholders. Similar proposals have been submitted to Alphabet and Apple, reflecting widespread investor concern. The materiality of this risk was underscored in March 2026, when a jury awarded $6 million against Alphabet and Meta in a lawsuit alleging that negligent platform design contributed to a young woman’s social media addiction and subsequent mental health harms. Additional lawsuits with similar allegations are currently pending, demonstrating the tangible financial and reputational consequences of inadequate oversight in this area.

Opioid Crisis Oversight

In 2020, the Illinois State Treasurer co-filed a proposal at Johnson & Johnson to review opioid-related risks. The proposal garnered 60.9% support. Similar proposals were filed at McKesson, AmerisourceBergen, and CVS Health. These proposals presciently identified risks that later proved financially and operationally significant, culminating in the $26 billion opioid legal settlements reached by these companies in 2022. This case exemplifies how shareholder engagement can anticipate and flag material risks that may not be fully captured by existing corporate disclosures.

Worker Safety

In 2022, shareholders at Amazon filed a proposal requesting an independent audit of working conditions, citing injury rates significantly above the national average. The proposal received 44% support. Amazon has since faced a class-action lawsuit concerning its treatment of workers with disabilities and, in 2025, reached a settlement with the U.S. Department of Labor following an OSHA investigation into hazardous working conditions. Similar proposals have been filed at Walmart and other issuers, highlighting investor concern that workplace safety failures can lead to material operational, legal, and reputational risks.

Addressing the "Information Overload" Narrative

The SRG contends that the assertion of "information overload" as a basis for trimming disclosure obligations is a "false narrative" in the current technological landscape. Advanced tools, including Artificial Intelligence, empower investors to efficiently sift through both voluntary and mandatory disclosures to extract relevant information for their investment strategies. This capability diminishes the argument that a high volume of disclosures inherently hinders investor decision-making.

Expanding the Lens of Materiality

Crucially, the SRG proposes that the SEC should broaden the lens for assessing materiality under Regulation S-K. The group argues that substantial shareholder engagement and significant support for shareholder proposals should be recognized as evidence of materiality. This level of investor interest, the SRG posits, demonstrates a significant stake in an issue and should inform the necessity of disclosure under Regulation S-K.

Implications for Corporate Behavior and Disclosure

The SRG’s submission highlights the critical role of shareholder engagement in incentivizing more robust corporate risk management and transparent reporting. By prompting companies to develop metrics and disclose information on emerging risks, the shareholder proposal process fosters a more informed market. This process is particularly vital given the inherent incentives for corporations to manage their public image and financial reporting to meet or exceed market expectations, sometimes at the expense of full and frank disclosure of potential risks.

The SRG acknowledges that the SEC has faced pressure to reconsider rules governing environmental and social shareholder proposals, referencing the December 2025 White House executive order on ESG and DEI. However, the group firmly maintains that the shareholder proposal process is a principal mechanism for investors to communicate information needs and emerging risk concerns. Constraining the scope of Rule 14a-8 proposals to exclude environmental or social issues, which frequently manifest as material risks, would significantly harm the market by disrupting established channels for improved disclosure and weakening the broader disclosure ecosystem that includes Regulation S-K.

Recommendations for Strengthening the Disclosure Framework

Beyond urging the preservation of the current disclosure ecosystem, the SRG advocates for strengthening and clarifying the relationship between Rule 14a-8 and Regulation S-K. Specifically, the SRG suggests that the SEC could clarify that substantial support for a shareholder proposal (e.g., above 20% voting support) may constitute evidence of materiality for the related issue under Regulation S-K.

Furthermore, the SRG proposes that while voluntary sustainability reports and other ESG-specific disclosures do not substitute for mandatory Regulation S-K risk factor disclosures, it can be appropriate for voluntarily reported ESG information, even if not in a highly formalized format, to be included in SEC-mandated filings. This would streamline reporting and encourage the integration of valuable ESG data into official disclosures.

The SRG’s comprehensive comment letter, available on the SEC’s website, provides a detailed analysis of these issues and underscores the critical need for the SEC to recognize and bolster the integrated framework of shareholder engagement and regulatory disclosure in safeguarding investor interests and promoting robust corporate governance. The agency’s response to these arguments will have significant implications for the future of corporate transparency and accountability.