The collective net worth of the 17 largest U.S. university endowments experienced a substantial surge, escalating from approximately $249 billion in fiscal year 2016 to $426 billion by fiscal year 2025. This remarkable growth, representing an increase of roughly 70-73% depending on rounding, is a testament to a dual engine of robust investment performance and consistent new gift contributions. However, beneath this aggregate financial success lies a more intricate narrative, one defined by three distinct allocation philosophies, markedly different risk profiles, and a discernible structural gap when these endowments are juxtaposed against their global institutional counterparts. This comprehensive analysis draws upon the authoritative 2025 NACUBO-Commonfund Study of Endowments, individual fund annual reports, and sophisticated multi-factor statistical risk model outputs from FIS-APT to illuminate what the investment strategies of these top 17 endowments reveal about asset allocation, risk management, and overall efficiency in the institutional investment landscape.

A Decade of Growth: Strong Returns and Shifting Leadership

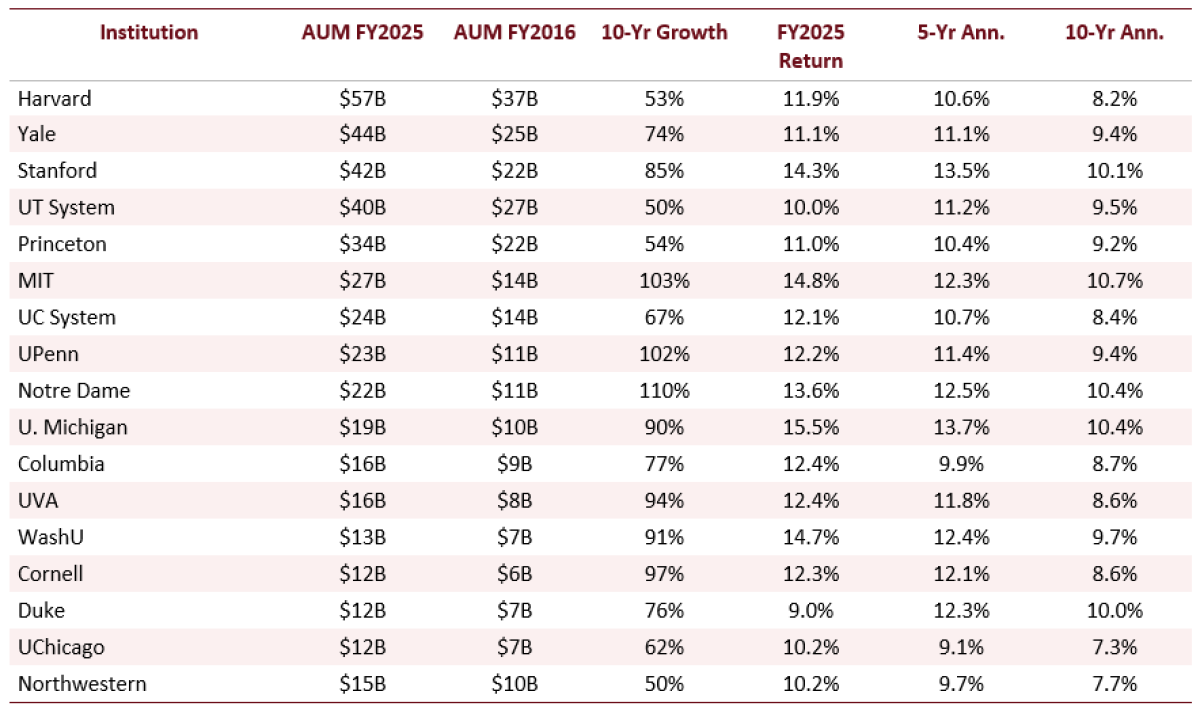

Over the past decade, the aggregate Assets Under Management (AUM) for this elite group of university endowments has seen a significant expansion, growing from roughly $247 billion in FY2016 to approximately $426 billion by FY2025. This impressive 70-73% gain is a product of both astute investment returns and substantial net new gifts. A closer examination of individual institution performance, as detailed in Table 1, reveals a dynamic landscape of returns. For FY2025, the University of Michigan led the pack with an exceptional net return of 15.5%, closely followed by the Massachusetts Institute of Technology (MIT) at 14.8%, Washington University in St. Louis (WashU) at 14.7%, and Stanford University at 14.3%.

Looking at longer-term horizons, the picture becomes more nuanced. Over a five-year period, Michigan, Stanford, the University of Notre Dame, WashU, and MIT have all consistently surpassed 12% in annualized returns. When extending the timeframe to a decade, MIT, Michigan, Stanford, Notre Dame, and Duke University emerge as the top performers. Notably, Harvard University, despite holding the largest AUM at $57 billion, posted a ten-year return of 8.2%, placing it at the lower end among the top five by asset size. This divergence highlights a critical insight: the institutions that achieve the highest one-year returns are not invariably the strongest long-term compounders. The sustained, disciplined growth over multiple market cycles often dictates the true measure of long-term investment success.

Table 1. AUM Growth and Net Returns: Top 17 Endowments (FY2016-FY2025)

(Image of Table 1 showcasing AUM growth and net returns for the top 17 endowments from FY2016 to FY2025. This table would detail individual endowment figures for each year, including starting and ending AUM, and net investment returns. The accompanying note clarifies that figures are net of investment management fees, exclude distributions and operating expenses, and that AUM growth reflects both investment returns and net new gifts, with some estimates included for undisclosed figures.)

Three Distinct Philosophies Shaping Endowment Portfolios

The investment strategies employed by the largest U.S. university endowments are far from monolithic. A review of their asset allocations reveals three prominent philosophical approaches, best exemplified by Harvard, Yale, and Michigan. These institutions, each with unique objectives and risk tolerances, offer a window into the diverse paths leading to endowment growth.

Harvard: The Concentration Model

Harvard University’s endowment, the largest among the group at $57 billion, exemplifies a "concentration model." Its portfolio is heavily weighted towards private equity (41%) and hedge funds (31%), with no dedicated venture capital allocation. This strategy embraces significant illiquidity and manager concentration, seeking to capture the premium returns associated with private markets. While Harvard has demonstrated strong recent one-year performance, its ten-year annualized return of 8.2% reflects the headwinds and potential costs associated with its earlier strategic transition periods and the inherent risks of concentrated alternative investments.

Yale: The Diversified Alternatives Model

The Yale University endowment is widely recognized as the progenitor of the "diversified alternatives model," a framework that has profoundly influenced the industry’s approach to endowment portfolio construction. Yale’s allocation reflects a broad diversification within alternatives, with 24% in venture capital, 20% in private equity, and 22% in hedge funds. This disciplined approach, pioneered by the late David Swensen, has become a benchmark against which other institutional investors are measured. Yale’s consistent performance, with an 11.1% one-year return and a 9.4% ten-year annualized return, underscores the power of broad diversification in achieving sustained compounding over extended periods.

Michigan: The Growth-Concentrated Model

The University of Michigan’s endowment stands out for its exceptional performance in FY2025, achieving a 15.5% net return. This success is largely attributed to a "growth-concentrated model" with a significant weighting in venture capital (33%) and private equity (11%), complemented by allocations to hedge funds (13%) and real assets (13%). Michigan’s strong track record, evidenced by its 13.7% five-year and 10.4% ten-year annualized returns, suggests that this strategic posture is durable and has been built to withstand multiple market cycles, rather than being a fleeting outcome driven by short-term market trends, such as those influenced by AI-related public market valuations.

Table 2. Three Endowment Case Studies: Harvard, Yale, and Michigan (FY2025 Standardized Allocation Categories)

(Image of Table 2 presenting a standardized comparison of asset allocations for Harvard, Yale, and Michigan in FY2025. The table would detail percentage allocations across categories like Private Equity, Venture Capital, Hedge Funds, Real Assets, and Public Equities for each institution. The note emphasizes that categories are mapped for comparability and may differ from exact public reporting labels, and that rounding and mapping may cause rows to not sum precisely to 100%.)

The Nuances of Diversification: Real Assets and Hedge Funds

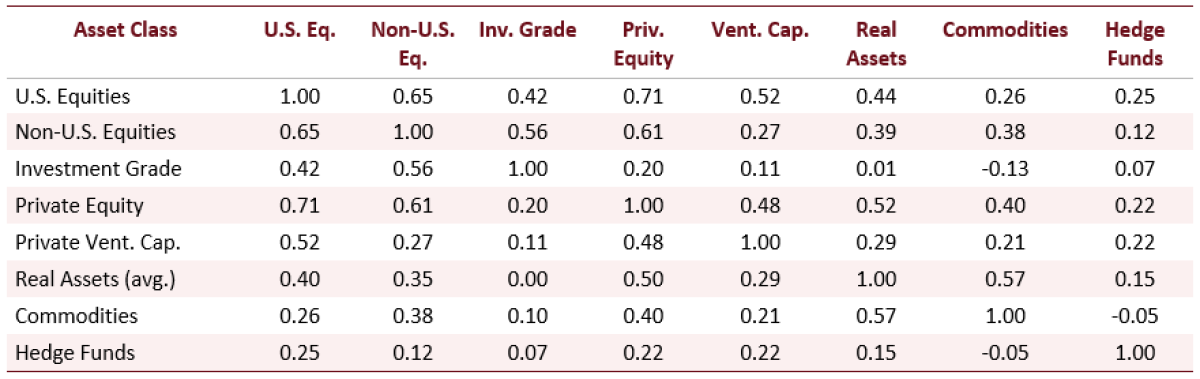

While the broad diversification into alternative assets is a common theme among leading endowments, the impact of these diversifiers on risk reduction is not uniform. An examination of ex-ante correlation estimates from the APT model reveals critical distinctions. Private equity, for instance, exhibits a 0.71 correlation with U.S. equities and venture capital a 0.52 correlation, indicating that both asset classes retain significant equity beta. Similarly, real estate and private energy investments often carry comparable equity exposures.

In contrast, hedge funds, as modeled by the Global HFR Index, demonstrate considerably lower correlations with traditional equity markets: 0.25 with U.S. equities and a mere 0.12 with non-U.S. equities. Commodities, another alternative asset class, show a negative correlation of -0.05 with hedge funds. This divergence is a crucial insight: despite allocating over 60% to alternatives, 86% of the ex-ante volatility across large endowments still originates from the equity factor. This suggests that endowments have not necessarily eliminated equity risk but have, in many cases, shifted it towards manager selection, market timing, and the embrace of illiquidity.

Table 3. Selected APT Correlation Estimates Across Asset Classes (APT Model)

(Image of Table 3 displaying selected ex-ante correlation estimates between various asset classes derived from the APT model. This table would likely show correlation coefficients for pairings such as U.S. Equities vs. Private Equity, U.S. Equities vs. Hedge Funds, Private Equity vs. Venture Capital, etc. The note clarifies that "Real Assets" is an approximate composite, and thus pairwise values are selected estimates rather than a complete symmetric matrix, with full output available elsewhere.)

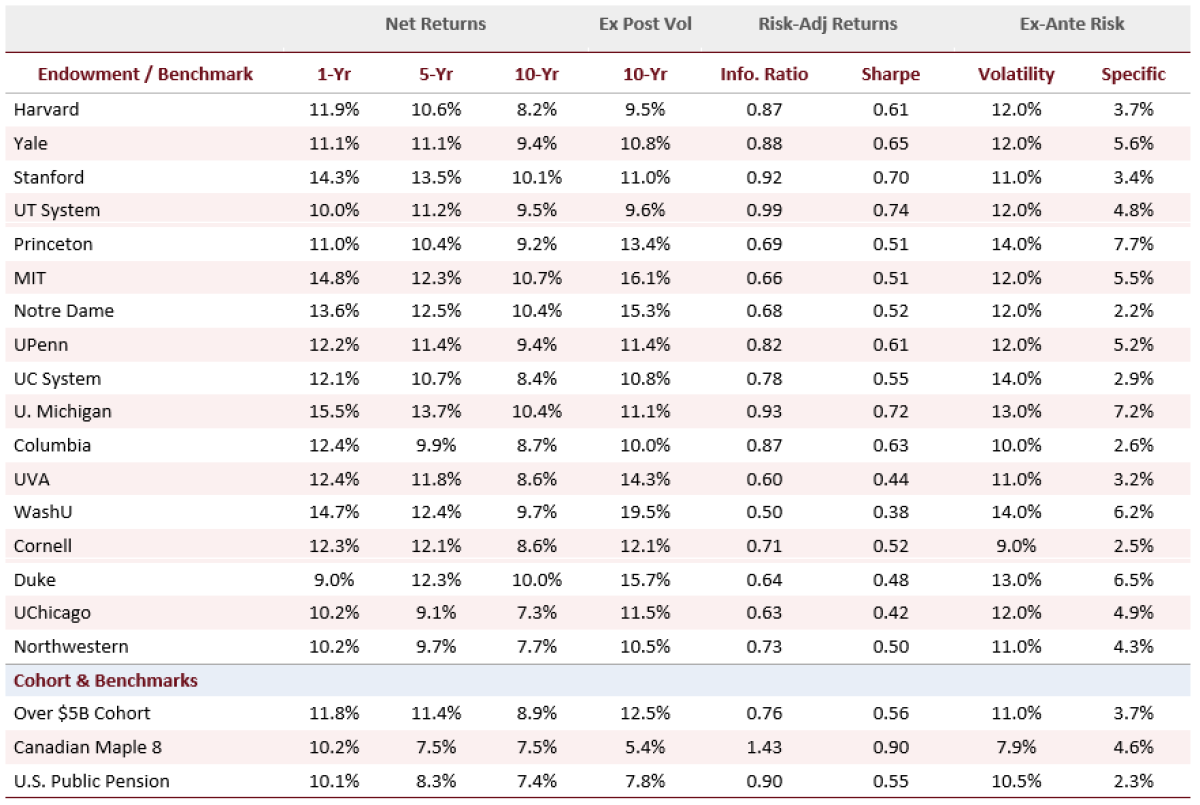

Risk Profiles: Higher Returns, But Often Lower Risk-Adjusted Efficiency

A comprehensive analysis of the APT risk model output, presented in Table 4, reveals that while the largest 17 U.S. endowments (the Over $5B cohort) have outperformed U.S. and Canadian pension peers over one, five, and ten-year horizons (averaging 12%, 11%, and 9% respectively), this outperformance often comes with higher ex-ante risk—approximately 11%—and potentially greater losses, around 20% in a 1-in-20-year event. Consequently, their risk-adjusted returns, as measured by Sharpe and Information Ratios, are notably lower. The Over $5B cohort exhibits Sharpe Ratios of 0.56 and Information Ratios of 0.76, significantly trailing the Canadian Maple 8 benchmark, which achieves ratios of 0.90 and 1.43, respectively.

The range of Sharpe Ratios among the 17 endowments spans from 0.38 for WashU to 0.74 for the University of Texas System. WashU’s high ex-post volatility over ten years (19.5%) explains its relatively low Sharpe Ratio (0.38) despite a competitive 9.7% ten-year return. Conversely, Cornell University and Columbia University demonstrate the lowest ex-ante volatility within the individual endowment group (9.1% and 9.6%, respectively) and achieve above-average Sharpe Ratios, even with lower headline returns compared to some peers. The Maple 8’s superior Information Ratio of 1.43 compared to the Over $5B cohort’s 0.76 is a stark numerical representation of this efficiency gap, suggesting a more effective translation of risk into return.

Table 4. Ex-Ante Risk, Net Returns, and Risk-Adjusted Performance by Endowment Plan (APT Model Output)

(Image of Table 4 providing detailed APT model output for each endowment plan and benchmark. This table would include metrics such as Ex-Ante Volatility, Net Returns (1-yr, 5-yr, 10-yr), Sharpe Ratio, Information Ratio, and potentially systematic and specific risk components. The note specifies the data sources and the risk-free rate used for Sharpe Ratio calculations.)

Stress Tests: Unveiling the Dominance of Equity Risk

The true resilience of investment portfolios is often revealed under stress. Table 5 presents the outcomes of stress tests and factor attribution for each institution and benchmark, underscoring a persistent theme: 86% of ex-ante volatility across large endowments is still driven by equity factor risk. This inherent exposure leads to significant losses during severe market downturns.

During the COVID-19 pandemic (March-April 2020), most endowments experienced losses ranging from 21% to 27%, a testament to the pervasive equity beta that even alternative allocations could not fully mitigate during this rapid, global liquidity event. However, in a scenario mimicking the early 2022 inflationary environment, endowments generally fared better than their pension peers. The Over $5B cohort lost approximately 8%, whereas benchmark portfolios saw losses between 22% and 25%. This resilience in inflationary periods is attributed to the partial inflation hedging provided by real assets and certain hedge fund strategies.

Several specific findings emerge from these stress tests:

- Notre Dame’s Equity Dominance: The University of Notre Dame exhibits a striking 96% equity factor attribution, resulting in a substantial -18.1% loss during the stagflation scenario. This reflects its public-equity-heavy investment posture.

- Duke’s Inflation Hedge: Duke University’s 11.7% allocation to commodities, the highest among its peers, contributed to a comparatively smaller -4.3% loss during the stagflation period. Its exposure to real assets and natural resources proved to be a meaningful inflation hedge.

- Maple 8’s Fixed Income Exposure: The Canadian Maple 8’s 7.0% duration factor attribution, significantly higher than most endowments, stems from its greater reliance on fixed income. While this strategy contributed to lower overall volatility, it resulted in a -10.0% loss during stagflation, a performance worse than many endowments despite its lower volatility profile.

The UC System and Notre Dame experienced the largest stagflation losses among endowments (-15.7% and -18.1%, respectively), directly attributable to their high equity factor concentrations (97.8% and 96.0%). The U.S. Public Pension benchmark also faced a significant stagflation loss of -18.8%, a consequence of its mandatory fixed income allocations, which incurred mark-to-market losses during a sharp rise in interest rates.

Table 5. Potential Losses and Factor Risk Attribution by Endowment Plan (APT Model Output)

(Image of Table 5 detailing potential losses and factor risk attribution for each endowment plan and benchmark. This table would include metrics like Value at Risk (VaR), Average Loss (1-in-20-year), Maximum Drawdown Horizon, and factor attribution percentages for key risk factors (e.g., Equity, Interest Rate, Commodities). Stress test scenarios like Financial Crisis, COVID, and Stagflation would be detailed. The note clarifies omitted factors and the nature of scenario-based estimates.)

Key Insights for Investment Professionals

The analysis of these top U.S. university endowments offers several critical takeaways for investment professionals seeking to optimize portfolio construction and risk management:

-

Raw Returns Require Volatility Adjustment: When comparing investment performance, raw returns alone can be misleading. For instance, WashU’s ten-year return of 9.7% appears comparable to Cornell’s 8.6%. However, WashU’s ex-ante volatility of 14.1% dwarfs Cornell’s 9.1%. On a risk-adjusted basis (Sharpe Ratio), Cornell’s more disciplined approach yields a demonstrably more efficient outcome for the level of risk undertaken. Table 4 effectively illustrates this crucial comparison across all 17 institutions.

-

Factor Attribution Explains Stress-Test Outcomes: Understanding factor attribution provides a more accurate explanation of performance during stress events than simple allocation labels. Institutions with similar allocations to alternatives can exhibit vastly different equity factor shares, and it is this equity share that predominantly drives losses during market crises like the Financial Crisis and the COVID-19 pandemic. In stagflationary environments, exposures to real assets and commodities—specifically in energy, natural resources, and infrastructure—have proven to be key differentiators in performance.

-

The Maple 8 Approach: Structural Divergence: The investment strategies employed by the Canadian Maple 8 are not merely a matter of strategic preference but represent a fundamentally different structural approach. While U.S. endowments primarily utilize real assets and hedge funds to diversify away from equity markets, the Maple 8 leverages debt, repurchase agreements, and derivatives markets to achieve diversification, particularly through fixed income. Both methodologies enhance risk-adjusted returns relative to traditional portfolios, but they employ distinct mechanisms with differing risk profiles. The Maple 8’s superior Sharpe and Information Ratios suggest that U.S. endowments could potentially improve their efficiency by adopting balance sheet leverage and direct investment infrastructure, although such strategies may encounter governance challenges within current U.S. institutional frameworks.

In conclusion, the landscape of U.S. university endowments is characterized by a dynamic interplay of aggressive growth strategies, diverse risk appetites, and a continuous search for alpha. While substantial gains have been achieved, a deeper analysis reveals persistent challenges in optimizing risk-adjusted returns when benchmarked against sophisticated global peers. The insights gleaned from allocation philosophies, correlation analyses, and stress-testing underscore the enduring importance of a nuanced understanding of risk factors and the potential benefits of structural approaches that may differ from current industry norms.