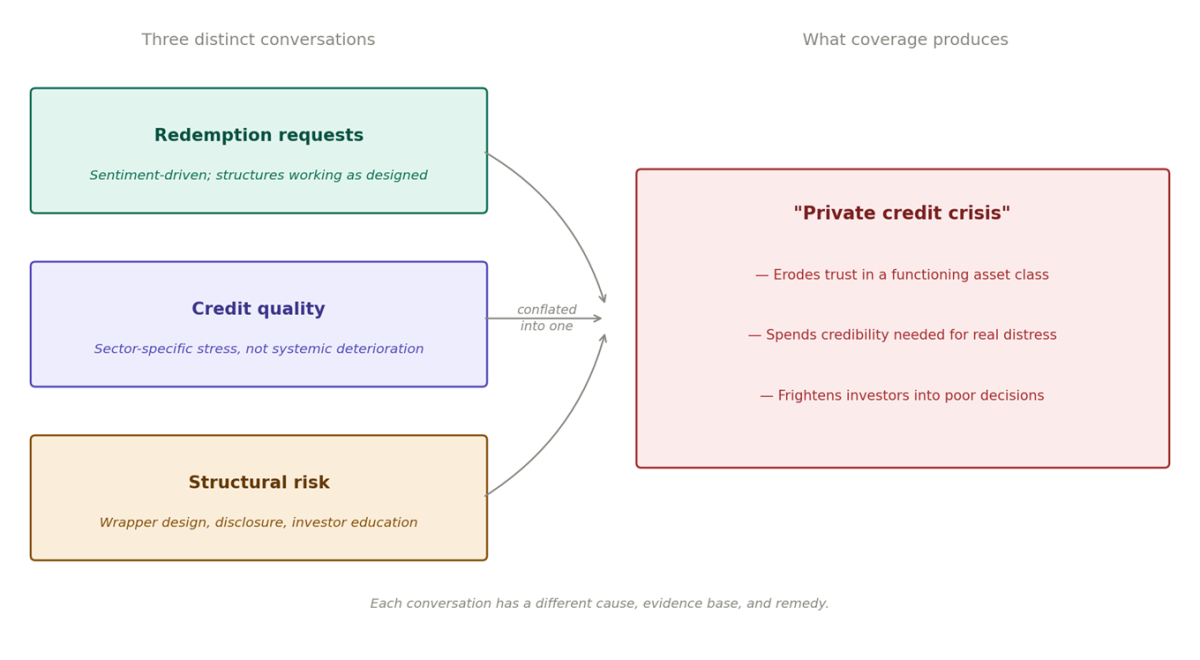

The narrative surrounding the $2.02 trillion private credit market has been dominated by alarmist headlines, painting a picture of impending collapse or a grim rehash of the 2008 financial crisis. However, a closer examination of the data reveals a more nuanced reality, where distinct issues are being conflated into a single, misleading crisis narrative. This conflation risks eroding trust in a vital asset class and diminishes the industry’s analytical credibility when genuine challenges arise. To understand the current landscape, it is crucial to disentangle three separate conversations: redemption requests, credit quality, and structural risks.

The Surge in Redemption Requests: Sentiment Over Substance

A significant driver of the current market anxiety stems from increased redemption requests from retail investors in non-traded Business Development Companies (BDCs) and semi-liquid vehicles. These requests have triggered quarterly caps, leading to the imposition of "gates" and capital lock-ups. While media coverage has often presented this as evidence of a collapsing asset class, a deeper dive into the mechanics is warranted.

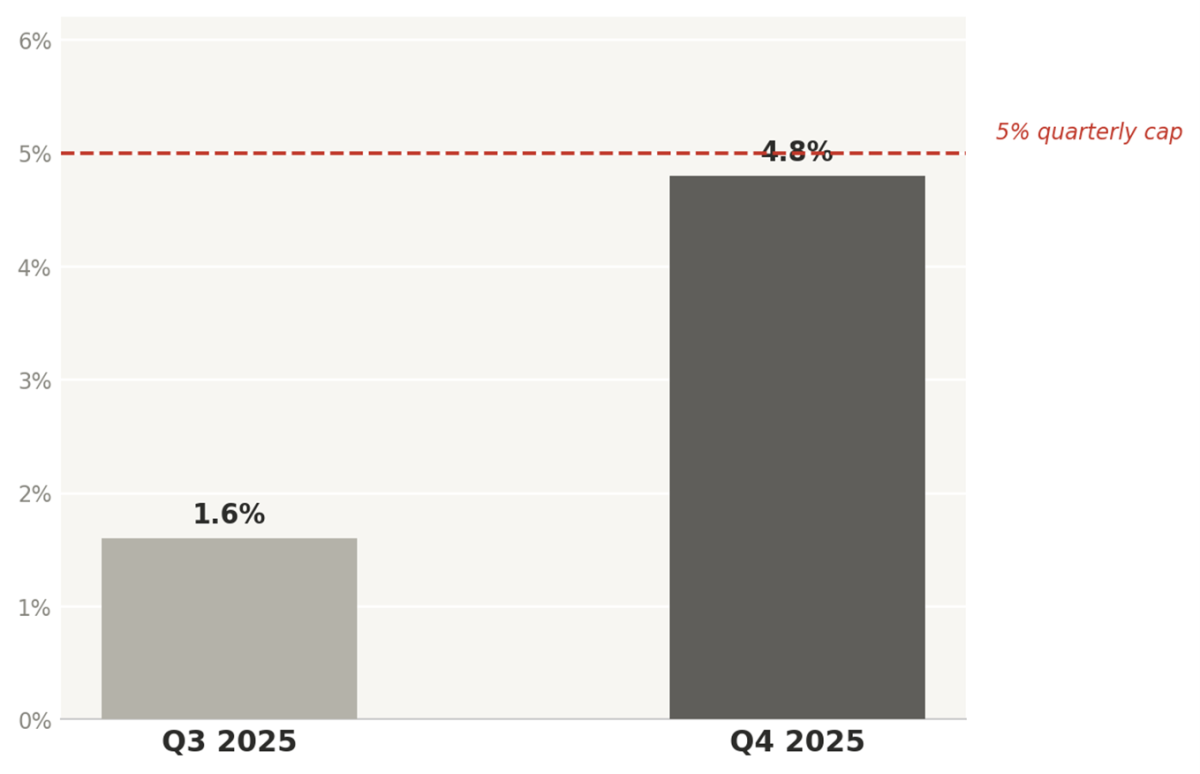

Actual redemptions, representing capital returned to investors, are capped at 5% of Net Asset Value (NAV) per quarter by design. What has surged is not the capital returned, but the volume of redemption requests. This distinction is critical. A spike in requests signals shifts in investor sentiment, not necessarily a deterioration in underlying credit quality.

In the fourth quarter of 2025, average redemptions for perpetually non-traded BDCs rose to 4.8% of NAV, a substantial increase from 1.6% in the third quarter. Five BDCs even funded tenders exceeding the standard 5% quarterly cap. This surge, amplified by media coverage, has been characterized as hysteria. Fitch analysts suggest that these redemption requests are largely sentiment-driven, with concerns often stemming from investor anxieties about the impact of Artificial Intelligence (AI) on software companies. This has led to elevated requests and slower inflows, which, while concerning from a narrative perspective, do not yet represent a broad-based judgment on the quality of private credit portfolios.

The structures in place are functioning as intended. The 5% quarterly cap is not a crisis-induced gate but a pre-existing feature designed to protect the integrity of the loan book, underwriting discipline, and the return profile for remaining investors. Managers adhering to this cap are not signaling distress but are instead managing a significant oversubscription of redemption requests. This situation highlights a potential "elephant in the room": whether the long-term, illiquid nature of these vehicles was adequately understood by investors at the time of purchase.

Crucially, liquidity and asset coverage cushions appear sufficient to absorb spikes in elevated redemptions. While sustained tenders above the 5% cap could pressure credit profiles, this is not Fitch’s base case scenario. The average debt-to-equity ratio for seven rated perpetually non-traded BDCs stood at 0.71x, significantly lower than the 1.13x for other rated BDCs. Asset coverage cushions averaged 38.6%, well above the 22% average for Fitch-rated public and private BDCs. These balance sheet metrics do not suggest a sector on the brink of crisis.

In fact, Fitch identifies a potential structural silver lining: if fundraising remains weak, the competitive pressure that has compressed spreads and weighed on BDC earnings could ease, signaling a rebalancing rather than a crisis.

Moody’s has noted a shift from inflows to outflows for perpetually non-traded BDCs in Q1 2026. Publicly traded BDCs, having maximized leverage, have less room for error. A significant contributor to the current market stress is the concentration of software within BDC portfolios. Moody’s found that software represents approximately 25% of BDC portfolios on a median basis and flagged AI as a developing credit risk. However, their assessment offers a balanced perspective: "Asset quality metrics have so far remained largely benign, and software loan maturities do not increase more meaningfully until 2028-2029, suggesting AI risk will be a sentiment and monitoring issue in the near term rather than an immediate ratings driver."

The Software Sector and the AI Disruption

The deep involvement of private credit in the software sector is a key part of the current narrative. Loans to Software-as-a-Service (SaaS) firms have grown exponentially, from nearly $8 billion in 2015 to over $500 billion by the end of 2025, representing 19% of total direct loans. This growth was fueled by the appeal of SaaS companies to private credit lenders, offering predictable recurring revenue, sticky customer bases, high margins, and scalability. By 2023, direct lenders captured a record 54% of large leveraged buyout (LBO) financing, a significant shift from the pre-pandemic era when syndicated loan markets dominated.

The proximate trigger for the recent surge in redemption requests appears to be the unveiling of new agentic AI tools by companies like Anthropic. These tools are designed to perform complex professional tasks, potentially disrupting the business models of existing SaaS companies that currently charge for such services. This sparked a sell-off in software data provider shares and raised fresh concerns about the vulnerability of traditional SaaS business models. Within weeks of these AI product launches, investors sought to withdraw over $10 billion from private credit funds, driven by fears of over-exposure to software companies perceived as vulnerable.

The underlying issue is not necessarily the software exposure itself but the opacity surrounding private credit loans. These loans are often held at par, and borrowers do not publicly disclose earnings. Deteriorations in a borrower’s business model may not surface in stated valuations until a covenant breach or maturity event forces disclosure, by which time options may be significantly narrowed.

Stress Indicators and Covenant Structures

While broad-based deterioration is not evident, existing stress indicators warrant careful examination. As of Q4 2025, 6.4% of private credit loans carried "bad PIK" (Payment-In-Kind) interest, meaning interest deferred due to liquidity strain rather than structured in at origination. This is nearly triple the levels seen in 2021. Lincoln International considers this a shadow default rate, suggesting implied distress closer to 6% against a headline rate of around 2%.

Furthermore, approximately 70% of private credit issuance is not covenant-lite, meaning that early warning systems that once flagged borrower stress before a missed payment are largely absent. This lack of transparency leaves investors uncertain about the true value of their holdings. In such an environment, rational retail investors with quarterly redemption windows may choose to exit before potential issues become clearer.

Blue Owl: A Case Study in Wrapper and Disclosure Issues

Blue Owl became a prominent casualty of the redemption request wave, with investors seeking to withdraw significant portions of their holdings from its technology-focused vehicles and credit income funds. These requests were largely driven by sentiment and fears surrounding the software sector, rather than by any meaningful deterioration in the underlying loan portfolios, which had performed in line with the Cliffwater Direct Lending Index with minimal non-accruals.

The company’s attempt to address a liquidity mismatch involved merging one of its vehicles into its publicly traded BDC. However, the proposed terms, which would have imposed a roughly 20% haircut on investors due to the BDC’s discount to NAV, triggered a class-action lawsuit and significant media attention. Allegations included the firm having repeatedly assured investors of no "meaningful pressure" on redemptions while withdrawals were accelerating.

The timing proved particularly unfortunate. The merger was terminated, redemption mechanics were restructured to eliminate quarterly tender offers entirely, and Moody’s revised its outlook to negative. However, Moody’s simultaneously noted that asset quality remained solid, underscoring that the issues were with the "wrapper" (the investment vehicle structure) and disclosure, rather than the credit itself.

Investors were not redeeming because the assets were failing, but because they were frightened by negative coverage that, ironically, was citing their redemption requests as proof of a crisis. They were also motivated by the perception that "semi-liquid" offered greater accessibility than the quarterly cap mechanics actually allowed.

This situation raises a more fundamental question about investor psychology and its interplay with market participants. Investor sentiment is shaped by conversations with fund managers, advisors, and intermediaries. When redemption requests massively oversubscribe the stated liquidity features of a vehicle designed for long-term illiquidity, it prompts an inquiry into whether the vehicle’s fundamental nature was adequately conveyed, understood, or perhaps disregarded amidst prevailing market exuberance.

The language used to describe these products also warrants scrutiny. "Semi-liquid" implies a degree of accessibility that the underlying mechanics may not consistently support. More fundamentally, the feasibility of structures that offer periodic withdrawal capabilities from inherently illiquid assets, pursued at the scale seen in the industry, is being challenged. While retail investors deserve access to private market opportunities, particularly given their role in capital formation and innovation, the current messaging, structures, and investor education may not be sufficiently robust. The industry may need to reconsider its wrapper design before further expanding into the retail channel. This situation is a complex interplay of distribution, education, and wrapper design challenges, rather than a fundamental credit crisis—at least for now.

Credit Quality: Pockets of Stress, Not Systemic Collapse

Credit quality is a separate conversation that requires objective assessment. There are indeed meaningful pockets of stress within the private credit market. The software and tech sector, estimated to represent around 26% of direct lending portfolios, is under pressure due to AI disruption, which poses real questions for SaaS business models underwritten for predictable recurring revenue. Highly leveraged healthcare roll-ups and smaller middle-market borrowers, priced for an era of low interest rates, are also showing strain. The prevalence of covenant-lite structures, common during the 2021-2024 inflow frenzy, offers less protection than lenders may have assumed.

Morgan Stanley has warned that direct lending default rates, currently around 5.6%, could reach 8%, a significant increase from the historical average of 2-2.5%. While this warrants attention, Morgan Stanley’s own analysts characterized an 8% default rate as "significant but not systemic." KBRA’s rated BDC universe showed no rating changes or negative outlook revisions through Q3 2025, though selective downgrades followed in Q4. The stress is real and concentrated, particularly in sectors like software and leveraged healthcare, but it does not represent a broad-based deterioration across the entire $2 trillion market.

This distinction is crucial. Concentrated credit stress in specific sectors is primarily a problem of manager selection and underwriting discipline, not an indictment of the entire private credit asset class. While AI disruption risk is real and interconnected with the broader ecosystem, it does not impact all private loans uniformly.

Systemic Risk: A Different Landscape Than 2008

Comparisons to the 2008 Global Financial Crisis (GFC) are frequently invoked whenever complex financial structures exhibit stress. While understandable, these comparisons are often inaccurate and misleading in the current context. Private credit is structurally different from the GFC landscape. It lacks the depositor runs, repo line freezes, and overnight funding market collapses that characterized 2008. The feedback loop of subprime mortgage losses embedded in bank balance sheets, backstopped by government-insured deposits, does not exist in the same form.

However, this does not imply zero systemic risk. Contagion channels, while different, are still present. Mark-to-model valuations can obscure deterioration until it becomes undeniable. The increasing entanglement of insurance companies in funding private credit means that losses could ultimately impact the retirement savings of policyholders who are unaware of their exposure. These are real risks, though distinct from those of 2008.

A less-discussed wrinkle is the interconnectedness of the AI ecosystem itself. The AI disruption impacting SaaS is built on circular dependencies that bear a resemblance to the pre-2008 financial system. Major AI players like Microsoft, OpenAI, Google, Amazon, Anthropic, and Nvidia are deeply intertwined through capital flows, infrastructure reliance, and strategic partnerships. Mapping these relationships reveals an ecosystem that functions more like a single organism than a competitive technology sector. This structure mirrors the counterparty exposure diagrams seen in 2007, where the question shifted from "who has the risk?" to "who doesn’t?" A significant stumble in one key node could reverberate through private credit portfolios exposed to SaaS companies whose revenue streams depend on the stability of this ecosystem. The diversification many investors believe they possess may be more theoretical than real. Understanding these connections is vital for informed analysis, not to incite a new wave of hysteria, but to learn from past mistakes.

The Problem of Conflation

The conflation of redemption requests, credit quality, and systemic risk is itself the core problem. Redemption requests do not directly cause defaults. A company does not fail on its loan obligations simply because retail investors in a non-traded BDC sought liquidity.

While the ecosystem is interconnected—persistent outflows can tighten lending conditions at the margins, indirectly impacting companies reliant on private credit—the chain of causation is long and indirect, not immediate. The media narrative has compressed this complex chain into a single, alarming story. This compression has significant consequences. When every instance of a redemption gate is framed as a systemic crisis, and every gated fund is presented as evidence of a collapsing asset class, the media’s ability to signal genuine distress when it actually occurs is diminished.

Private credit may not be in a crisis, but it is certainly undergoing a recalibration. This recalibration involves real stress in specific sectors, genuine structural questions about the design of semi-liquid wrappers, and real risks that demand rigorous oversight and honest analysis. What it does not deserve is the breathless conflation that obscures the difference between a wrapper problem, a sector-specific issue, and a systemic one. The distinction is analytically important and marks the difference between informed markets and frightened ones.

This situation aligns with broader shifts being tracked in CAIA’s latest report, "The World Rewired," which explores key ideas and their interconnectedness in the evolving investment landscape.