Despite ongoing volatility in the global landscape, U.S. manufacturing leaders are expressing a renewed sense of optimism regarding the year ahead, as indicated by the latest Chief Executive CEO Confidence Index Survey. While current business conditions remain tempered by a confluence of international conflicts, price fluctuations, regulatory shifts, and inflationary pressures, the outlook for the next twelve months has seen a moderate improvement. This subtle but significant shift suggests a growing conviction among manufacturers that the current headwinds will abate, paving the way for more favorable operating environments.

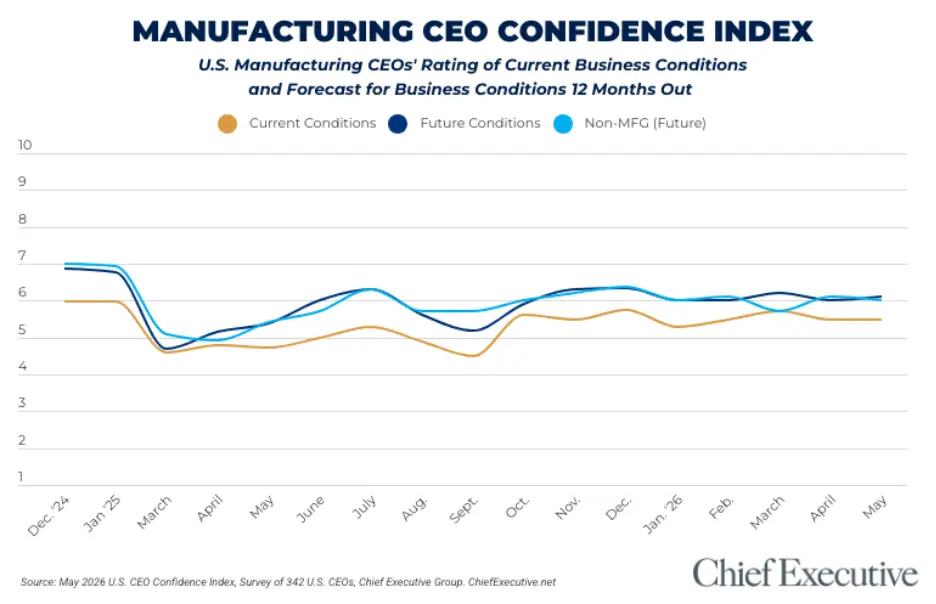

The survey, conducted from May 5-6 among 342 U.S. CEOs, reveals that manufacturers rated current business conditions at a 5.5 out of 10, a score that has remained relatively stable since February 2026. This period coincided with an intensification of geopolitical tensions in the Middle East and a heightened awareness of their impact on global supply chains, a critical concern for the manufacturing sector. While this rating signifies a challenging present, it represents an improvement compared to the sentiment observed for much of the preceding year.

A more encouraging trend emerges when examining year-ahead projections. Manufacturers anticipate an uplift in business conditions, forecasting a rise to 6.0 out of 10 by this time next year. This represents a 2 percent increase from April’s figures and signifies a palpable turn towards optimism, with 52 percent of U.S. manufacturers sharing this positive outlook. This recovery in sentiment is particularly noteworthy, as it follows a 3 percent dip in the Index during the previous month, underscoring the resilience of manufacturing leadership in the face of evolving economic and geopolitical landscapes.

A Divergent Outlook from Broader CEO Sentiment

Interestingly, the sentiment within the manufacturing sector is diverging from that of the broader CEO population polled in May. While overall ratings of current conditions for all CEOs saw a slight improvement, their future forecasts declined by 1 percent compared to April. This suggests a more cautious "wait and see" approach adopted by a larger segment of the CEO community across various industries. Manufacturers, in contrast, appear more inclined to project a more positive trajectory, driven by specific sectorial improvements and an expectation of broader geopolitical and economic stabilization.

Drivers of Manufacturing Optimism

Several factors are contributing to this more optimistic manufacturing outlook. A key driver is the perceived improvement in demand, particularly within the technology and consumer products sub-sectors. These areas, often at the forefront of economic trends, are signaling a resurgence that bodes well for manufacturing output. Furthermore, there is a growing belief among manufacturers that the current period of volatility will resolve before the end of 2027, a projection that underpins their confidence in future growth.

Randy Colwell, CEO of Holloway America, a mid-sized industrial manufacturer, encapsulates this dual perspective. He notes, "Right now, our market is strong, and material costs are steady, but higher interest rates and fuel costs may worsen the market. Especially if the war in Iran slows, we see good growth in the next 12 months." Colwell’s statement highlights the delicate balance between current operational strengths and anticipated external pressures, with a clear acknowledgment that de-escalation of international conflicts could significantly bolster growth prospects.

Echoing this sentiment, Art Hamilton, president of Hamilton International, a mid-sized industrial fabrics manufacturer, expressed his optimism by stating, "I believe the interest rates will be lower in the year ahead. Also, the tariff refund will drive growth." Hamilton’s perspective points to the potential impact of favorable monetary policy shifts and the economic stimulus provided by tariff adjustments as significant catalysts for future expansion. Other manufacturers are pinning their hopes on a "slowdown in accelerating costs" and an ability to "grow market share through innovation," underscoring a strategic focus on operational efficiency and competitive differentiation.

Recessionary Fears Subside, Growth Prospects Improve

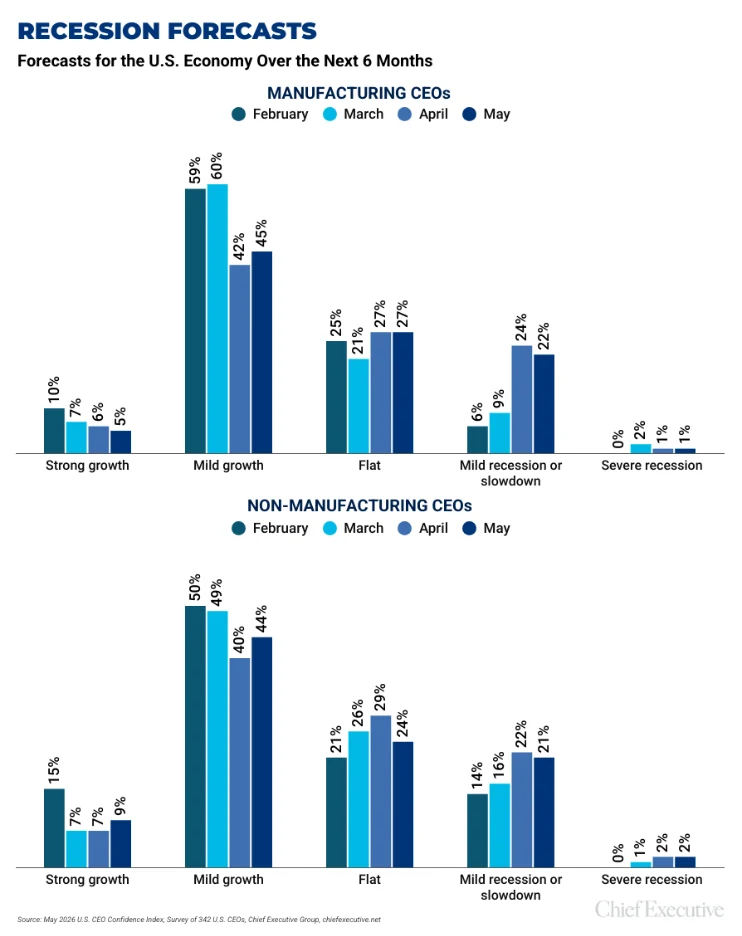

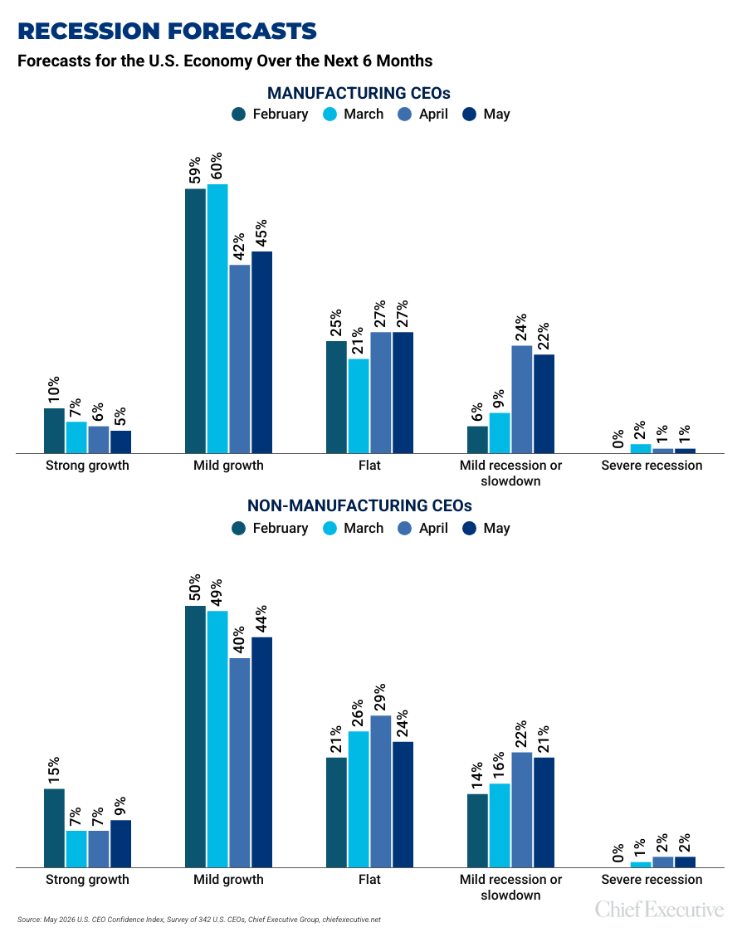

This prevailing optimism has also translated into an improvement in recession forecasts for May. Following a significant increase in the proportion of manufacturers expecting a recession in April, the latest survey indicates a more balanced view. Exactly half of the surveyed manufacturers now project economic growth, a slight uptick from 48 percent in the previous month. While a substantial 23 percent still anticipate recessionary conditions, this figure represents a decrease from April’s 25 percent, suggesting a gradual easing of recessionary concerns within the sector.

In a comparative analysis, non-manufacturing CEOs, while also experiencing a more pessimistic turn in their overall forecasts, continue to exhibit a higher degree of optimism than their manufacturing counterparts regarding near-term growth. 53 percent of non-manufacturers now expect some form of growth in the next six months, an increase from 47 percent in April. This suggests that while challenges are recognized across the board, different sectors are experiencing and anticipating these economic forces in distinct ways.

Artificial Intelligence: A Future Catalyst for Profitability

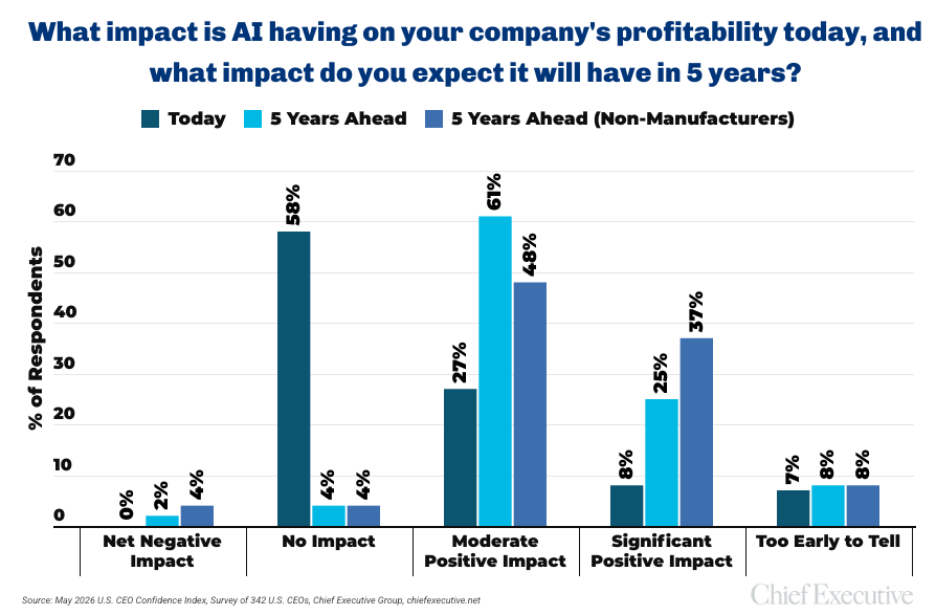

Beyond immediate economic indicators, the survey also sheds light on the burgeoning role of artificial intelligence (AI) in the manufacturing sector. While a majority of U.S. manufacturers (58 percent) currently report that AI has no impact on their current profitability, this figure is largely attributed to the ongoing process of AI integration and the nascent stages of defining its return on investment within organizations.

However, when the time horizon shifts to the future, the perception of AI’s impact becomes overwhelmingly positive. A remarkable 86 percent of manufacturing CEOs forecast that AI will have some form of positive impact on profitability within five years, with the majority anticipating a moderate effect. This long-term bullishness suggests a strategic understanding of AI’s transformative potential, even if its immediate financial benefits are not yet widely realized.

Non-manufacturers, in comparison, tend to be even more bullish on AI’s future impact. 37 percent of this group forecast a significant positive AI-driven impact on profitability five years down the line. This indicates a broader and perhaps more aggressive adoption strategy for AI across the entire business landscape.

A negligible minority in both groups foresee net negative effects from AI by 2031, with 2 percent of manufacturers and 4 percent of non-manufacturers expressing such concerns. This underscores a widespread consensus on AI’s potential to drive efficiency, innovation, and ultimately, profitability.

The Evolving Manufacturing Landscape

The current climate for manufacturing leaders has been shaped by a complex interplay of factors since late 2025. The escalation of international conflicts, most notably in the Middle East, has disrupted established supply chains, leading to increased lead times and heightened logistical challenges. Concurrently, price volatility across raw materials, energy, and transportation has put significant pressure on operational costs. Add to this the evolving regulatory landscape, which can introduce new compliance burdens and strategic uncertainties, and the ongoing concern of inflationary pressures that erode purchasing power and impact demand.

This multi-pronged threat has created a challenging operating environment, forcing manufacturers to constantly adapt their strategies. The resilience demonstrated by the sector, as reflected in the CEO Confidence Index, is a testament to the adaptability and forward-thinking nature of its leadership. The ability to maintain a stable current business sentiment score, even amidst such pressures, suggests a capacity for weathering short-term storms.

The projected improvement in year-ahead forecasts is not a sudden development but rather a continuation of a gradual recovery in optimism that began in late 2025. Following a period of significant downturn, the manufacturing sector has been slowly rebuilding confidence. The recent uptick in May signifies a more robust affirmation of this trend, suggesting that the anticipated resolutions to current global stressors are becoming more tangible in the minds of business leaders.

Understanding the CEO Confidence Index

The Chief Executive CEO Confidence Index has been a vital barometer of business sentiment among U.S. CEOs since its inception in 2002. Compiled by Chief Executive Group, the Index surveys hundreds of CEOs from organizations of all types and sizes, providing invaluable insights into their perceptions of current and future business environments. The survey methodology involves assessing various economic and business components, allowing for a nuanced understanding of confidence levels across different sectors and over time. This long-standing data collection effort offers a critical historical perspective on business cycles and the strategic responses of corporate leadership.

The data collected for this report, specifically the May 5-6 survey, involved 342 U.S. CEOs. The methodology ensures a representative sample, allowing for broad generalizations about the manufacturing sector and the broader business community. The consistent polling methodology over two decades provides a robust dataset for tracking trends and identifying shifts in economic outlooks. For further details and access to prior months’ data, the ChiefExecutive.net website serves as a comprehensive resource, offering in-depth analysis and historical trends of the CEO Confidence Index. This ongoing commitment to data collection and dissemination plays a crucial role in informing business strategy and public understanding of the economic landscape.