Despite ongoing geopolitical tensions, fluctuating commodity prices, evolving regulatory landscapes, and persistent inflationary pressures that continue to temper immediate business forecasts, a palpable sense of cautious optimism is emerging within the U.S. manufacturing sector. Year-ahead confidence has shown a moderate but significant improvement this month, signaling a collective belief among industry leaders that a resolution to current challenges is on the horizon.

The confluence of international conflict, particularly the prolonged instability in the Middle East, coupled with significant price volatility across key inputs and the specter of continued inflation, has created a multi-faceted threat for manufacturing leaders since late 2025. These stressors have cast a long shadow over current business sentiment, leading to a period of cautious assessment. However, the latest data from Chief Executive‘s CEO Confidence Index Survey, conducted on May 5-6 among 342 U.S. CEOs, indicates a shift in perspective when looking towards the future.

Current Conditions Remain Stable, Future Outlook Brightens

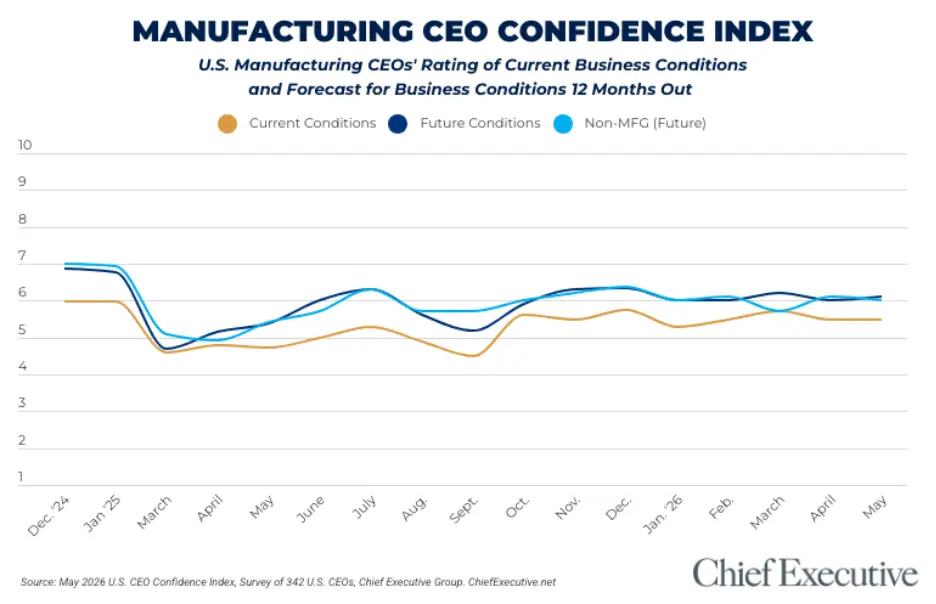

Manufacturers are currently rating their business conditions at a 5.5 out of 10, a score that has remained relatively consistent since February 2026. This period coincided with the intensification of the conflict in the Middle East and its subsequent impact on global supply chains, which became a primary concern for the sector. While this score reflects a stable, albeit not booming, operational environment, it is a notable improvement from the sentiment recorded for much of the preceding year.

The real story, however, lies in the forward-looking projections. When asked about their expectations for the next 12 months, U.S. manufacturers anticipate an improvement in business conditions, forecasting an increase to 6.0 out of 10 by this time next year. This represents a 2 percent uptick from April’s figures and indicates that 52 percent of U.S. manufacturers share this optimistic outlook. This recovery in optimism is particularly significant as it begins to counteract the 3 percent decline in the Index experienced last month, suggesting that the sector is beginning to absorb and adapt to the prevailing uncertainties.

A Divergent Path from Broader CEO Sentiment

Interestingly, the manufacturing sector’s trajectory is diverging from that of the broader CEO community. While overall ratings for current business conditions among all surveyed CEOs have seen a slight improvement, their future forecasts have experienced a 1 percent decline since April. This suggests a growing inclination among a larger segment of CEOs to adopt a "wait and see" approach, perhaps due to the multifaceted nature of global economic uncertainties that extend beyond the manufacturing sphere. This cautious stance among the general CEO population underscores the unique resilience and forward-looking conviction demonstrated by the manufacturing sector.

Drivers of Optimism: Demand Recovery and Resolution of Headwinds

Several factors are contributing to this renewed sense of optimism within manufacturing. A key driver appears to be an improvement in demand, particularly within the technology and consumer products sub-sectors. These segments, often at the forefront of economic shifts, are showing signs of robust recovery, bolstering confidence. Furthermore, there is a growing expectation that the current period of volatility will begin to abate before 2027, providing a clearer runway for strategic planning and investment.

Randy Colwell, CEO of Holloway America, a mid-sized industrial manufacturer, encapsulates this nuanced perspective. "Right now, our market is strong and material costs are steady," Colwell stated, "but higher interest rates and fuel costs may worsen the market. Especially if the war in Iran slows, we see good growth in the next 12 months." His sentiment highlights the delicate balance between immediate concerns and the anticipated benefits of a de-escalation of global conflicts and a potential easing of economic pressures.

Echoing this hope, Art Hamilton, president of Hamilton International, a mid-sized industrial fabrics manufacturer, expressed his belief that "interest rates will be lower in the year ahead. Also, the tariff refund will drive growth." This points to specific policy and economic factors that manufacturers are closely monitoring and which, if they move favorably, are expected to provide a significant boost. Beyond these specific indicators, a broader hope for a "slowdown in accelerating costs" and the ability to "grow market share through innovation" also underpins the sector’s forward-looking strategy.

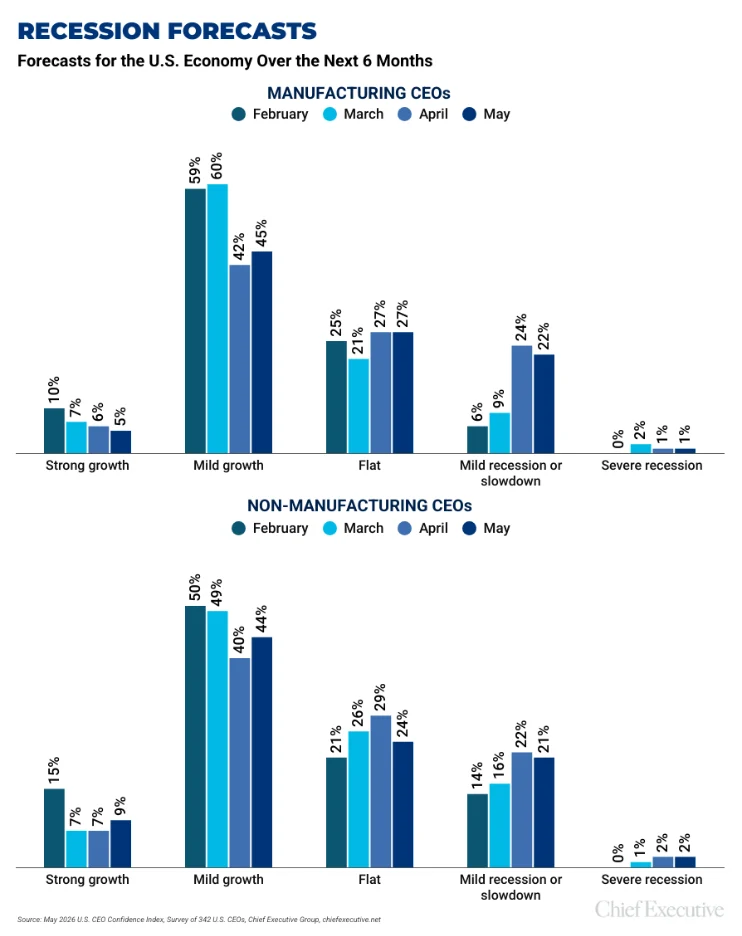

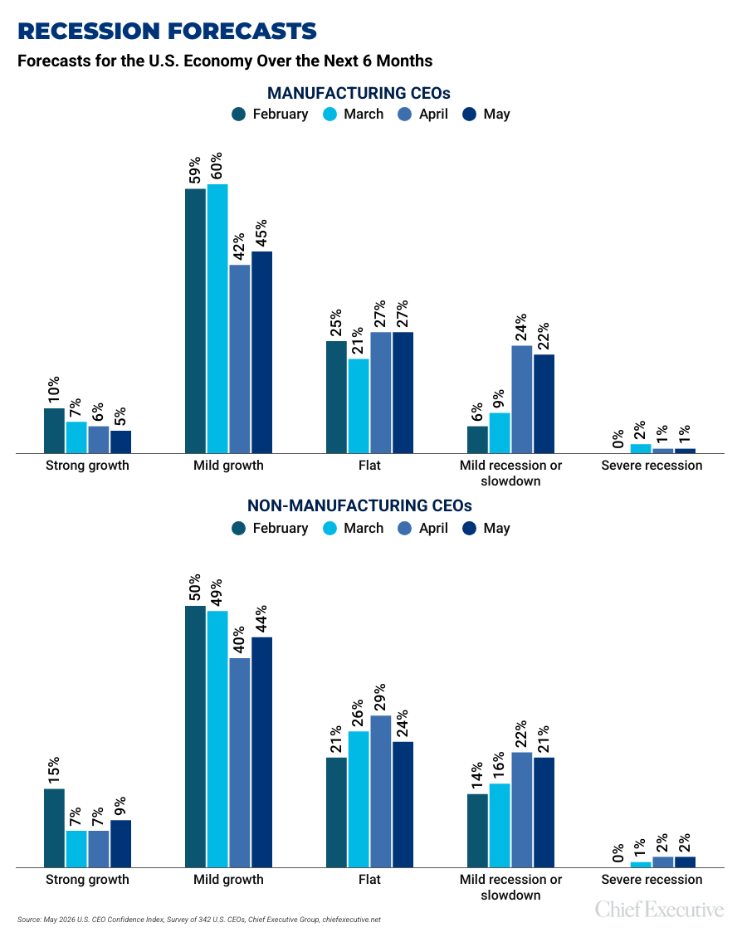

Recessionary Fears Ease as Growth Projections Rise

The optimistic year-ahead outlook has also translated into a more favorable view on recessionary risks. After a significant increase in the proportion of manufacturers expecting a recession in April, May has seen a notable improvement. Exactly half of the surveyed manufacturers now project growth, up from 48 percent in the previous month. While 23 percent still anticipate recessionary conditions, this figure represents a decrease from April’s 25 percent, indicating a gradual but positive shift away from widespread recessionary fears. This recalibration suggests that manufacturers are increasingly factoring in potential growth drivers and the resolution of current economic impediments into their outlooks.

Non-Manufacturers Show Confidence, But Manufacturers Lead on Future Outlook

While non-manufacturing sectors also display increasing confidence, manufacturers are demonstrating a more pronounced optimism regarding future conditions. In the next six months, 53 percent of non-manufacturers expect some form of growth, an increase from 47 percent in April. However, the manufacturing sector’s more significant jump in year-ahead projections highlights their specific industry drivers and a more targeted optimism for their immediate future.

Artificial Intelligence: A Long-Term Game Changer

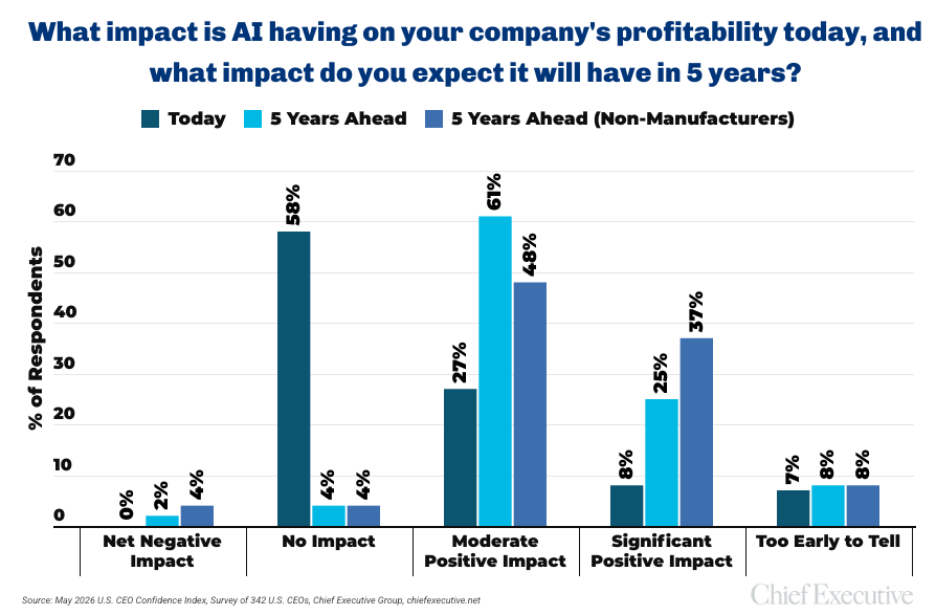

Beyond immediate economic forecasts, the role of artificial intelligence (AI) in shaping the future of manufacturing is a significant point of discussion. While the immediate impact of AI on current profitability is perceived as minimal by most U.S. manufacturers (58 percent reporting no impact), this is largely attributed to the ongoing process of AI adoption and the establishment of clear return-on-investment (ROI) frameworks. Many organizations are still in the early stages of integrating these advanced technologies.

However, when looking further ahead, the sentiment shifts dramatically. A substantial 86 percent of manufacturing CEOs forecast that AI will have a positive impact on profitability within five years, with the majority anticipating a moderate positive effect. This long-term perspective underscores a strategic understanding of AI’s transformative potential, even if its immediate financial dividends are yet to be fully realized.

In comparison, non-manufacturers tend to be even more bullish on AI’s future impact, with 37 percent forecasting a significant positive AI-driven boost to profitability in five years. This suggests a broader awareness and perhaps a faster adoption rate of AI’s capabilities across the entire business landscape. The proportion of both groups forecasting negative effects from AI by 2031 remains a slim minority, with 2 percent of manufacturers and 4 percent of non-manufacturers anticipating net negative outcomes. This data suggests a widespread belief in AI as a net positive force for business growth and efficiency.

Historical Context and Methodology of the CEO Confidence Index

The CEO Confidence Index, compiled by Chief Executive Group since 2002, has been a vital barometer of U.S. business sentiment. The survey polls hundreds of U.S. CEOs from organizations of all types and sizes, tracking their confidence in both current and future business environments. The index is based on CEOs’ observations of various economic and business components, providing a comprehensive snapshot of leadership perspectives. This consistent methodology allows for the tracking of trends and the identification of significant shifts in sentiment, such as the current uptick in manufacturing confidence.

The current data, collected over a two-day period in early May, represents a snapshot in time. However, the sustained stability in current conditions coupled with the marked improvement in year-ahead forecasts provides a compelling narrative of resilience and forward-looking strategy within the U.S. manufacturing sector. As global uncertainties persist, the sector’s ability to adapt, innovate, and maintain a degree of optimism will be crucial for navigating the complexities of the evolving economic landscape. The increasing integration of advanced technologies like AI further signals a commitment to long-term growth and competitiveness.